In this, the third installment, I'm going to examine Industrial Production, and duration of Unemployment - the first of which gives a very brief leading signal, and the second of which appears to be of only limited value -- before I get to "the Holy Grail" in part IV.

Industrial Production, which was just reported yesterday morning, is probably the single most important marker of the end of recessions. It tends to make a clean "v" in graphs right at the end of recessions. This is not a coincidence since the NBER makes use of it in their determination.

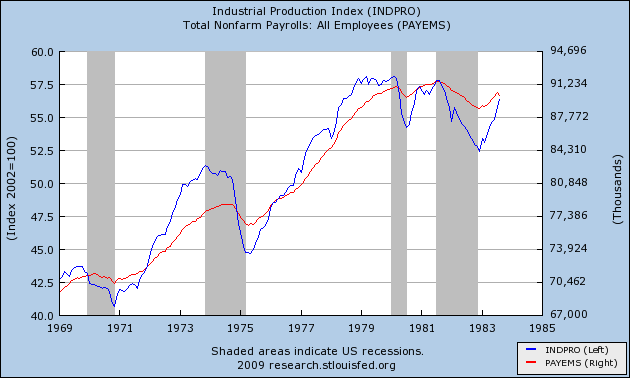

As compared with payrolls, however, industrial production does have a slightly leading characteristic. It tends to peak a median +2 months before payrolls, and to trough at the end of recessions a median +1 month before payrolls. In particular, of the 10 troughs since World War 2, in 8 of them industrial production troughed within 2 months of the payrolls number. For example, here is the graph of the two series for the 1970s recessons:

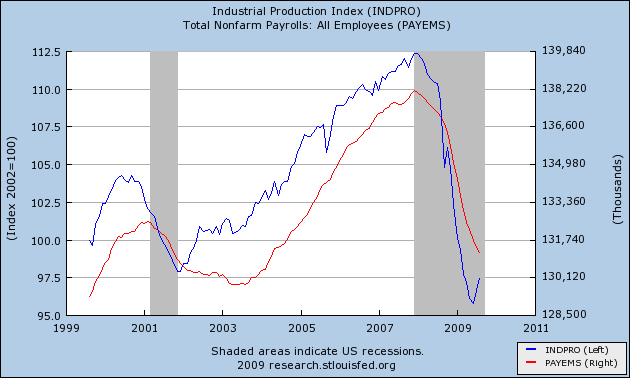

The most notable exception, of course, was 2002-3, when production troughed a full 20 months before payrolls, as shown here, along with our present recession/recovery:

Without more, at best we can say that the odds are nevertheless quite good, historically, that the trough in jobs will be within 2 months of the trough in industrial production -- which would mean the economy should start to produce actual job growth this month!

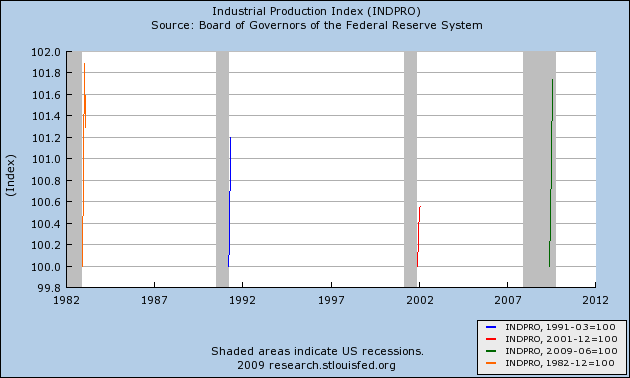

Fortunately, there is some further guidance, because the only times that industrial production has led employment growth by a relatively long period of time, it has also shown weak growth -- less than 5% a year. In more typical V shaped job recoveries, it has grown at a rate of 10% or more a year. Here are two graphs, the first showing the rate of industrial production growth in the 1953, 1992, 2002, and present recoveries two months after their trough:

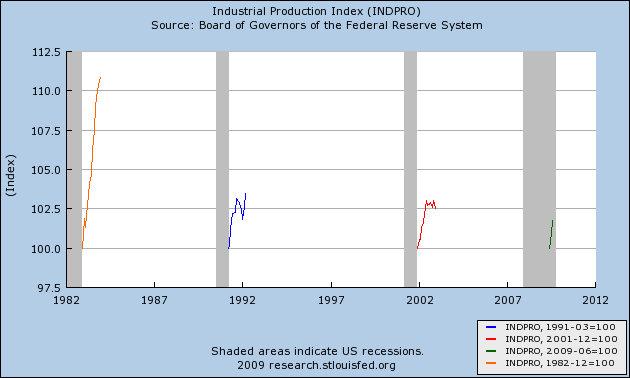

and here is the same graph extended one year for the prior three recoveries:

