One the phrases both Bonddad and I have been using (I'm going to take credit for being first) is that in this global recovery, the American consumer is no longer the locomotive, but the caboose. In particular, China and Asia aren't growing because the US consumer has started to lighten up a little. On the contrary, all of the growth in Asia is in large part responsible for the resumption of American growth.

- "We cut way too far, so as a result we are going to have sustained jobs growth this year."I have been paying a lot of attention to ECRI because they made what was an extremely bold call in March 2009 -- namely, that the Great Recession would bottom out in summer 2009 and a recovery would start. It is easy to remember just how depressed the mood was back at that time. Yet now just about every economist who is on record believes that is exactly when the recession ended.

- "The demand is coming back not only the US but around the world. The problem is it won't be enough to make up for all the job losses for the people who are in the long term joblessless. It's not going to solve [the problem of the need to fun long term unemployment benefits]."

- "All of these [American technological] companies ... are to a degree platform companies where they own intellectual property, and they're sourcing it from around the world..... They're getting a lot of profits out of it, but they're not necessarily creating a lot of jobs out of it."

- "Business spending [is] disproportionately driving the growth.... The[ consumer] is growing at about the same pace as they have in past recoveries.....

- "Asia grew by [ ]17% [during our recession and] They are sucking up a lot of demand. We're exporting to them."

So let's briefly examine ECRI's outlook one point at a time.

1. Growth will continue:

ECRI continues to be bullish on the economy. Their Weekly Leading Index

rose to a nearly two-year high in the latest week, indicating that the recovery remains underway....said Achuthan.

....

That was the highest level since May 23, 2008....

The index's annualized growth rate fell to a 37-week low of 12.5 percent from 12.6 percent a week earlier.

However, "with the WLI rising to a 99-week high, the economic revival will continue in the months ahead,"

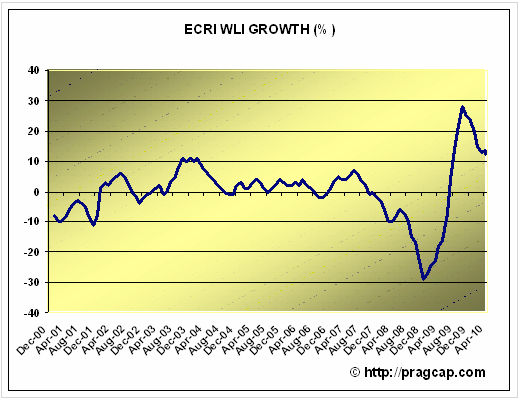

The following graph of ECRI's leading index shows that a period of torrid growth, better than anything seen in the last 20 years, is expected to throttle back to merely normal expansion as the year wears on.

[h/t Pragmatic Capitalist]

Achuthan has also said bluntly that "a double dip recession remains out of the question,"

As we already know, the other leading forecast organization, the Conference Board, said earlier this month that its Index of Leading Indicators was up 1.4% in March, and on a year over year basis was up 12%. This is the strongest reading in 20 years.

2. Substantial job growth will continue

Last September, responding to complaints by Paul Krugman among others that GDP growth wasn't good enough, that what was critical for average Americans was the issue of jobs, jobs, jobs, I came up with a series of Leading Indicators specifically for job growth.

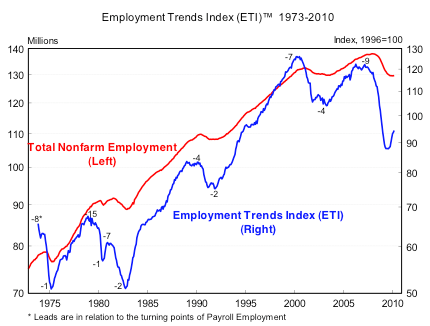

It turns out I wasn't alone. The Conference Board had been looking into the same thing, and a couple of years ago started to publish and "Employment Trends Index," which agglomerate 8 separate statistics and were back-checked 30 years. Here's how that long term graph looked at the beginning of this month:

In their report at that time they said that the Index

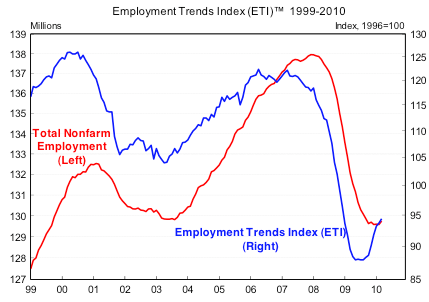

rose in March for the seventh consecutive month.... The index is up 5.5 percent from a year ago. Over the past three months, all of the index’s eight components have been improving. “The solid rise in the ETI and the widespread improvement across its components suggest that the March increase in employment was not a fluke and the economy is likely to continue to add jobs in the coming months,” said Gad Levanon, Associate Director, Macroeconomic Research at The Conference Board.Here is what a close up of the graph, covering the last few years, looks like:

As you can see, the index is rising faster than during either of the two previous "jobless recoveries" but not quite as quickly as the V-shaped jobs recoveries of 1974 or 1982.

