Saturday, May 6, 2017

Weekly Indicators for May 1 - 5 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

Despite some flat or faltering monthly data, we are down to only 3 negative high frequency indicators.

Friday, May 5, 2017

Just How Economically Clueless is Ed Morrissey? Pretty Darn Clueless

Once again, ol' Ed has written about the jobs report. And, as usual, he complains about the "status quo" job growth that is unimpressive.

Overall, this looks like pretty good news, but not spectacular and probably not a sign of a coming boom — yet, anyway. Excluding the big miss in March, it’s the weakest report in 2017 by a slight amount, and not a large amount over the maintenance rate for population growth (~125-150K). It’s certainly better than last month, and better than the last quarter of 2016, but it’s not gangbusters

But that's not what the averages say:

Overall, this looks like pretty good news, but not spectacular and probably not a sign of a coming boom — yet, anyway. Excluding the big miss in March, it’s the weakest report in 2017 by a slight amount, and not a large amount over the maintenance rate for population growth (~125-150K). It’s certainly better than last month, and better than the last quarter of 2016, but it’s not gangbusters

But that's not what the averages say:

The chart above shows the average 3, 6 and 12 month rate of change in total establishment jobs. The current pace has gone on longer than the Bush expansion (which I'm sure Ed argued was the greatest thing since sliced bread) while maintaining a similar pace. The current expansion's levels are slightly below the pace of the previous 2 expansion.

So, we know (once again) that Ed really doesn't know much about economics. But that wont' stop him from writing about.

Scenes from the employment report

- by New Deal democrat

As I described in my detailed post on the April jobs report, below, almost everything moved in the right direction, and significantly so. Let me lay out a few graphs to show the longer-term stronger and weaker points.

In the good news department, the U6 underemployment rate has been falling at a good clip in the last few months, and at 8.6%, is about 0.6% from representing a reasonably "full" employment situation:

Part of the U6 calculation is those employed part time for economic reasons. This isn't down to normal yet, but continues to make good progress:

What is particularly good news is that both the U3 and U6 un- and under-employment rates are falling, even though people in the prime working age demographic are coming off the sidelines in substantial numbers:

The only other times in the last 30 years there has been a 1%+ increase in prime age labor force participation (red line above) were 1988 and 1995.

This *relatively* stout increase in participation is probably an important reason why nominal YoY wage gains for nonsupervisory workers have stalled:

This *relatively* stout increase in participation is probably an important reason why nominal YoY wage gains for nonsupervisory workers have stalled:

Finally, we still have about 1 million or more people who aren't even bothering to look for work, but would like a job now:

This equates to roughly 0.7% of the prime age population.

In sum, we still need to move this +0.7% off the sidelines and into actual employment, and also add another +0.6% or so from underemployment to complete employment before we can say that the the economy is operating at "full employment." And we are almost 8 years out from the beginning of this expansion, and probably a lot closer to the beginning of the next downturn. This is simply not an economy that in secular terms is working for the average American.

In sum, we still need to move this +0.7% off the sidelines and into actual employment, and also add another +0.6% or so from underemployment to complete employment before we can say that the the economy is operating at "full employment." And we are almost 8 years out from the beginning of this expansion, and probably a lot closer to the beginning of the next downturn. This is simply not an economy that in secular terms is working for the average American.

April jobs report: a blowout -- except (sigh) for wages

- by New Deal democrat

HEADLINES:

- +211,000 jobs added

- U3 unemployment rate down -0.1% from 4.5% to 4.4%

- U6 underemployment rate down 0.3% from 8.9% to 8.6%

Here are the headlines on wages and the chronic heightened underemployment:

Wages and participation rates

- Not in Labor Force, but Want a Job Now: down -74,000 from 5.781 million to 5.707 million

- Part time for economic reasons: down -281,000 from 5.553 million to 5.272 million

- Employment/population ratio ages 25-54: up +0.1% from 78.5% to 78.6%

- Average Weekly Earnings for Production and Nonsupervisory Personnel: up $.06 from $21.90 to $21.96, up +2.3% YoY. (Note: you may be reading different information about wages elsewhere. They are citing average wages for all private workers. I use wages for nonsupervisory personnel, to come closer to the situation for ordinary workers.)

Holding Trump accountable on manufacturing and mining jobs

Trump specifically campaigned on bringing back manufacturing and mining jobs. Is he keeping this promise?

Trump specifically campaigned on bringing back manufacturing and mining jobs. Is he keeping this promise?

