- by New Deal democrat

Let’s take a look at the new month’s first data, on manufacturing and construction.

The ISM manufacturing index, and especially its new orders subindex, is an important short leading indicator for the production sector. In May both increased, by 0.7 to 56.1, and by 1.6 to 55.1, respectively. The breakeven point between expansion and contraction is 50, so these both remain solidly positive, if not white hot like they were during last year’s Boom (new orders shown in graph below):

This forecasts continued economic expansion on the production side through summer into early autumn.

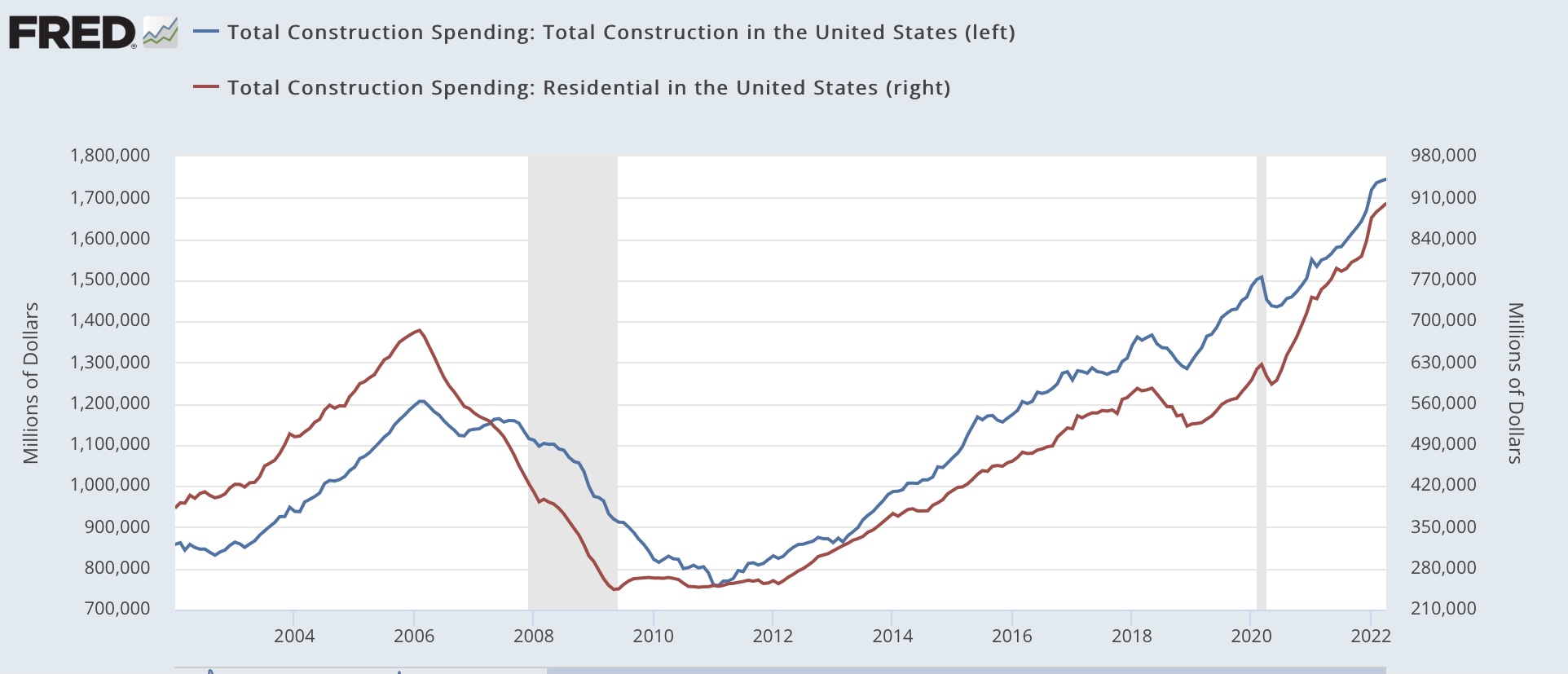

Meanwhile, construction spending rose 0.2% in nominal terms in April, and March’s number was revised up 0.2% to 0.3%. The more leading residential sector rose 0.9%, both thus making new highs:

On a YoY basis, nominal residential construction spending is up 18.4%.

Adjusting for price changes in construction materials, which declined -0.2% for the month, and have been almost exactly unchanged since January, “real” construction spending rose 0.4% m/m, and residential spending rose 1.1% m/m. In absolute terms, “real” construction spending has declined sharply - by -16.7% - since its peak in November 2020, while “real” residential construction spending has declined -9.4% since its post-recession peak in January of last year, and has risen by about 6% in the past six months:

While total construction spending has declined by more than the -10.4% it did before the Great Recession, the decline in residential construction spending, while substantial, at its worst was only as bad as its 2018-19 decline, and was nowhere near the -40.1% decline it suffered before the end of 2007. In general these two series have been helped considerably by the fact that the cost of construction materials has stopped rising this year.

Mindful of the fact that it takes awhile for the downturn in mortgage applications, sales, and permits to filter through into actual construction, especially with record numbers of housing units permitted but not yet started, these two reports point to continued growth, albeit at a slower pace than last year, in manufacturing and construction in the next few months.