Well, this was an unpleasant surprise. A few days ago I wrote that if the trend of initial jobless claims compared with payrolls from the last 3 years held, we should expect a report of about +250,000 jobs. That was considerably above the consensus. Instead, as you know by now, we only got +120,000.

In that same post I wrote:

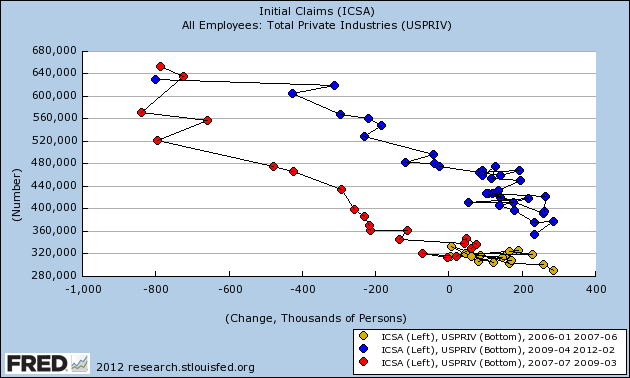

[I]f we were on the cusp of entering an economic contraction, new jobs offered would decline before layoffs increased, meaning the new entries on the scatterplot would shift substantially to the left. Should March come in under 200,000 ..., and should February also be revised down under 200,000, that would be a bad omen.Although February's report was actually revised up to +240,000, this month's report is what I would expect to see in the months leading up to a recession, per the scattershot graph comparing initial claims to payrolls (note this does not include this morning's data):

Today's report is well to the left of what the trend, just like the months as teh last recovery waned in 2007 (shown in yellow and also the first six of the series shown in red) before the onset of that recession.

The manufacturing workweek, an element of the Index of Leading Economic Indicators, declined 0.3 hours to 40.7. That is a large decline and is consistent with manufacturing rolling over from weakness. Another leading part of the report, temporary jobs, also declined by 7,500 (completely contrary to the ASA survey's strong increase).

The punk report was based on weakness throughout the service economy, but especially two areas. Comparing January with March, retail jobs went from +24,900 to -33,800. Professional and business services went from +79,000 to +31,000. Those two areas alone are responsible for 106,000 in the shortfall in job creation.

The index of Aggregate hours worked in the economy, [which were revised higher for February, fell 0.2 from 96.0 to 95.8 -- NDD note. This original line is in error.] did increase 0.1%, in line with actual payrolls. This is a notable coincident indicator consulted by the NBER.

The general workweek declined by 0.1 hour to 34.5. Overtime was unchanged. Hourly earnings rose $0.05 to $23.39, a 0.2% increase.

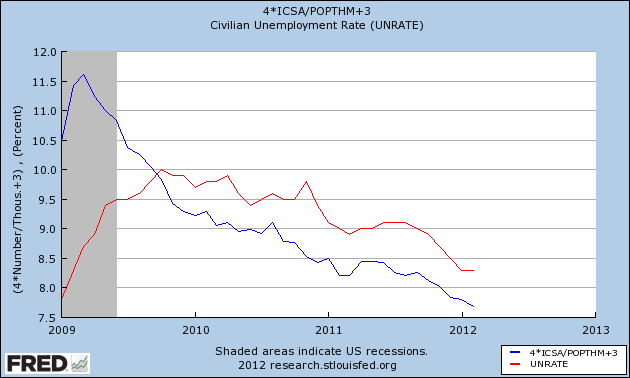

The only relatively bright spot was the unemployment rate, which did fall from 8.3% to 8.2%, as predicted from the initial jobless claims data, since that leads the unemployment rate (note the graph below does not include this morning's data):

The broad U6 unemployment rate fell from 14.9% to 14.5%. Some of this was due to the -0.1% decline in the employment to population ratio. Since the unemployment rate is a lagging indicator, this isn't terribly heartening.

It may be that some job growth was pulled forward due to the non-winter winter, but between the declining leading indicators in the report, and the break in trend with initial claims, this report has to be regarded as a serious piece of evidence that high gas prices, wages that have not kept up with inflation, and weaker manufacturing growth are finally extracting a toll.