- Manufacturing jobs rose by +6,000 vs. the last severn years of Obama's presidency in which an average of 10,300 manufacturing jobs were added each month.

- Coal mining jobs rose by +200 vs. the last severn years of Obama's presidency in which an average of -300 jobs were lost each month

The more leading numbers in the report tell us about where the economy is likely to be a few months from now. These were positive with one exception.

- the average manufacturing workweek rose +0.1 from 40.6 hours to 40.7 hours. This is one of the 10 components of the LEI.

- construction jobs increased by +5,000. YoY construction jobs are up +173,000.

- temporary jobs increased by +5,800.

- the number of people unemployed for 5 weeks or less increased by +1,000 from 2,334,000 to 2,335,000. The post-recession low was set nearly 18 months ago at 2,095,000.

Other important coincident indicators help us paint a more complete picture of the present:

- Overtime fell -0.1 from 3.3 to 3.2 hours.

- Professional and business employment (generally higher- paying jobs) increased by +39,000 and is up +612,000 YoY.

- the index of aggregate hours worked in the economy rose by 0.5 from 106.3 to 106.8

- the index of aggregate payrolls rose by +0.7 from 132.8 to 133.7 .

Other news included:

- the alternate jobs number contained in the more volatile household survey increased by +156,000 jobs. This represents an increase of 2,128,000 jobs YoY vs. 2,237,000 in the establishment survey.

- Government jobs rose by +17,00.

- the overall employment to population ratio for all ages 16 and up rose +0.1% from 60.1% to 60.2 m/m and is up +0.5% Yo Y.

- The labor force participation rate fell -0.1% m/m and is up +0.1% YoY from 62.8% to 62.9%.

SUMMARY

This was an excellent report in almost all respects. Not only were the headlines very positive, but so were most of the internals. Hours rose, aggregate payrolls rose, and the employment to population ratio continue to rise as well. People are coming off the sides maybe not in droves but pretty vigorously -- and they are finding jobs. Involuntary part-time employment is declining sharply.

There were a few pockets of softness, in short-duration employment, which hasn't made a new low in 18 months, and those outside of the labor force but who want a job, which also hasn't made meaningful progress in nearly 4 years (although recently it has declined sharply as well). The labor force participation rate also declined this month.

The other soft spot remains wages, which are only up +2.3% in nominal terms for nonsupervisory workers. This is probably in part due to the YoY increase in prime age participation (up over 1% from ages 25-54 in the last year), which means more competition for available jobs.

So, while this month is very good news, we are still at least 0.5%, and probably more like 1%, from reasonably "full" employment, and wages are still really soft. I will repeat, as I do every month now, that the biggest danger I see in the next downturn, whenever it hits, is that we have the first actual wage deflation since the 1930s.

Postscript: Is this employment report an affirmation of Trump and the GOP? Yes -- if by that you mean that they haven't really done anything to affect the economy as of yet, and so it continues on autopilot.

Thursday, May 4, 2017

Holding Trump to account on manufacturing and mining jobs: setting the benchmarks

- by New Deal democrat

Tomorrow is the April employment report, and at this point we can begin to hold Trump and the GOP Congress at least somewhat (but not fully for about 3-6 more months) accountable for the trend. For example, by this point 8 years ago, Obama and the Democratic Congress had passed the stimulus program, and the hemorrhaging of jobs, while continuing, gradually lessened before completely turning around 9 months later.

On the campaign trail last year, Trump made some pretty specific promises to bring back both manufacturing and mining jobs. Those promises were a major part of his economic appeal to the working class. So, beginning tomorrow, it's time to start holding him to account.

Today let's set the benchmarks. As noted above, the economy finally started to add jobs at the beginning of 2010. So let's calculate how many jobs were gained or lost in the Obama recovery, as a monthly average, for those 7 years.

Here is the Obama record on manufacturing jobs annually beginning in 2010:

In December 2009, 11.475 million people were employed in manufacturing. eighty-four months later, in December 2016, 12.343 million people were, for a gain of 868,000, or 10,300 a month.

Now here his the Obama record on coal mining jobs annually beginning in 2010:

In December 2009, 77,700 people were employed in coal mining. After rising to almost 90,000, by December 2016, only 49,700 people were so employed, for a loss of -28,000, or -300 a month.

For Trump to do better than Obama, he needs to add 11,000 manufacturing jobs a month, and simply not lose any jobs in coal mining.

