In case you haven't already seen it, this video clip of CNBC anchors Jim Cramer and Simon Hobbs getting into a heated argument on-air about European banks has been going viral:

Hobbs, Cramer, and Carl Quintanilla actually seemed to be in "violent agreement." Here are a few snippets of dialogue:

Cramer:

"We have a Lehman situation"

"people are trading as if it is [a Lehman situation]"

Hobbs:

"We do not have a Lehman-like situation. We have the fear that there may be a Lehman situation at the moment."

"That is not going to happen here, at this stage" (my emphasis)

"We're not about to have a European bank hit the wall"

Quintanilla (trying to be a peacemaker):

"It may be a fat-tail risk, but it is a risk"

In other words, all three actually agree that while there is no European bank failing right now, there is a non-trivial and indeed significant chance that there could be a major European bank failure with systemic risk in the coming days/weeks/months. More to the point, Cramer says that people are trading as if that is the case.

There's one more quote I'm going to come back to, because I believe it perfectly encapsulates the situation.

But being the nerd that I am, let's go look at some pertinent data. First of all, if there were a substantial systemic risk to finance right now, then bankers should be charging more for counterparty risk, in particular when they loan other banks overnight money. It ain't happening. Here's LIBOR:

and here's EURIBOR:

As I first said a couple of weeks ago, Where's the fear? Why don't the front line troops in the trenches share the trepidation of the pinstriped strategists in the rear?

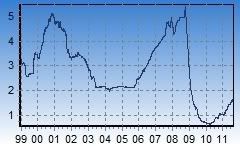

Now here is Barron's graph from Saturday's edition of insider buying vs. selling:

The ratio is down to 1:3, the lowest in a year (since the much-mocked "Hindenburg omen"). Even in 2008, when insiders trading got to this level, it always signaled at least a short term bottom (e.g., when Bear Sterns failed in March, and when Fannie and Freddie were nationalized in July), and it also marked the ultimate bottom in March 2009. So the smart money sees a buying opportunity.

Well then, what is the dumb money doing? According to the Investment Company Institute:

Investors pulled the most money from U.S. mutual funds in 14 months as stocks lost ground and Congress battled over raising the nation's debt ceiling. Mutual funds suffered $16.9 billion in withdrawals in the week ended Aug. 3, up from $9.6 billion the previous week ....and then:

Investors pulled a net $40.3 billion out of those funds in the week ended Aug. 10, the largest weekly withdrawal since early October 2008, soon after the collapse of Lehman Brothers.Let me return to the video above, because Cramer, refusing to back off his "this is a Lehman situation" statement, said the following, which seems to perfectly encapsulate the zeitgeist:

"I can't give false assurances because I learned my lesson .... for people not worrying that there is a Lehman situation is to run a risk of two weeks from now seeing 'Cramer said it would not be a Lehman situation.' "In short, having been burnt in 2008, he is unwilling to take any risk of being too optimistic now. This is Pavlovian: if the stimulus looks similar to that which led to a severe shock in the past, it is resulting in behavior to attempt to absolutely ensure avoiding the shock now.

In short, "fear itself." The very same fear which appears to have caused consumer confidence to plunge to new lows. The same seizure which led to a 10% decline in mortgage applications in one week earlier this month. The same seizure that was reflected in a Philly Fed manufacturing reading that simply fell off a cliff to one of it deepest recessionary readings in 40 years.

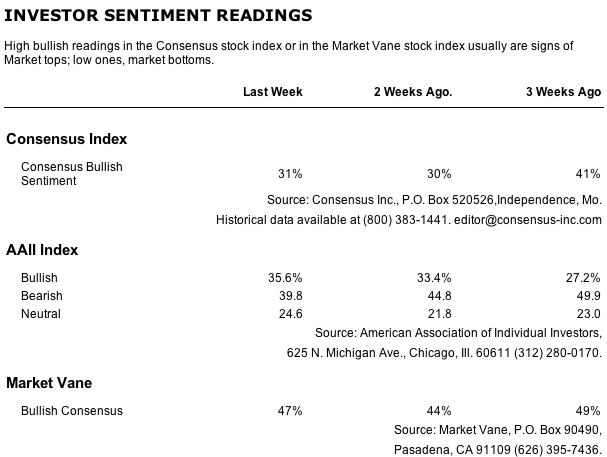

The only piece of the puzzle that doesn't quite fit, and gives me pause is investor sentiment. Here's a screenshot of that metric from Barron's over the weekend:

It seems that there is a fair amount of "buy the dip" sentiment out there - not the true panic I would want to see at a real bottom. So perhaps we have to have a severe retest. But if the front line troops and the smart money are sanguine, and the dumb money is panicking, who do you think is more likely to be right?