- by New Deal democratMost of my analysis proceeds from the view that leading indicators still lead, and lagging indicators still lag. While no approach is perfect, you will be right a lot more than most armchair (and highly-paid) pundits if you simply proceed from the premise that It Isn't Different This Time, and that while each recession, recovery, and expansion will have areas of variance from the norm (as in housing bubble and bust that still persists), in the main they will abide by past patterns. I parted from the vast majority of the doomish econoblogosphere almost a year ago when I noticed that consumers were refusing to play dead but, zombie-like, were rising from the grave to spend again, at least making a bottom in those figures. Shortly thereafter, the Leading Indicators almost all began to stabilize or even turn positive, in the face of the most severe economic downturn in decades.

As time has gone on, more and more of the bearish argument has focused on lagging indicators, and as an exercize to show that they do indeed lag and would turn positive in time, just as in prior recoveries, I have been tracking them here.

Most pointedly, back in November, Lee Adler of the Wall Street Examiner wrote a piece called

Retail Sales Data, Tell me another Joke in which he said:

The reported rise in retail sales this morning had the media had in a full throated bull chorale...But as usual it’s all hype, little substance. A dead cat bounce is not a recovery. The “recovery” the pundits are talking about is little more than a semantic game. Bernanke sounds more like Chauncey Gardener every day. If this is recovery it must be just like the “recovery” that took place in the 4th quarter of 1929 and first quarter of 1930.

Adler's piece was quickly picked up by the usual suspects, as proof that the Recovery was illusory. Now, I respect Lee Adler a lot, and in particular he was one of few non-permabears who called the September-October 2008 crash ahead of time. But the fact is that state and withholding tax collections lag. You have to have the recovery and the hiring first, before people pay taxes on their new jobs and revenues!

This was an argument I had already had last July at the place where I used to blog, when they claimed that

the worst state tax revenue declines in 46 years meant Doom was upon us. I pointed out in a comment that the bottom in revenues would come one or two quarters after the bottom in the economy, to no avail, because in January of this year, they did it again, claiming

If this is a Recovery, shouldn't tax revenue be increasing?Now we know that even before they were writing this, in the last quarter of 2009, according to an article in

Business Week, state tax revenues were indeed beginning to increase, one to two quarters after the bottom in the economy, just like I said they would:

The two-year slide in tax collections that opened a $196 billion gap in U.S. state budgets has stopped, easing pressure on credit ratings and giving leeway to lawmakers as they craft spending plans for next year.

The 15 largest states by population forecast a 3.9 percent gain in tax revenue in fiscal 2011, budget documents show. The 50 states on average may increase collections by about 3.5 percent, the first time in two years the figure is expected to grow, said Mark Zandi, chief economist at Moody’s Economy.com,

....

Combined state and local tax collections climbed to $360.1 billion during the final three months of 2009 , the first year- over-year gain in five quarters and an almost 1 percent boost from the same period in 2008, according to the agency.

....

“We’ve seen the worst,” said Philip Condon, who oversees about $9.4 billion in municipal bonds for DWS Investments in Boston. “While it may not be great, it’s getting better.”

Although getting recent, accurate state tax receipt data on the internet is fiendishly difficult, it nevertheless appears that once again, Mish unintentionally bottom-ticked an economic indicator a month ago when he highlighted the shortfall in November 2009 state revenues.

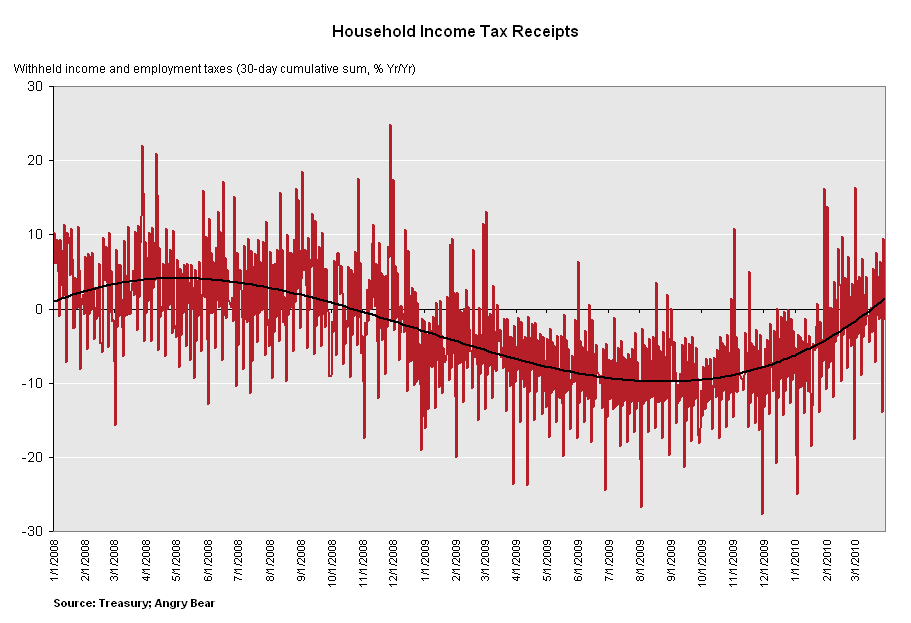

Adler's piece noted that the reporting of state tax revenue (by the Rockefeller Institute) lagged badly, usually 4 months behind the collections. So he made use of the Daily Tax Receipts (h/t

Matt Trovisonno) for more recent information, claiming that they too showed a non-Recovery. The TrimTabs mantra of poor withholding receipts comparisons had also been picked up by

others of the Doomish persuasion. But of course those taxes too are lagging indicators, and as I've been noting weekly for the last few months, the YoY comparisons kept getting better and better until this month, they finally surpassed the taxes withheld in March 2009. As I write this, with one day left of reporting, March 2010 taxes withheld are already ahead of last year, $159.2B to $156.0B (and nearly equal to the March 2008 figure of $162.6B).

Well, TrimTabs will no longer give them comfort either, because

as of yesterday they claim that the economy added between 80,000 and 130,000

non-Census jobs in March. [Note: I am not endorsing their analysis, which has been suspect in the past. The point is that in the parlance of sandlot baseball, "your own man says so."]

Leading indicators still lead, and lagging indicators still lag. It wasn't different this time. With their withholding, sales, and state revenue arguments gone or rapidly dissipating, there really is very little (bank loans, but historically those lag too) in the statistical data left for Doomsters to hold onto.