For Trump to do better than Obama, he needs to add 11,000 manufacturing jobs a month, and simply not lose any jobs in coal mining.

The accounting starts tomorrow.

Wednesday, May 3, 2017

Monthly update on housing and cars

- by New Deal democrat

First of all, sorry for the lack of posting this week. Occasionally real life intrudes, and so it did for the last few days, demanding my full-time (and more!) attention. Posting should return to nearly normal.

If the consumer economy were really in trouble, the first two places I would expect to see that manifesting is in housing and cars. Now that the latest monthly results have been reported, we have an updated look.

This post is up at XE.com.

Saturday, April 29, 2017

Weekly Indicators for April 24 - 28 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com. Stagnant real wages helped make for a punk Q1 GDP report, but the nowcast and the forecast still look positive.

Friday, April 28, 2017

Two hits and a miss on GDP and wages

- by New Deal democrat

We got two pieces of good news from the GDP report this morning, and one piece of bad news for workers.

First, from the important long leading housing sector, real private fixed residential investment rose again to a new post-recession high:

This adds to the generally positive data coming out of that sector.

Second, proprietors income increased:

This is a good proxy for corporate profits, which won't be reported until next month. It isn't quite as reliable an indicator, but the two generally move in the same direction,

So the two long leading aspects of the GDP report were hits.

So the two long leading aspects of the GDP report were hits.

This miss was in the Employment Cost Index. Since this is a median measure, it is not distorted by outsized gains at the top of the distribution. While this measure rose +0.8% in the quarter, inflation increased at least as much, meaning that median real earnings were stagnant:

Had I used persoal consumption expenditures as my deflator, real wages would actually show a decline.

That inflation has been more than eating up nominal gains in wages for the last three quarters is not good news.

Wednesday, April 26, 2017

Declining positivity of background money and financial indicators

- by New Deal democrat

The supply, cost, and rationing of money and credit set the background for almost all other indicators. I take a look at what they look like now over at XE.com.

Tuesday, April 25, 2017

A high frequency indicator for credit conditions: the Chicago Fed'sFinancial Conditions Index

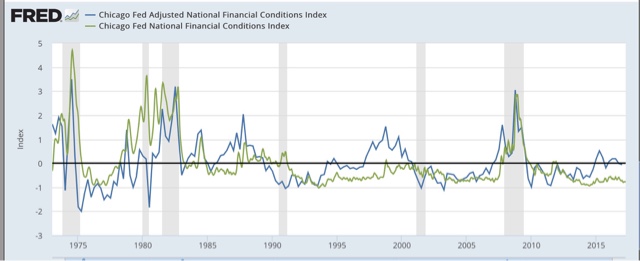

- by New Deal democrat

One particularly useful leading indicator that is handicapped by being reported only quarterly, and late, is the Senior Loan Officer Survey. This tells us whether banks have been tightening or loosening credit standards in the preceding quarter.

It has a 30 year history and has typically reported net tightening about 1 year before a recession, with a fair amount of variability, rapidly intensifying as the recession is about to start, typically showing net tightening about 1 or 2 quarters after corporate profits peak:

But the problem is, for example, that we won't learn about the first Quarter of 2017 for several more weeks. So I have been looking to find a proxy that is reported on a more frequent and timely basis. I have now found it: the Chicago Fed's Financial Conditions Index.

Here is the detailed explanation, according to the Chicago Fed:

The Chicago Fed’s National Financial Conditions Index (NFCI) provides a comprehensive weekly update on U.S. financial conditions in money markets, debt and equity markets, and the traditional and “shadow” banking systems. Because U.S. economic and financial conditions tend to be highly correlated, we also present an alternative index, the adjusted NFCI (ANFCI). This index isolates a component of financial conditions uncorrelated with economic conditions to provide an update on how financial conditions compare with current economic conditions

.....

A zero value for the NFCI can be thought of as the U.S. financial system operating at historical average levels of risk, credit, and leverage. The ANFCI removes the variation in these indicators attributable to economic activity, as measured by the three-month moving average of the Chicago Fed National Activity Index (CFNAI), and inflation, according to its three-month total based on the Personal Consumption Expenditures (PCE) Price Index. As such, a zero value for the ANFCI corresponds with a financial system operating at historical average levels of risk, credit, and leverage consistent with economic activity and inflation.

