With that being said, I do think it is possible to see general trends with the understanding they could change at a moments notice depending on what is happening in the economy at large.

Trend number 1:

Hopefully, housing will stabilize at some point in 2008, but not until the last two quarters. Housing still has a long way to go before it hits bottom so I don't think it's even possible until the end of the year. Here's the bottom line: inventory is sky high, the credit markets are frozen the underwriting standards are getting tighter. In addition, there is the foreclosure issue. The main estimate I have seen in this area is 1.2 million foreclosures are possible in 2008. The most liberal estimate I have seen for the number of homeowners that will benefit from the Paulson plan is 600,000. Assuming both those numbers to be true, we have an additional 600,000 homes hitting the existing home inventory numbers. That's on top of the people who want to sell for other reasons.

So -- we already have a super-glut of inventory on the market with the possibility of more homes coming on the market and it's harder to get a loan.

Econ 101: Increasing supply + decreasing demand = lower prices.

Trend number 2:

Slowing consumer spending. While I don't think Americans will stop spending (largely because Americans never stop spending) I do expect the combination of the housing market mess and a slowing economy to lower consumer spending for most of the year. Also add in the possibility of higher gas and food prices and you have further hits to discretionary spending habits.

Keep a close eye on the Christmas numbers; these will give us a decent indicator of consumer sentiment and desire to spend.

Trend number 3:

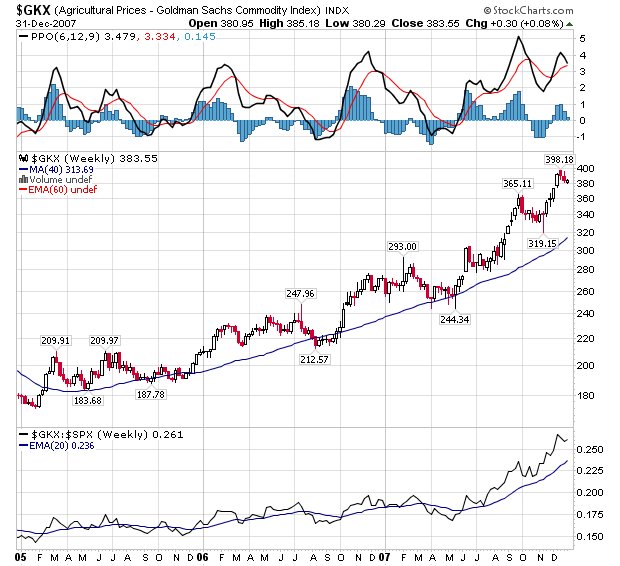

Commodity inflation will be with us for most of the year. Agricultural prices are in the middle of a three year rally:

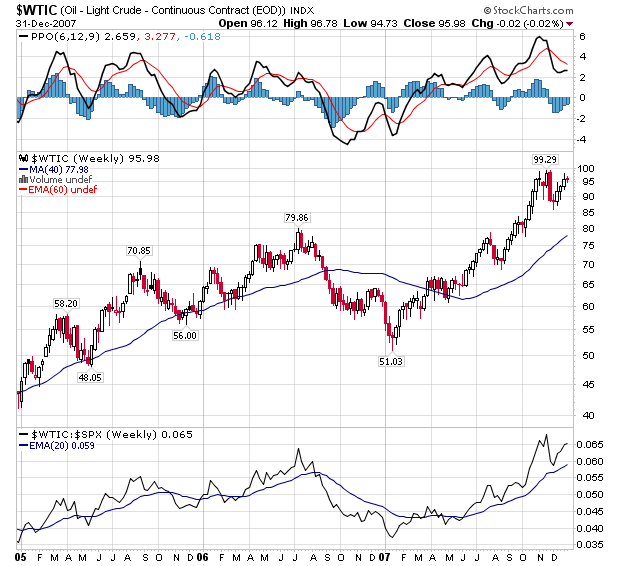

Oil is in the middle of a year long rally:

There is no reason to think this will change anytime soon. With India and China coming on line there are now two billion more people who want food and energy. That's an awful lot of demand and I think it's enough to keep prices moving higher.

Trend number 4

A hemmed in Fed: Boy would it suck to be a member of the Federal Reserve right now. On one hand the economy is under enormous downward pressure. On the other hand, we have commodity inflation that will probably be getting worse as I detail above. I think commodity inflation is the primary reason the Fed has opted for a liquidity injection rather than a more aggressive rate decision. I would expect more outside the box thinking from the Fed on this issue. Because of commodity inflation I am very wary of aggressive predictions for Fed action.

Trend Number 5

Credit market turmoil continuing: The predictions for total writedowns in the credit markets range from $300 -- $500 billion. But there have only been about $100 billion in total writedowns so far. Assuming the $300 - $500 range is accurate, that means we have an additional $200 billion more of writedowns to go at a minimum. So long as that problem is out there, expect institution to institution level lending to be a problem. And as long as that goes on the credit markets will have a hard time getting anything done.

It's taken us about 6 months to get through about $100 billion in writetdowns. Assuming that time line holds and assuming the $300 - $500 billion of total writedowns is accurate, we've got about a years worth of bad news to go, assuming the pace of announcements during 2007 holds for 2008.

Trend Number 6

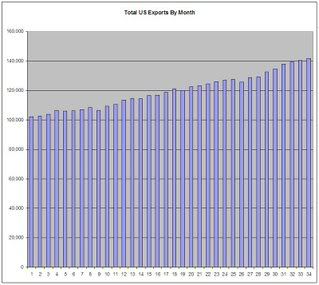

Increasing Exports: Thanks to a decreasing dollar US exports are doing quite well. Here is a chart from the Census Bureau of total monthly exports. Notice it has been increasing for the last three years.

All of this being said, let me add this one caveat. There are plenty of plausible reasons why none of these will play out for the entire year. There are simply too many unknowns over a 12 month period to effectively predict the validity of these predictions. So don't assume any of these are golden. They are all based on the information we have as of January 1, 2008.

SO -- keep these in mind, but remember to stay flexible.