In accordance with usual practice, the U.S. Bureau of Labor Statistics is announcing its preliminary estimates of the upcoming annual benchmark revision to the establishment survey employment series. The final bench- mark revision will be issued on February 5, 2010, with the publication of the January 2010 Employment Situation news release.

Each year, the Current Employment Statistics (CES) survey employment estimates are benchmarked to comprehensive counts of employment for the month of March. These counts are derived from state unemployment insurance tax records that nearly all employers are required to file. For national CES employment series, the annual benchmark revisions over the last 10 years have averaged plus or minus two-tenths of one percent of total nonfarm employment. The preliminary estimate of the benchmark revision indicates a downward adjustment to March 2009 total nonfarm employment of 824,000 (0.6 percent).

Table B shows the March 2009 preliminary benchmark revisions by major industry sector. As is typically the case, many of the individual industry series show larger percentage revisions than the total nonfarm series, primarily because statistical sampling error is greater at more detailed levels than at a total level.

A few points about this revision. Economic statistics are revised all the time for plenty of reasons. But the big reason is more data becomes available over time. This is standard in economic statistics land. It does not mean the staff of the BLS is involved in a secret plot to cover-up the severity of the recession in order to quell the masses into sleep. It does mean the severity of the economic situation played havoc with everybody including those who compile government statistics.

Secondly, this also does not mean that the unemployment rate will spike up an additional amount when these numbers are added to the survey on February 5, 2010. The unemployment rate is derived from the household report. This was a change to the establishment survey. The two are separate and distinct economic reports; they have nothing to do with one another.

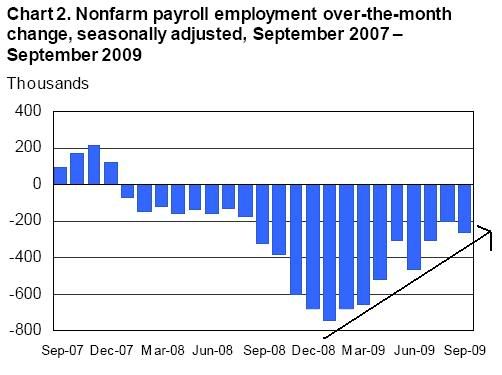

Now, let's turn to the data, especially this chart:

This is from the latest unemployment report and it shows the number of jobs lost per month over the last few years. Pay particular attention to the November - March period when the rate of job losses was over 600,000/month (and in one case was over 700,000). Now we've learned that there were in fact more job losses. In other words, the rate of decline was that much more severe. That leads to a very important conclusion: it's going to take longer for the jobs market to heal.

The primary argument against recovery has been the jobs market. While there are numerous economic indicators that signal the economy is rebounding (here is a list of over 20) there is one that stands out like a sore thumb: jobs. However, those arguing against the idea the economy is recovering do not note that an economy the size of the US's does not simply turn on a dime. When an economy loses over 2.4 million jobs in a 4 month period (as originally thought), it does not turn around and start growing anytime soon. Now we've learned that the severity of job losses was in fact more severe. This means the period from the time of job losses to recovery is in fact longer than originally thought. Additionally -- and just as importantly -- the unemployment rate is a lagging indicator. That means it goes down after the economy starts growing. So to talk of a "jobs recovery" when the economy is still in negative territory (although it will probably print a positive GDP in the third quarter) is premature at best. Simply put, it's not time to talk about a jobs recovery yet.

In other words given the increase in the number of expected job losses, the pace of the decline in the rate of job losses, and the numerous indicators signaling recovery, "recovery on".

Now, let's add another piece to this discussion:

The bleak September jobs report appears to have cracked the political logjam blocking progress on a third stimulus package.

I'm not going to speak to the politics of this. That's for people who actually enjoy that sort of discussion. (Personally I have come to loathe all politicians, whatever stripe) What I can say is this could be a good idea if done properly.

There were two arguments against the first stimulus: it didn't put enough money into the economy fast enough and the method of the stimulus -- which was a combination of tax credits and direct injections -- should have been more weighted more towards straight injections.

Regarding the first point Washington responded there weren't enough "shovel ready" projects. I can't speak to the veracity of this claim. However, I also think the decision was just as much political as it was economic. Washington wanted to inject money into the economy during the 2010 elections so they could say "look what I'm doing for you." However, in retrospect I think spreading the payments out over time is a good idea given the severity of the downturn and the difficulty the economy will have in coming out of the hole it's in.

Regarding the second method, the primary argument against tax credits was it would not go to spending but instead to debt reduction. In other words, the money would not get out in the economy helping it to grow. This was the experience with the Bush rebate checks; there was little reason to think the result would be different with the second round of tax cuts. And, in general, consumer spending has bottomed but not grown at a strong pace since the beginning of this year. But we have seen a large pay down in consumer debt. In other words, consumers are using some of the money they are getting from the government to pay down consumer debt. That is a good thing in the long-term.

However, more money, strategically spent on specific projects would be a good idea. But it must be done properly. By properly, I mean it needs to be narrowly focused on one specific area: job creation as quickly as possible. In addition, this can't be a large bill. There just isn't a lot of room in the national debt package right now. My guess is at the most we can afford another $250 billion at the most.