Positive values of the NFCI indicate financial conditions that are tighter than on average, while negative values indicate financial conditions that are looser than on average. Similarly, positive values of the ANFCI indicate financial conditions that are tighter on average than would be typically suggested by current economic conditions, while negative values indicate the opposite.

The NFCI is made up of over a dozen components, including 2 year Swaps and Libor vs. the TED spread, which also are components of the Conference Board's "leading credit index" that is one of the 10 components of the monthly Index of Leading Indicators.

Here is what the Financial Conditions Index, averaged quarterly, looks like compared with the Senior Loan Officer Survey:

This is a pretty close match, except that the Senior Loan Officer Survey's crossover point between tightening and loosening equates to a -0.5 reading on the NFCI.

When we compare the Adjusted Financial Conditions Index with the NFCI, we see that while it is more volatile, it appears to lead by about 6 months:

What this tells us is that background economic conditions tend to move in the direction of credit standards.

What this tells us is that background economic conditions tend to move in the direction of credit standards.

Additionally, the Chicago Fed also touts the Leverage subindex of the NFCI as leading GDP:

So in the next graph we can see the AFNCI (blue) compared with the Senior Loan Officer Survey (red) and the Leverage subindex (purple):

Both the AFNCI and the Leverage subindex appear to lead the Senior Loan Officer Survey by a year or more, but are noisy as for example in 1990 and 2001, where at least one of the two had already turned negative, indicating loosening compared with economic conditions, a year before the Senior Loan Officer Survey spiked coincident with recessions.

Putting this all together, the history of the Financial Conditions Indexes suggest that a positive value of the ANFCI or the Leverage subindex, or a reading higher than -0.5 in the NFCI, correlate with a tightening of credit conditions. Values above +0.5 (as adjusted in the case of the NFCI) should put us on higher alert for a recession, and values above +1.0 signal danger, in 1-3 years in the case of the ANFCI or the Leverage subindex, or 1 year or less in the case of the NFCI.

So in the next graph we can see the AFNCI (blue) compared with the Senior Loan Officer Survey (red) and the Leverage subindex (purple):

Both the AFNCI and the Leverage subindex appear to lead the Senior Loan Officer Survey by a year or more, but are noisy as for example in 1990 and 2001, where at least one of the two had already turned negative, indicating loosening compared with economic conditions, a year before the Senior Loan Officer Survey spiked coincident with recessions.

Putting this all together, the history of the Financial Conditions Indexes suggest that a positive value of the ANFCI or the Leverage subindex, or a reading higher than -0.5 in the NFCI, correlate with a tightening of credit conditions. Values above +0.5 (as adjusted in the case of the NFCI) should put us on higher alert for a recession, and values above +1.0 signal danger, in 1-3 years in the case of the ANFCI or the Leverage subindex, or 1 year or less in the case of the NFCI.

Finally, here is a close-up of the last two years of the weekly values of the ANFCI (blue), the NFCI (green), and the Leverage subindex (purple) [In this graph I have added +0.5 to the NFCI per my comment above]:

Note that the ANFCI did reach above +0.5 for one month two years ago. But all 3 have been below zero for the last six months. This suggests that when the Senior Loan Officer Survey is reported next month, it is at very least likely to be neutral, and more likely than not will show a slight loosening of credit. In broader terms, it means that we now have a useful weekly indicator that tells us that credit conditions are not forecasting a recession.

I will begin to report this each week.

Dear Jazz: The First Thing to Do When You're Digging a Hole ...

The above picture is Jazz Shaw, who continually makes the argument that raising the minimum wage will cost jobs.

Mr. Shaw believes that a recent report published by the Harvard Business Review supports his conclusion. As I wrote, it doesn't (see here and here). But, being that Mr. Shaw is, well, dumber than a post, he'll keep making the argument. So, here's a key excerpt from a report that he claims supports his position

Our results contribute to the existing literature in several ways. First, our findings relate to a large literature seeking to estimate the impact of the minimum wage, most of which has focused on identifying employment effects. While some studies find no detrimental effects on employment (Card and Krueger 1994, 1998; Dube, Lester & Reich, 2010), others show that higher minimum wage reduces employment, especially among low-skilled workers (see Neumark & Wascher, 2007 for a review). However, even studies that identify negative impacts find fairly modest effects overall, suggesting that firms adjust to higher labor costs in other ways. For example, several studies have documented price increases as a response to the minimum wage hikes (Aaronson, 2001; Aaronson, French, & MacDonald, 2008; Allegretto & Reich, 2016). Horton (2017) find that firms reduce employment at the intensive margin rather than on the extensive margin, choosing to cut employees hours rather than counts. Draca et al. (2011) document lower profitability among firms for which the minimum wage may be more binding

Put more directly: the report that Mr. Shaw says supports his position in fact doesn't. The data -- as noted above -- says the opposite.

