Our U.S. Investment Strategy service noted last week in a Special Report that corporate bond spreads have stayed tight, and the level of bond yields remains low, acting to turbo-charge the stampede to buy/retire equities. The wide gap between equity and corporate bond valuations is being arbitraged and will persist until the valuation gap is closed. If a mania develops like in the late 1990s, then the gap could even move into negative territory. Although such a shift seems a long way off, M&A activity is expediting the re-leveraging, and the financial and investment communities are rushing to take part in this stampede.

They also had a very nice graph accompanying the highlights:

The graph highlights a few interesting points:

1.) Corporations are issuing more debt than equity.

2.) The total value of M&A activity (as a percentage of GDP) is approaching the pace of the late 1990s, but isn't there yet.

According to the Federal Reserve's Flow of Funds report (PDF) corporations have cleaned up their balance sheets over the last few years. Total liabilities of non-farm non-financial corporate business increased (in billions) from $9,922 at the end of 2002 to $10,493 at the end of the 4th quarter in 2006, or an increase of 5.75%. Over the same period, total assets increased (in billions) from $19,473 to $24,621, or an increase of 26.43%. As a result, total net worth of US business increased (in billions) from $9,551 at the end of 2002 to $14,128 (see page 103 of the FOF).

It's not that corporations have been issuing tons of debt. Non-financial corporate business issued $132.3 billion debt in 2002 and $322.3 billion in the last quarter of 2006 (see page 44 FOF). However, corporations have been buying back tons of stock. Non-financial corporate business issued -41.6 billion of equities in 2002 and -701.2 billion in the 4th quarter of 2006 (page 45 FOF).

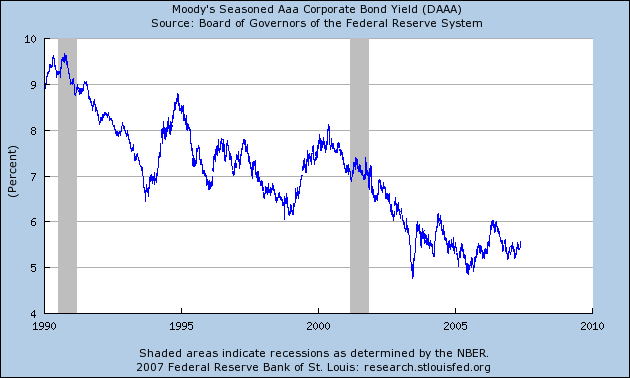

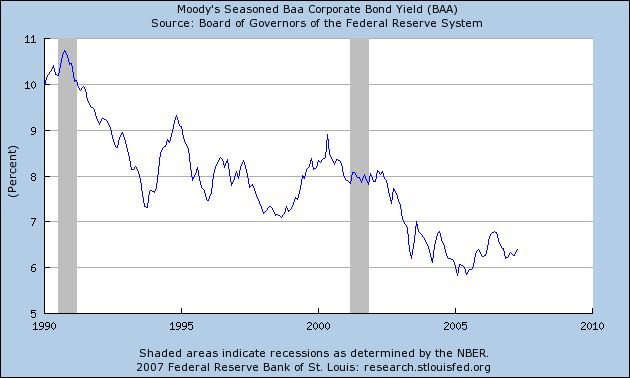

What's a bit odd about this is corporate bond yields have been conducive to borrowing. Here is the yield of the AAA and BBB corporate market from the St. Louis Federal Reserve:

So, let's sum up this picture.

1.) Non-financial, non-farm business is in great financial shape. Debt issuance is low and stock buy-backs are high.

2.) As a result, corporations are in a great place to perform tons of M&A activity. Interest rates are still very low, which encourages this activity.

Let's carry this one step further. A weak economy actually plays into the M&A rally because a weak economy increases speculation the Fed will lower rates, which will add more fuel to the M&A fire.