Because we also turned negative in 1987 prematurely, about two or three months prematurely, and people thought we didn't recognize a new era of valuations. The two things Wall Street was talking about to support the market before the terrible October decline was the huge amount of liquidity and the big shrink in equities. Then liquidity was coming from Japan because Japanese brokers had started selling U.S. stocks. The big equity shrink was partly the result of LBOs, but mostly from companies buying back their own stock. There were other parallels. Breadth was deteriorating and investors were gravitating to big-cap stocks from small-cap stocks. There was an acceleration of inflation, which we are seeing now. There was an acceleration of interest rates, and the market kept going up in the face of higher rates, although, back then, the rise in rates was greater. There were a lot of similarities.

First, I am loathe to compare any economic or market period A to period B. There are simply too many economic and technical factors in an economy like the US to warrant this kind of comparison. The market and the economy are ever changing.

That being said, this is the first market observer who has said increasing liquidity and stock buy-backs are a net negative for the market. I have interpreted these developments as a net positive for the market for the simple reason more money floating around the world plus fewer outstanding shares means more money is chasing fewer things to buy which equals higher prices.

Let's look at his observations to see what is going on.

1.) I've written a fair amount about all of the M&A activity going on. I remember seeing an article in CBS Marketwatch that showed M&A activity for May was very high (sorry but I can't find the story). In short, there has been a ton of mergers over the last 6 months or so. It seems like every Monday we have a new round of mergers to consider. I have argued this is bullish so long as the mergers continue to make sense -- which most have. For example, the Wachovia/AG Edwards deal was a great idea because it allows Wachovia to sell financial products to AG Edwards customers and creates a retail firm with the size, resources and current customer base to compete with Merrill Lynch. This is just one example of some of the positive mergers that have occurred over the last 6-9 months.

2.) According to the Federal Reserve's Flow of Funds report (see page 45) there has been a net decrease in equities issued starting in 2005. The latest seasonally adjusted annual rate is -277.2 billion. So, the corporate buy-backs and deal making are acting to lower the amount of outstanding shares.

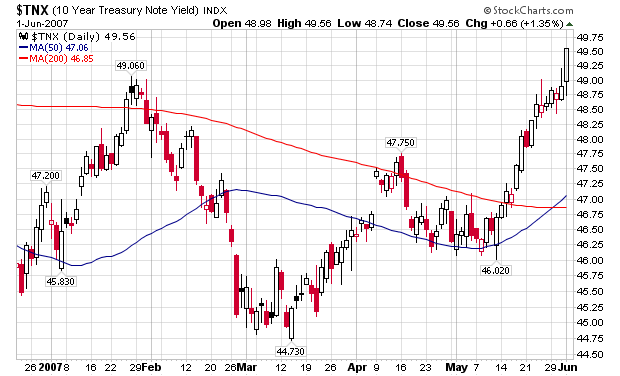

3.) Interest rates have started to creep up lately. Here is a chart of the 10-year Treasury.

I'm an old-fashioned 10-year guy. I think bond prices are determined by three forces: inflation expectations, equity performance and interest rate policy. I'm not a big fan of the 10-year minus TIPS spread analysis. I think the recent sell-off in Treasuries is simply explained: stocks are making more money and with the perception the economy will rebound in the second half of 2007 there is a concern about inflation heating up again.

4.) This analyst seems to be using a different breadth indicator (many analysts have their own proprietary indicators). However, these publicly available breadth charts from Stockcharts indicate NY new highs/new lows and overall market breadth is OK. The NASDAQ breadth has been an issue for some time, although the new high/new low numbers are good. However, the current rally is a basic materials rally, not a tech rally so a better breadth indicator from the NYSE makes sense.

5.) According to Barron's the S&P 500's PE is 18.42. While this isn't cheap, it's not expensive either.

So, this analyst has some interesting points to make. However, I think he is wrong in concluding these are bearish indicators. I think they are all slightly bullish with the exception of the 10-year situation. Even there, however, rates are still low by historical standards. The 10-year is still under 5% which is really low.

So -- I respectfully disagree.