Now, does this matter to Shaw or the editors at Hot Air? No. They, in fact, could care less. They just know in their bones that they're right, so that's it. The above citation from the report -- which contradicts Hot Air's "analysis" -- is meaningless academic drivel written by liberal economists who are secretly in league .... you get the idea.

Monday, April 24, 2017

Sunday, April 23, 2017

A thought for Sunday: the economy is on autopilot. Pray that it stays that way

- by New Deal democrat

It's Sunday, so I get to step out from nerdy analysis, and opine as I please.

Back in 2014, when there was another GOP "wave" election in the Congress, I wrote that the silver lining was that we were at the best point in the economic cycle for it to function on autopilot for the next 24 months. In other words, almost all of the long term indicators were positive, so if all the Congress did in 2015-16 was agree to continue to pay the country's bills, we would probably be OK. And we were.

So, a little over 3 months into the Trump Administration, what action has it taken to materially change the economic trajectory?

Basically, nothing. Yes, a bunch of executive orders have been signed promising to undo Obama regulations, and the telecoms have gotten the right to sell all of your data, but in terms of actual action, the economy is still on autopilot.

All of the mid-cycle indicators have made their highs, and a couple of the long leading indicators have vacillated between neutral and negative, and a few more of them are weakening, but are still positive. If the economy stays on autopilot, it probably doesn't have a bad accident until at least the middle of next year -- although I do expect things like job and real wage growth, while still positive, to weaken.

So, the good news is that if Trump and the GOP Congress continue to be unable to form a majority to enact actual policy, we're not in any serious economic danger for now.

The bad news is that something might happen within the next week. If stopgap funding is not passed, at least a partial government shutdown seems likely. Actually welching on our debts is apparently still a few months off.

And Obama's negotiating with the hostage-takers at the time of the 2011 debt ceiling debacle is coming back to bit us in the butt, now that it serves as a precedent. First Trump threatened to cut off funding for Obamacare. The Democrats responded by insisting that its statutory funding be codified in the debt ceiling resolution (something that probably a lot of GOPers silently want to happen as well). Now Trump has threatened to shut down the government and stop paying its bills if he doesn't get all of his legislative wishes, like a border wall and a big tax cut for the wealthy, as part of the deal.

Since the odds of a 2/3's majority in both Houses of Congress overriding any Trump veto are essentially zero, the Full Faith and Credit of the United States is in the hands of an ignorant narcissist. One week from now, the economy might be taken off autopilot and deliberately steered into a mountainside.

For the record, I see no reason for Democrats to go along with any of this. The GOP is in nominal controls of both Houses of Congress, and there is a nominally GOP president. Time to put on their big boy pants and govern. If they won't do that, there is no reasonable rationale for trying to negotiate a less awful, but still awful, outcome.

Saturday, April 22, 2017

Weekly Indicators for April 17 - 21 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

No big change this week from the recent story, although one long leading indicator did flip negative this week, and another edged a little more towards neutral.

Friday, April 21, 2017

No, consumer debt service payments aren't signalling recession

- by New Deal democrat

When I see an article trumpeting an oncoming recession, I will usually take at least a quick look to see if maybe there is an indicator that I've been missing or discounting. Or if it is just the usual cherry-picking of data never relied upon before, and probably not to be relied upon again once it reverses.

So this morning I read that there was a "Gathering Storm of Recession Indicators."

One of the datapoints caught my eye: consumer debt service payments as a percentage of disposable personal income. Here's the graph in context:

I immediately focused on the limited time shown by the graph: the last 8 years, with a nice red line showing how the value now is the value then.

I wondered if maybe I was missing something. After all, this data series comes from the same quarterly report that gives us several other measures of household debt service that I've been following for 10 years, and which have, with one exception, risen into a recession, during and after which they turn down:

Both are pretty much going sideways as of the last report. Nothing exciting happening there.

So here's what happens when I take the reference graph and follow it all the way back to its beginning:

Consumer debt service as a percentage of disposable personal income has been *declining* in advance of 3 of the 4 recessions since the reports were initiated. In the 4th case, the rising debt level was much higher than it is now.

Oh.

