From the WSJ:

Companies are stepping up spending on equipment as the recovery that first took hold in manufacturing broadens to other areas of the economy.

.....

A Commerce Department report Thursday showed that orders for durable goods—items expected to last at least three years—fell 1.1% in May from April, a drop that was driven by a decline in often-choppy aircraft orders. But a key measure that economists watch to gauge capital-spending plans—nondefense capital-equipment orders excluding aircraft—rose 2.1% and was 18.4% above its year-earlier level.

.....

A Commerce Department report Thursday showed that orders for durable goods—items expected to last at least three years—fell 1.1% in May from April, a drop that was driven by a decline in often-choppy aircraft orders. But a key measure that economists watch to gauge capital-spending plans—nondefense capital-equipment orders excluding aircraft—rose 2.1% and was 18.4% above its year-earlier level.

.....

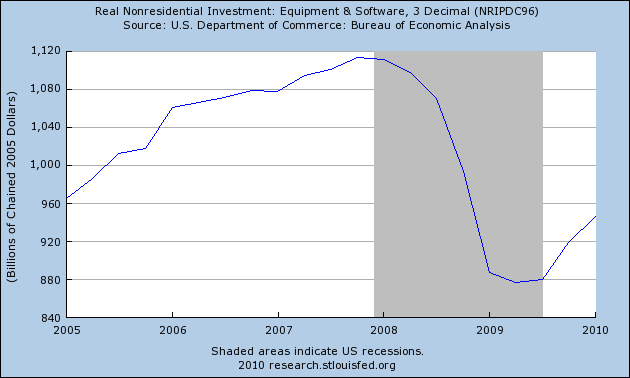

This has been an untalked about part of the recovery -- how inventory restocking and foreign demand is helping US manufacturing to grow which in turn leads to more investment.

However, here is the basic chain of events:

The ISM manufacturing index is at strong levels. As a result,

durable goods orders have turned around. In addition, the increase productivity

Firms have increased their investment in equipment and software.

In addition, this is not just a story about manufacturing:

increased non-manufacturing orders are helping as well.