In any event, the weakness in housing will continue to be a drag on overall economic activity into the first half of next year, with the effect gradually waning as the year progresses. But I seriously doubt it will be enough of a drag to tip the economy into recession. My doubts stem from the fact that residential investment accounts for 6 percent of GDP, while household consumption accounts for 70 percent, and the outlook for that spending looks quite strong right now. For the first three quarters of this year, consumer spending has increased at a healthy 3.4 percent annual rate, and it looks like the fourth quarter will see something similar. That growth in spending has been underpinned by a strong labor market and solid income growth. Labor markets are fairly tight, overall, as indicated by the 4.5 percent unemployment rate. Real disposable income increased at a strong rate in the third quarter, and there are signs that real wage gains are improving — wages and salaries, as measured by the employment cost index, increased at a 3.8 percent annual rate in the second and third quarters, the best two-quarter increase in almost five years.

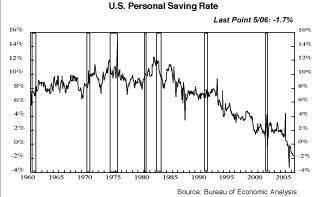

Here's the rub with that statement. It is typical of economists talking about the US economy. Because consumer spending accounts for 70% of GDP growth economists are always talking about consumer spending. But no one -- and I mean no one -- is ever talking about saving. More importantly, no one is talking about the fact that personal consumption expenditures come at a current cost of a negative savings rate. Here is a chart of the US savings rate.

This is bad. This is very bad. Every time I have brought this up in discussion with a more conservative economists, the standard refrain is "this calculation is wrong." Instead, they use household net worth from the Fed's Flow of Funds statement. But this figure has a ton of unrealized capital gains which are subject to market fluctuations. In addition, other studies conducted on the US savings rate confirm the US is indeed a poor savings country.

In Bernanke's world, it's all OK because there is a global savings glut. The problem with this theory is 1.) it does nothing to address the current US problem of negative savings, and 2.) the "global savings glut" is caused by a decrease in Asian investment at the beginning of the 21st century. When Asian economies return to their standard level of investment, the "global savings glut" will go away.

In other words, the lack of US savings is a huge issue that the US should be addressing but isn't.