- by New Deal democrat

Last week I took an updated look at the long leading indicators identified by Prof. Geoffrey Moore, the founder of ECRI, 20 years ago. None of those 4 series, which in the past have generally topped out 12 months or more before the economy as a whole, showed any sign of rolling over. This morning the Conference Board's LEI also showed a continued positive trend, increasing 0.6 in April (thanks in large part to building permits, initial jobless claims, and the yield curve), and +1.7 over the last 6 months.

In addition to his long leading indicators, Prof. Moore also proposed a series of 11 short leading indicators. These are more variable but typically turn a few months before the economy as a whole. Moore identified them as:

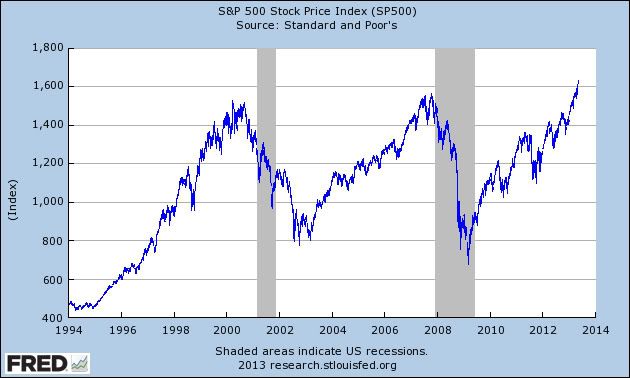

S&P 500 stock price index

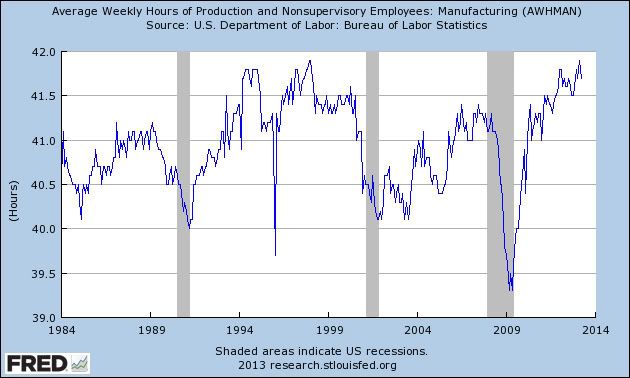

Average workweek in manufacturing

Layoff rate under 5 weeks

Initial claims for unemployment insurance

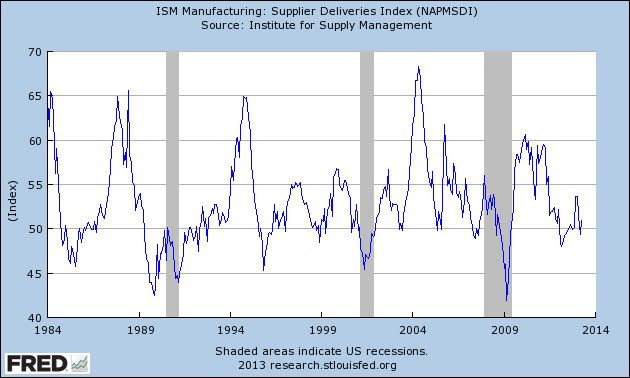

ISM manufacturing vendor performance

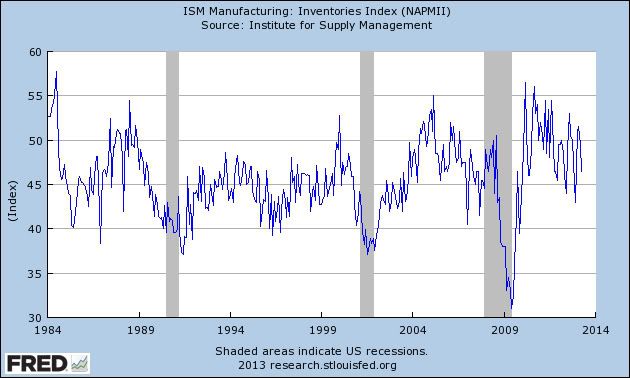

ISM manufacturing inventory change

Journal of Commerce change in commodity prices

Change in deflated nonfinancial debt

New orders for consumer goods and materials

Dun and Bradstreet change in business population

Contracts and orders for plant and equipment

If this list looks familiar, it is because most of its components made it into the 1990's remake of the LEI, which was subsequently turned over the the Conference Board for calculating and publishing, and over half of the components (or similar components) still are contained in the Conference Board's Index. Where they differ is primarily that the Conference Board's LEI is a mix of longer (e.g., building permits) and shorter (e.g., initial jobless claims) indicators, whereas Moore advocated monitoring the Long Leading Index, and then looking for confirmation of a turn in the short leading index.

