Residential real estate markets remained weak, but signs of improvement continued to be noted. Chicago, Richmond, Boston, and San Francisco observed an uptick in sales over the last six weeks, while sales in the Philadelphia District were described as steady. St. Louis commented that residential home sales had not improved. Most Districts reported that sales remained below the levels of a year earlier. However, Atlanta, New York, Cleveland, and Minneapolis documented some year-over-year gains in select markets. Most Districts noted that demand remained stronger at the low-end of the housing market. Boston, Cleveland, Dallas, Kansas City, Richmond, and New York indicated that the first-time home buyer tax incentive was spurring sales. However, Philadelphia did note an upturn in sales at the high-end of the market. Reports on house prices generally indicated ongoing downward pressures, although Dallas and New York noted some increases. Construction remained at low levels overall, although Chicago and Dallas reported a small increase in activity.

The points made are consistent with the following charts of homes sales.

New homes sales have bottomed and are showing a slight increase.

Existing home sales increased at a good rate last month.

While we are still seeing a year over year decline in housing prices, we are starting to see month to month improvement:

The prices of single-family homes in 20 major cities rose a not-seasonally adjusted 1.4% in June, the second increase in a row after falling every month for three years, according to the Case-Shiller home-price index released Tuesday by Standard & Poor's.

Commercial real estate is still having problems:

Reports on commercial real estate markets indicated that demand for space remained weak and that construction continued to decline in all Districts. Atlanta, Philadelphia, Richmond, and San Francisco reported that vacancy rates increased, while rates held steady in the Boston and Kansas City Districts and were mixed in New York. Boston, Dallas, Kansas City, Philadelphia, and Richmond commented that the demand for space remained weak. Commercial rents declined according to Boston, Chicago, New York, Philadelphia, and Richmond. Rent concessions were reported in the Richmond and San Francisco markets, and Richmond noted that some landlords had postponed property improvements in an effort to conserve cash. Construction remained at very low levels, with modest improvements noted in public construction in the Chicago, Cleveland, and Minneapolis Districts.

There's been a great deal written about the impending commercial real estate collapse. However, a closer look at the data indicates the word collapse is a bit far-fetched:

U.S. banks have been charging off soured commercial mortgages at the fastest pace in nearly 20 years, according to an analysis by The Wall Street Journal. At that rate, losses on loans used to finance offices, shopping malls, hotels, apartments and other commercial property could reach about $30 billion by the end of 2009.

The losses by regional banks on their commercial real-estate loans will be among the most watched details as thousands of banks report second-quarter results over the next two weeks. Many of the most troubled banks have heavy exposure to commercial real estate. So far, 57 banks have failed this year.

The $30 billion estimate is based on financial reports filed by more than 8,000 banks for the first quarter. The trend continued as a handful of major banks reported second-quarter results, including Goldman Sachs Group Inc., J.P. Morgan Chase & Co. and Bank of America Corp. Regional banks tend to have higher exposure to commercial real estate than these big financial institutions.

While $30 billion is not good, it is hardly a fact on which to make calls for an apocalypse. In short, the market should be able to handle that. While other estimates place the total losses higher (at a maximum rate of $150 billion) it's still not a a level where we should be making doomsday predictions. And while there is also trouble in commercial mortgaged baceked securities, the concern is over roughly $100 billion in total problem loans that will come due and have to be refinanced by 2012. That means the loans will have to be dealt with over a period of 2-3 years. While the development is not good and should not be applauded, this is a manageable disaster.

Most Districts reported modest improvements in the manufacturing sector. Philadelphia, Richmond, Atlanta, Cleveland, and Chicago all reported slight-to-moderate increases in new orders. San Francisco indicated that new orders increased for manufacturers of semiconductors and other IT products, while orders declined for metal fabricators and petroleum refineries. Dallas noted that orders held steady, while St. Louis reported that manufacturing output continued to decline, but at a slower pace. Richmond, Atlanta, Chicago, and Minneapolis reported increases or planned increases in automobile and automobile-related production. Several Districts also noted increased production in the pharmaceutical industry.

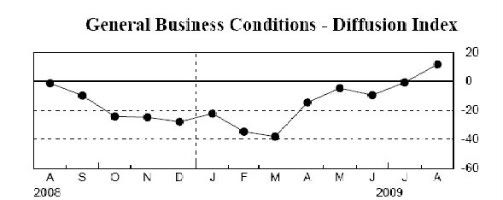

This has been a surprisingly uncovered series of stories. Consider these charts of the various Federal Reserve district's manufacturing surveys:

The Empire State index (NY) has been increasing for several months and is now above 50.

The Philly Fed index is right about expansion levels, as is

The Richmond Fed's numbers.