Levanon added that “However, we do not expect job growth to significantly accelerate in the short term, as both consumption and investment growth are likely to remain relatively weak."

Since that time, we had the blockbuster March real retail sales report that I discussed last week. It will be interesting to see if the Conference Board also finds that significant for future job growth.

3. The problem of long term unemployment and underemployment

Achuthan believes that it will be impossible for a recovery, even a strong one, to replace the 8 million jobs that have been lost since 2007 (let alone dealing with population growth). Since neither political party is willing to countenance the idea of direct government employment (i.e., a new WPA), either unemployment benefits must be extended indefinetely, or else the long-term unemployed will truly fall into the abyss.

This point could not have been made more starkly by a recent study by Andrew Sum, et al,(pdf) for the C.S. Mott Foundation differentiating between the top 10% of income earners, the middle 20% and the lowest 20%. They found that among the lowest 10% of American workers, unemployment was 20.7%, and another 30.8% were underemployed. meaning that over half of all of the lowest 10% of Americans suffered some degree of employment loss. On the other hand, only 3.2% of the top 10% of Americans were unemployed, and another 1.4% were underemployed, for an overall rate of under 5%. For middle income Americans, the figures were 8.4% and 5.8% for a total rate of 14.2%.

Their conclusion: for the uppermost Americans, there has been no recession at all, but by the time you get to the bottom of the income scale, it has been a true Depression.

4. Asia is the locomotive, American wage-earners are the caboose

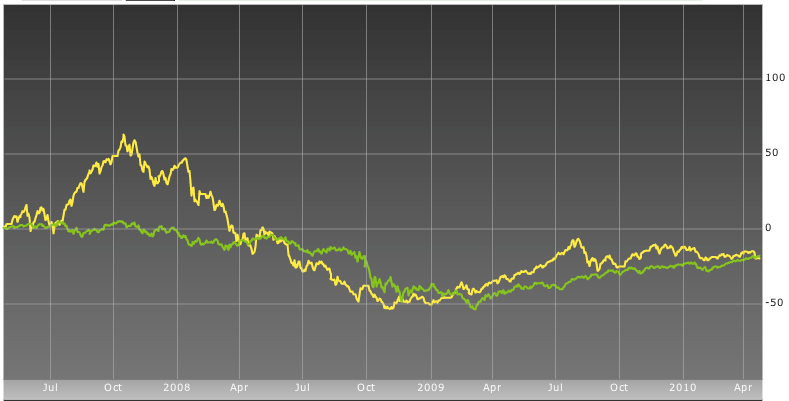

Achuthan's point that Asia is driving the global recovery makes me recall that one of the most telling indications that the baton of global economic leadership had passed, were graphs of when the various global stock markets bottomed. The US' market bottomed in March 2009, but Asian markets all bottomed about 4 months before, in November 2008. For example, here is a graph comparing China's Shanghai market (yellow) with the S&P 500 (green):

According to the IMF, the Asian locomotive is chugging ahead, as they are calling for 10% growth in the Chinese economy this year, and their exports recovering modestly:

Chinese Commerce Minister Chen Deming Friday said he remained cautious about growth of exports this year as recovery in demand for China-made goods in the United States and Europe was still very slow....

"This fair is better than the spring and autumn sessions last year. A majority of exporters reported growth in orders from overseas customers," he said.

Chen, however, warned against blind optimism about trade recovery....

The recovery in demand in major markets like the U.S. and Europe remained very slow, a sign that global demand had not recovered to pre-crisis levels ....

As the Wall Street Journal noted back in December:

"Households have now become a driver in the recovery" across the region, says Frederic Neumann, Asia economist for HSBC. He notes that consumption grew faster than overall output in most Asian economies in the third quarter, a change from earlier in the decade.

But increasing demand is producing rising costs of raw materials and labor that Chinese manufacturers called "their biggest challenge."

Meanwhile, exports at US West Coast ports are up over 10% from a year ago. To put it bluntly, since global wage arbitrage is a huge issue and has been completely unaddressed, growth in the American economy is in large part becoming increasingly poorer American workers employed by global corporations feeding the growth of increasingly richer Asian ones.

Looking ahead, the bite of near $3 a gallon gasoline among other commodities, that now has the Shanghai stock exchange going sideways for the last 6 months, is cause for particular concern for the American working/middle class that has become the caboose in the global recovery.