- by New Deal democratMonthly data released this week showed relief from the manufacturing slowdown, as the Chicago PME rebounded to a strong 61.0 and the ISM manufacturing survey also rebounded to 55.3. The employment, new orders, and vendor delivery components were also up slightly.

New construction spending was mixed, with residential construction in May down 2%, but nonresidential construction up 1.2%. Residential construction is meandering near the bottom of a 3% range established since last July, while nonresidential construction has essentially been flat so far this year (i.e., it appears to be bottoming).

Real personal income was flat, and real personal spending decreased -0.3% in May, indicating further impact of high gas prices, and consumer confidence and University of Michigan consumer sentiment were both down. The Case-Shiller house index also declined, but but not as much as expected.

The

high-frequency weekly indicators were also mixed this week.

Let's start with the good:

YoY weekly median asking house prices from 54 metropolitan areas at

Housing Tracker showed that the asking prices declined only -3.5% YoY.

This is the best reading since May 2007. The areas with double-digit YoY% declines decreased by three to 7. The areas with YoY% increases in price increased by four to 7. This adds more weight to the belief that in nominal if not real terms housing prices may bottom as early as this winter.

The

ICSC reported that same store sales for the week of June 25 increased 3.0% YoY, and increased 2.9% week over week. This is the best YoY comparison in a month.

Shoppertrak failed to report this week.

Other series remained in their recent range:

M1 was up 0.5% w/w, up 0.2% m/m, and up 12.5% YoY, so Real M1 was up 9.1%.

M2 was up 0.3% w/w, up 0.5% m/m, and up 5.2% YoY, so Real M2 was up 1.8%.

Real M1 remains very bullish, while Real M2 remains stuck in the caution zone under 2.5%

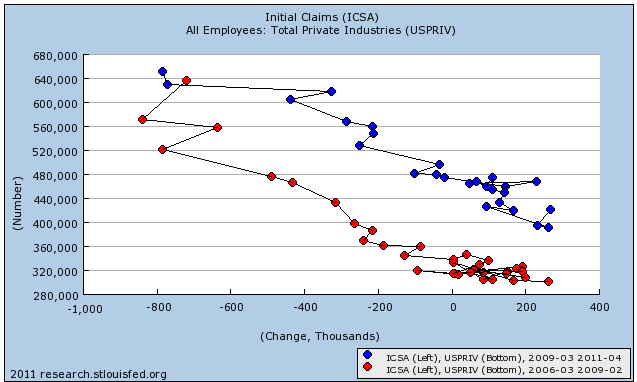

The

BLS reported that Initial jobless claims last week were 428,000. The four week average increased slightly to 426,750. We appear to have stabilized under 430,000.

The

Mortgage Bankers' Association reported that seasonally adjusted mortgage applications decreased 3.0% last week. It was 4.5% higher than this week last year. This is the fifth week in a row that YoY comparisons in purchase mortgages were positive. Except for the rush at the two deadlines for the $8000 mortgage credit, these are the first YoY increases since 2007. Refinancing decreased 7.6% w/w despite a decline in mortgage rates.

Topping the weak or bad numbers is the report from

Railfax, which was up a mere 1.3% YoY for the week. Baseline traffic is actually down 662 carloads from a year ago. Cyclical traffic was also down, 7141 carloads YoY. Intermodal traffic (a proxy for imports and exports) was the only component up this week, at +19,128 carloads YoY. This series is very close to turning negative on a carload basis.

Oil was near $94 a barrel midday Friday, right at the level of 4% of GDP which according to Oil analyst Steve Kopits is the point at which a recession has been triggered in the past. Gas at the pump fell for the sixth week in a row, declining $.08 more to $3.57 a gallon. Gasoline usage at 9261 M gallons was -2.2% lower than last year's 9462. This is the first time in five weeks that gasoline usage has been significantly less than last year.

The

American Staffing Association Index remained at 87 for the third week in a row This series is just barely above a stall, and is a significant danger sign. It is weaker than early 2007, but not trending down as during the recession.

Weekly

BAA commercial bond rates remained the same at 5.73%. This compares with yields on 10 year treasury bonds decreasing .01% to 2.99%. The continuing decline in treasury rates shows fear of deflation, and the relative increase in corporate rates shows a slight increase in relative distress in the corporate market.

Adjusting +1.07% due to the 2011 tax compromise, the

Daily Treasury Statement showed that for the first 21 days of June 2011, $135.2 B was collected vs. $136.5 B a year ago, for a decrease of $1.3 B YoY. For the last 20 days, $134.8 B was collected vs. $115.9 B a year ago, for an increase of $18.9 B, or 15%. Use this series with extra caution because the adjustment for the withholding tax compromise is only a best guess, and may be significantly incorrect.

While much of the data shows a stall, almost none of it shows any actual decline in economic activity. Housing and Oil prices continue to appear to be moving in the right direction. Contractionary fiscal policy coming out of Versailles remains the biggest risk.

Have a happy and safe Fourth of July weekend!