And the national ISM number is now above 50, indicating expansion in the manufacturing sector. Overall, manufacturing is showing clear signs of pulling out of the recession.

Labor market conditions remained weak across all Districts, but several also noted an uptick in temporary hiring and a decline in the pace of layoffs. Richmond reported that most service-providing firms continued to cut employees, while Minneapolis and New York noted additional layoffs in the manufacturing sector. Cleveland reported modest job declines in the banking, commercial construction, and coal mining sectors. Further job cuts are expected in auto manufacturing according to St. Louis, and Dallas indicated further staff reductions are anticipated in the airline, energy, and residential construction sectors. Staffing firms in a majority of Districts reported a modest increase in the demand for temporary workers, although industry contacts in Boston also questioned whether these gains will persist. New York cited a modest pickup in temporary hiring for the legal and financial industries. Chicago noted an uptick in demand for workers in the healthcare and information technology industries. St. Louis and Minneapolis reported that federal stimulus funds have had a positive impact on construction and local government jobs.

I analyzed the latest jobs report here. Here is a list of the conclusions from the article:

1.) The rate of job destruction has decreased since the beginning of the year. Remember that at the end of last year the beginning of this year, the economy was losing 600,000 jobs per month. To expect that figure to turn around and print a positive number within 6-9 months is highly unrealistic. In fact, it is most possible that we'll see job losses through the next 3-6 months. But the pace of job losses is decreasing which is good news.

2.) The increase in the unemployment rate is bad news, plain and simple.

3.) The steady size of the number of people working part-time for economic reasons along with the possible topping out of discouraged workers is also good news as it indicates a possible topping of two categories of labor under-utilization.

4.) Two of the four time periods of unemployment showed improvement last month and the worst category (people unemployed for 27 weeks and longer) showed a far slower rate of acceleration.

5.) The increase in the marginally attached and the number of people unemployed for 5-14 weeks are bad developments.

There is one important point with the unemployment rate: it is a lagging indicator. History shows us that on a year over year basis, GDP must turn positive before we can even think about a decline in the unemployment rate. As such, we're simply not in a position to be talking about a drop in the unemployment rate yet.

Consumer spending remained soft in most Districts. The majority of Districts reported that retail activity was flat. Boston, Philadelphia, and Kansas City noted improvement in sales, but attributed the increase primarily to back-to-school purchases. Philadelphia, Chicago, Cleveland, and San Francisco observed that shoppers remained focused on essentials and continued to refrain from purchasing discretionary and big-ticket items. Kansas City and San Francisco noted weak restaurant sales. Richmond, Philadelphia, Chicago, Atlanta, and Boston remarked that retailer inventories were being closely monitored and were keeping them in line with low sales levels.

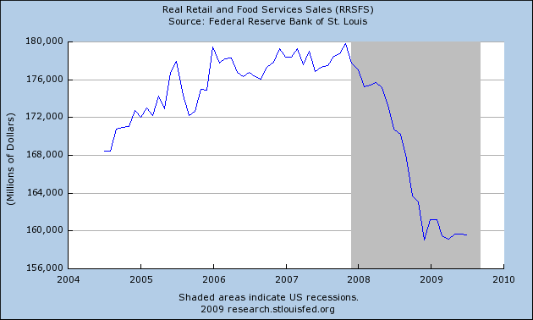

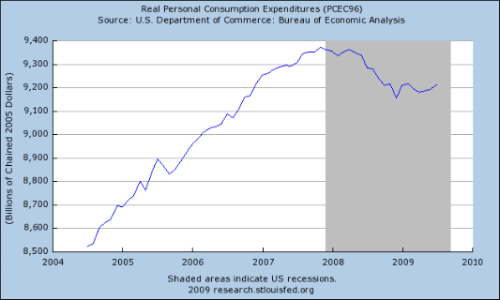

While spending is soft, it has stabilized as these two charts demonstrate:

Real (inflation-adjusted) retail sales have bottomed, as have

Real personal consumption expenditures.

Let's review:

1.) Housing sales have stabilized.

2.) Housing prices are still declining on a year over year basis, but have shown improvement over the last two months.

3.) The talk of a commercial real estate "implosion" is a bit far-fetched. There are problems but they are manageable.

4.) Manufacturing is now expanding.

5.) The labor market is still weak, but the rate of job loss continues to decrease and metrics within the jobs report (the number of people unemployed for specific lengths of time) is showing improvement. The latest Beige Book mentions in several places of an uptick in temporary help. Finally, the unemployment rate is a lagging indicator; it is unrealistic to talk of an improvement in the unemployment rate when GDP is still contracting.

6.) Consumer spending has bottomed.