As of today, industrial production is up 1.8% in the last two months, and looks more like the 1983 V shaped job recovery than the two subsequent "jobless" recoveries. Should it continue to increase at a similar rate in the next month or two, that would correlate very well with past instances of V shaped job recoveries.

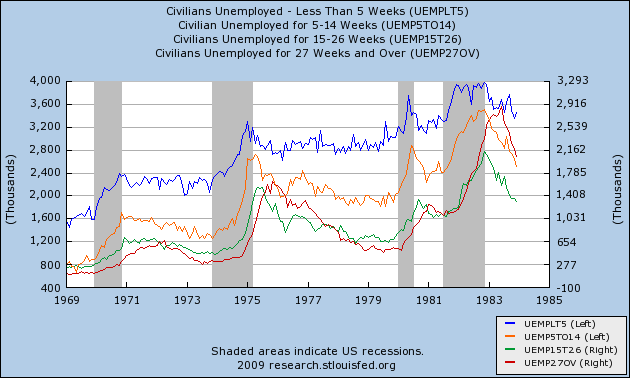

Various durations of unemployment are reported monthly together with payrolls. As I have mentioned before, the shorter the duration, the more it leads; the longer the duration, the more it lags, as shown for example in this graph (first blue, then orange, then green, then red):

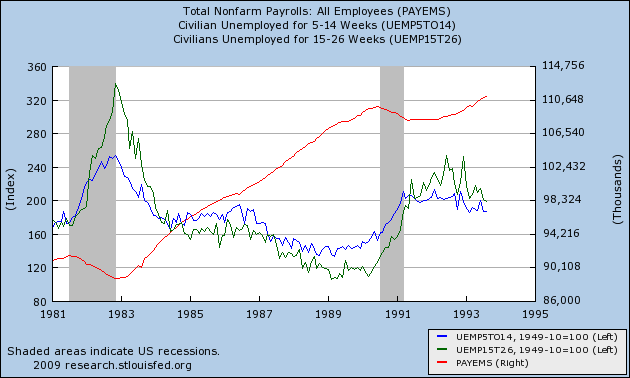

An examination of jobs data shows that it always troughs at or after the peak in the 5-14 duration weeks' employment data, but coincident with or slightly before the 15-26 week data, as shown for example here for the 1982 and 1991 recessions:

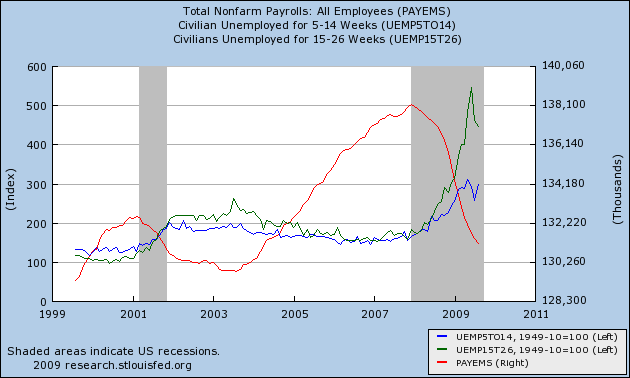

and here for the 2001 and present recession/recoveries:

Given that the interval between the peaks in the two series can be long, as it was in 2002-3, the series is of very little help. Both durations of unemployment data tend to become very "saw-toothed" as they approach and then recede from their peaks. The biggest pre-peak sawtooth in the 5-14 week data is 10%. Since we have already declined about 18% in that series before the recent upward move, that series has probably already peaked. But we have only declined about 7.5% from the peak in the 15-26 month data, which in the past has had a pre-peak sawtooth of 15%. At best, if we get a drop of more than 15% in that data, it might give us one month's lead on the trough in the jobs data.

Tomorrow (hopefully), I will discuss "the Holy Grail", the data series which almost infallibly gives a significant and relatively constant lead time for peaks and troughs in jobless claims, and also reliably indicates peaks in unemployment as well.