In the rear view mirror Q4 2011 GDP was revised up to 3.0%. Monthly releases were sharply mixed with some significant advances and some jarring declines. Consumer confidence was up strongly to a near 1 year high. This is a large component of the Conference Board's revamped LEI. Residential spending continued to increase. Vehicle sales were up sharply to nearly a 4 year high. The Chicago PMI increased strongly as well. On the other hand, the ISM manufacturing index unexpectedly fell, although still showing expansion. Personal income and spending were up only weakly. Personal consumption expenditures were flat for the fourth month in a row. Nonresidential construction spending fell. Durable goods fell strongly in January, wiping out December's similar increase and then some.

I watch the high frequency weekly indicators because, even if there is more noise, if there is a turning point, it will show up in these indicators first. In addition to the chronic issue of gasoline costs, with one or possibly two exceptions, no such turning point is evident.

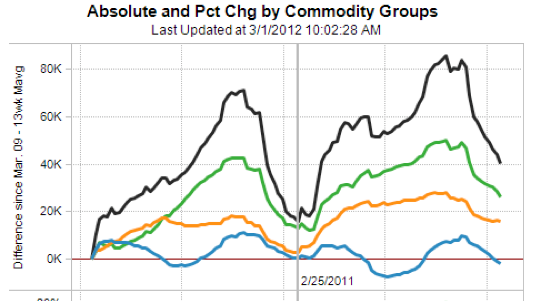

Let's turn first to the negative statistic. The American Association of Railroads reported a decline in weekly rail traffic for the week ending February 25, 2012, with U.S. railroads originating 281,644 carloads, down 5 percent compared with the same week last year. Intermodal volume for the week totaled 214,402 trailers and containers, down 2.8 percent compared with the same week last year. Last week I noted that Railfax is back with some free graphs. One of them is particularly helpful in interpreting the recent swings in the AAR weekly reports. Here is a graph of the 13 week average of carloads for the last two years (black=total, green = intermodal, orange = cyclical, blue= baseline):

The YoY comparisons may have been decidedly erratic this winter because of the batch of winter storms that hit in 2011, skewing weekly comparisons. The Railfax graph shows that rail traffic continues to trend higher on a YoY basis measured over 13 weeks. If this graph does not begin to turn up in the next few weeks, we'll know that we have a problem. Until then, the jury is out.

Employment related indicators were neutral to positive:

The Department of Labor reported that Initial jobless claims remained at 351,000 last week. The four week average declined by 5000 to 354,000. This is the lowest reading since spring 2008.

The American Staffing Association Index fell by 1 to 86 last week. It remains almost midway between its levels of 2011 and 2007. Seasonally we want to see this move slightly higher over the next 4 weeks.

The Daily Treasury Statement showed that for the 20 reporting days of February 2012, $158.3 B was collected vs. $144.9 B for February 2011. Because this year had one more day of reporting than last year, the reports are not truly comparable. For the 20 reporting days ending Wednesday March 2, 2011, $154.9 B was collected, meaning the most comparable 20 day increase this year was +2.2%. This is positive but quite weak.

Gasoline prices are more than 10% higher than one year ago while usage continues to be much lower: Oil fell about $2 this week to close at $106.70. Gas at the pump rose another $.13 to $3.72. Both of these are significantly above the point where they can be expected to exert a constricting influence on the economy. Gasoline usage, at 8363 M gallons vs. 9162 M a year ago, was off -8.7%. This is one of the weakest weekly comparisons since the YoY declines began last March. The 4 week moving average is off -6.7%.

Housing reports were positive:

The Mortgage Bankers' Association reported that the Refinance Index decreased -2.2% from the previous week, still close to its highest level in over half a year. The seasonally adjusted Purchase Index increased +8.2% from the prior week, and was -4.8% lower YoY. This is a rebound from the bottom of its 21 month overall flat range.

YoY weekly median asking house prices from 54 metropolitan areas at Housing Tracker were again up +4.1%. This number has stabilized on a YoY basis in the last month, which is what I would have expected. I expect this series to continue positive, but it will be interesting to see if it drifts lower as we hit the peak selling season. It remains at odds with the Case-Shiller reports of worsening YoY declines in price for comparable sales. One of the two is going to turn.

Sales remained positive. The ICSC reported that same store sales for the week ending February 25 were off -1.0% w/w, but increased 2.7% YoY. Shoppertrak reported +2.8% YoY gains. Johnson Redbook reported a 3.4% YoY gain. These reports have taken on added significance. If the consumer is beginning to fold, I would expect to see YoY comparisons under 2% as a warning signal. There's no such signal yet.

Money supply was mixed and Credit spreads narrowed:

M1 declined -0.3%t last week, but was up +0.1% month over month. On a YoY basis it fell to +18.6%, so Real M1 is up 15.7%. YoY. M2 fell -0.1% week over week, but was up +0.3% month over month. It was up 10.0% YoY, so Real M2 was up 7.1%. In short, real money supply indicators continue strongly positive on a YoY basis, although not so much as in previous months.

Weekly BAA commercial bond rates were flat at 5.15%. Yields on 10 year treasury bonds rose .04% to 2.01%. The credit spread between the two, which had a 52 week maximum difference of 3.34% in October, tightened again this past week to 3.14%. Narrowing credit spreads are not at all what I would expect to see if we were going into a recession.

Finally, the JoC ECRI industrial commodities index continued to increase, from 127.52 to 128.13. This is almost certainly the most heavily weighted component of ECRI's WLI, and is consistent with an increase in that index again next Friday.

Turning now to high frequency indicators for the global economy:

The TED spread is at 0.410 down from 0.420 week over week. This index is back slightly below its 2010 peak, and has declined from its 3 year peak of 2 months ago. The one month LIBOR is at 0.243, down .002 from one week ago. It is well below its 12 month peak set 2 months ago, remains below its 2010 peak, and ihas now completely returned to its typical background reading of the last 3 years.

The Baltic Dry Index at 771 was up 54 from 717 one week ago, and up 121 from its 52 week low of 3 weeks ago, although still well off its October 52 week high of 2173 (please note that even so this is nothing even remotely close to its decline during the Great Recession. This type of decline has happened 4 times since March 2009 without triggering any "double dip."). The Harpex Shipping Index rose by 1 to 376 in the last week, off of its 52 week low. Please remember that these two indexes are influenced by supply as well as demand, and have generally been in a secular decline due to oversupply of ships for over half a decade. The Harpex index concentrates on container ships, and led at recent tops and lagged at troughs. The BDI concentrates on bulk shipments such as coal and grain, and lagged more at the top but turned up first at the 2009 trough.

Just like last year, I believe that Oil's choke collar is beginning to be felt. Nevertheless, the overall tone remains positive for now. Weekly retail sales reports and gasoline usage have assumed increased importance as warning signals for any further deterioration.

Have a nice weekend.