So let's look at the components of Moore's Short Leading Indicators in order. First, here's the S&P 500:

No surprise here, this index has been making new highs.

Here's the average workweek in manufacturing:

Unlike the stock market, this has declined slightly in the last few months (although not as much as it typically does before the onset of a recession):

Here is the layoff rate for 0 to 5 weeks. This is a series from the monthly employment report:

This series made new yearly lows in the last couple of months, and has only been lower one time since the end of the great recession.

Iniital jobless claims have also been trending lower:

The minimum time between these establishing a new low and the onset of a recession has been 3 months, but is usually longer.

ISM vendor performance is one of the indexes in the monthly ISM manufacturing report:

This has been at a rate consistent with both expansions and recession, so is giving an ambiguous signal.

ISM inventory changes also come from the monthly ISM manufacturing report:

These are consistent with continued growth.

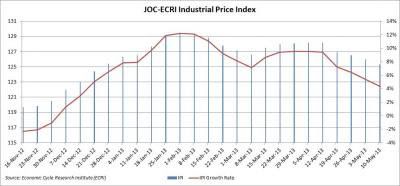

Next is the JoC-ECRI commodity price index:

This is greatly influenced by the price of oil.

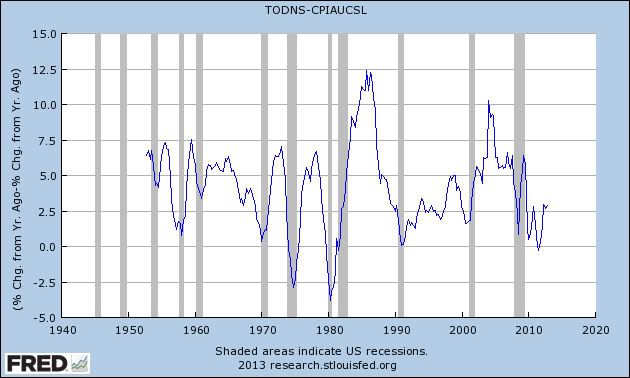

The change in deflated nonfinancial debt:

This series has recently been increasing, not declining.

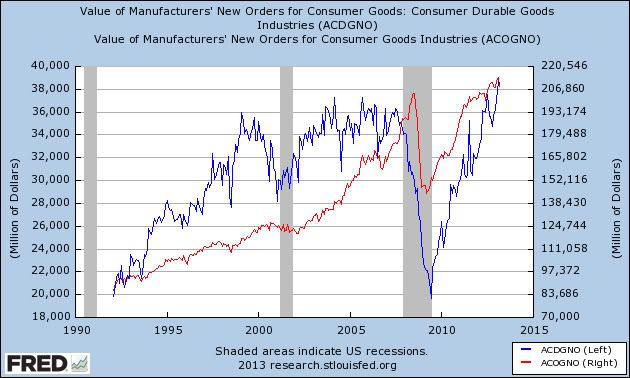

New orders for consumer durables and materials are part of the durable goods report:

These are holding up rather well.

I am told that Dun and Bradstreet's tabulation of business starts and bankruptices still does exist, but is proprietary and only available in a specialist publication. It is the only indicator to which I don't have access.

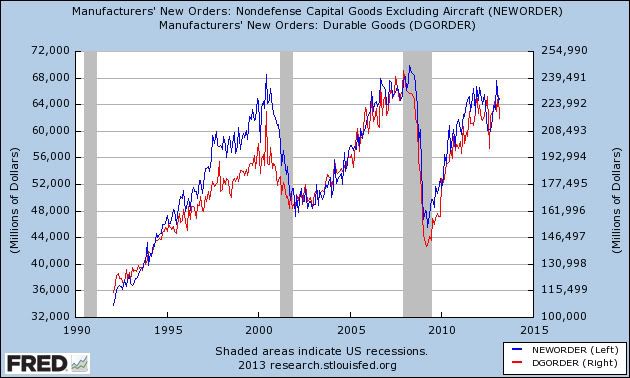

Finally, contracts and orders for plant and equipment are no longer kept in the same format, but a successor series is the new factory orders report, both in total and for core capital goods excluding aircraft, both of which are shown below:

Like other manufacturing series, these are flagging, but are not decisively showing either recession or expansion.

Generally speaking, there is a bifurcation in the short leading indicators. Those closely associated with manufacturing have either stalled or actually declined slightly over the last year, to the point where they are at least consistent with, if not exclusively associated with, the onset of recession. The other indicators are not consistent with recession, but continue to show an expanding economy.

In summary, with the exception of manufacturing, which is clearly hurting, both the long and short leading indicators are telling us to expect that the economy will continue to grow for the next few months and even into next year. As I indicated last week, however, this can be derailed by sudden external events. The increase in the payroll tax, Sequestration, and the next fight over the debt ceiling coming up in a few months all qualify as such shocks.