From the Beige Book:

Overall economic activity increased somewhat since the last report across all Federal Reserve Districts except St. Louis, which reported "softened" economic conditions. Districts generally reported increases in retail sales and vehicle sales. Tourism spending was up in a number of Districts. Reports on the services sector were generally mixed. Manufacturing activity increased in all Districts except St. Louis, and new orders were up. Many Districts reported increased activity in housing markets from low levels. Commercial real estate market activity remained very weak in most Districts. Activity in the banking and finance sector was mixed in a number of Districts, as loan volumes and credit quality decreased. Agricultural conditions were mixed as well, with positive conditions reported in Districts from the central and western parts of the country, while negative conditions were reported in the mid and southern Atlantic Districts. Mining and energy production and exploration increased for metals, oil and wind.

While labor markets generally remained weak, some hiring activity was evident, particularly for temporary staff. Wage pressures were characterized as minimal or contained. Retail prices generally remained level, but some input prices increased.

Let's look at more detail:

District reports indicated that consumer spending increased during the reporting period. New York and Cleveland reported that recent sales strengthened, while sales rebounded in Richmond and Kansas City. Slight sales gains were reported in Philadelphia. Retail sales in San Francisco continued to improve, but remained somewhat sluggish on net. In St. Louis several new establishments opened, particularly in the food industry. Several Districts described consumers as somewhat more confident. Businesses were cautiously optimistic regarding future sales: Cleveland, Atlanta, Kansas City and Dallas noted that retailers expect sales to improve during the upcoming months. Sales of home furnishings and electronic goods increased in a number of Districts, while seasonal apparel sales were up in New York, Philadelphia and Kansas City. New York and Minneapolis noted that shopping by Canadians was strong at businesses near the border. Atlanta reported that retailers continued to keep inventory levels lower than normal, and retailers in New York reported that inventories are in very good shape.

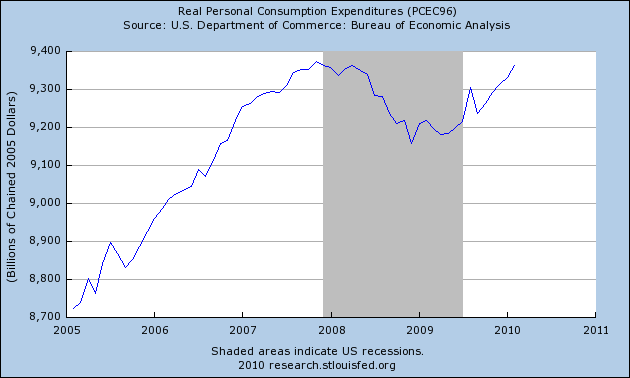

Let's look at the data:

Real PCEs have been increasing since the first quarter of 2009.

Service expenditures -- which account for over 60% of consumer expenditures -- never really decreased but instead were put into a holding pattern. However, they have now started to increase.

Increases in non-durable expenses started to increase right near the end of the first half of 2009.

Durable goods expenditures are still stuck in a rut. However, these comprise the smallest part of PCEs.

Business services were mixed, with some signs of economic recovery. Boston and Minneapolis reported increased activity. Richmond and Dallas were mixed, while San Francisco said demand remained lackluster. St. Louis reported that the sector continued to decline. Advertising and consulting firms in Boston said demand is up substantially from the first quarter of 2009, while an advertising contact in Richmond and professional media services firms in San Francisco characterized sales as flat at low levels. Dallas reported sluggish demand for nontax-related accounting and legal services. Law firms in Minneapolis specializing in debt collections and bankruptcy saw strong demand, while a Richmond property manager noted a large number of repossessions.

Here is a chart of the ISM services index:

Notice this bottomed out in late 2008 and has been rising since. The number is now above 50 indicating expansion.

Manufacturing activity increased since the last report across most of the country, with all Districts other than St. Louis reporting increases in orders, shipments, or production. Boston, Cleveland, Chicago, Dallas and San Francisco reported positive results in metals and fabrication. Cleveland, Richmond, Atlanta and Chicago reported increased auto or auto component production. Boston, Richmond, Dallas, and San Francisco saw increased production in electronic, computers or high-technology goods. Chicago and Minneapolis saw increased production of energy-related products. However, for construction-related goods, Chicago and Dallas reported mixed conditions, Boston reported flat activity and St. Louis reported decreases. Overall, St. Louis saw more plant closures than plant openings.

Here is a chart of the overall ISM manufacturing index:

This number has rebounded sharply since the end of 2008.

Overall industrial production bottomed in mid-2009 and has been rising since, as has

Bank lending activity was mixed by category in most Districts. Atlanta, St. Louis and Kansas City saw weaker loan demand across categories, while activity in San Francisco was flat at low levels and Dallas said that demand appears to be stabilizing. Demand for consumer credit decreased in New York and increased slightly in Philadelphia. Most banks in Cleveland reported weak consumer loan demand, although a few contacts saw a slight increase due to seasonal factors. Business and industrial loan volumes decreased in Philadelphia, Cleveland and Chicago and were flat in New York. San Francisco noted continued modest gains in venture capital funding.

Consumers are engaged in a massive drop in credit. We've seen consumer credit drop for the majority of last year. In addition, consider this chart of total bank credit outstanding:

Notice this figure has been dropping since before the end of 2009. In addition, consider these charts from the latest senior loan officer survey:

All point to weaker loan demand as a factor for the decrease in loans.

Residential real estate activity increased, albeit from low levels, in most Districts, with the exceptions of St. Louis, where it was mixed, and San Francisco, where it was flat. Contacts in Philadelphia, Cleveland and Kansas City expressed concern about whether sales would continue to grow after the expiration of the first-time home buyer tax credit. New York, Kansas City, Dallas and San Francisco noted sluggish sales for high-end homes. Home prices were stable across most Districts, but decreased in parts of the New York and Atlanta Districts. Residential construction activity increased slightly in New York, Atlanta, St. Louis, Minneapolis and Dallas, but remained weak in Cleveland, Chicago and San Francisco.

Let's look at the new and existing home market with charts from Calculated Risk.

Existing home sales have fallen back to levels seen in 2008 and 2009.

While the inventory is still decreasing, it did spike up last month. In addition,

In addition, the months of supply available at the current sales pace moved higher last month.

The new home sales chart tells us that sales are still very low, absolute inventory is back to more "normal" levels, but the months available at the current sales pace is again increasing, which is not a good sign.

As for construction spending (also from Calculated Risk):

We're still at low levels.

A complete review of the latest employment numbers is here.

Short version: things are looking pretty good right now.