Hey, pretty red line though!

Thursday, April 20, 2017

Real wages and spending: I don't think consumers will roll over that easily

- by New Deal democrat

This is the second part of a post about "hard data" and consumer spending.

Yesterday I noted that self-reported consumer spending, as measured by Gallup, has been running 10% or better YoY since the beginning of February, consistent with Amazon.com's earnings growth, but in contrast to a small slump in retail sales as reported for the last two months.

In fairness, real personal consumption expenditures have turned down slightly in the last several months:

Since this measures spending, there is clearly a divergence between this measure and Gallup.

Another contrary argument that the slump in consumer spending is real, is that the cause has been the decline in real wages since last July:

But over the last 50 years, a downturn in real wages has frequently not meant recession. Consumers can cope by refinancing debt at lower rates (not available now), by cashing in appreciating assets, if they have them (e.g., stocks or housing equity), or saving less, before they cut back saving. While there was a slight downturn in the savings rate in 2016, it was less than half of that we saw in 1998 and 2004 (and similar downturns in earlier cycles dnot shown in the below graph):

In the past, consumers have not caved in without saving less first. It could always be different this time, but my suspicion is that we will see a much more substantial decline in the savings rate before we see a real, sustained downturn in spending.

Maybe Jazz Shaw and John Hinderaker Should Read a Report Before Promoting its Result, Part II

Several days ago, both John Hinderaker and Jazz Shaw promoted a story from the Washington Examiner, which in turn covered a new Harvard Business Report study on the effect of San Francisco's $15 minimum wage increase on the restaurant industry. Yesterday, I observed that the report contained a key passage that essentially countered Mr. Shaw's and Mr. Hinderaker's assertion that "basic economics says the increase in the minimum wage is bad." Today, I want to look at the actual results of the report, because a nuanced reading shows that neither Mr. Shaw nor Mr. Hinderaker's points are validated.

Here is the first of two excerpts:

This paper presents several new findings. First, we provide suggestive evidence that higher minimum wage increases overall exit rates among restaurants, where a $1 increase in the minimum wage leads to approximately a 4 to 10 percent increase in the likelihood of exit, although statistical significance falls with the inclusion of time-varying county-level characteristics and city-specific time trends. This is qualitatively consistent but smaller than what Aaronson et al. (forthcoming) find; they show that a 10 percent raise in the minimum wage increases firm exit by approximately 24 percent from a base of 5.7 percent. Differences in sample and specifications may account for the differences between our study and theirs.

Next, we examine heterogeneous impacts of the minimum wage on restaurant exit by restaurant quality. The textbook competitive labor market model assumes identical workers and firms who therefore are equally likely to share in the minimum-wage generated employment and profit losses. However, models that depart from the standard competitive model to allow for heterogeneous workers and firms suggest that a minimum wage increase would cause the lowest productivity firms to exit the market (Albrecht & Axell, 1984; Eckstein & Wolpin, 1990; Flinn, 2006). We show that there is, in fact, considerable and predictable heterogeneity in the effects of the minimum wage, and that the impact on exit is concentrated among lower quality restaurants, which are already closer to the margin of exit. This suggests that the ability of firms to adjust to minimum wage changes could differ depending on firm quality. Finally, we provide evidence that higher minimum wages deter entry, and hastens the time to exit among poorly rated restaurants.

The report's conclusion is hardly breathtaking. According to the report, somewhere between 4 and 10 restaurants per hundred will close as a result of the increase in the minimum wage. And, that number may fall when other variables are added to the mix. In addition, so far only the lower rated restaurants are impacted. And considering the minimum wage is just going into effect, it's possible the techniques used by higher rated restaurants to limit the impact will be passed down to the lower rate restaurants -- which is a standard development in the market economy.

In fact, the findings are consistent with the literature. As this report conceded: even studies that identify negative impacts find fairly modest effects overall, suggesting that firms adjust to higher labor costs in other ways. Most economists would call a 4-10% closure rate (which has the potential to be lower when other factors are considered) of marginally efficient restaurants modest.

And a final point: the authors make no mention of San Francisco's restaurant bubble. That means that we could simply be seeing correlation, no causation.

What can we conclude from this little exercise:

First: Jazz Shaw doesn't read for comprehension.

Second: Jazz Shaw shouldn't be allowed to write about economics.

Third: Jazz Shaw will continue to do so, largely because he thinks he's an expert.

And so, we will continue to point out just how wrong he is.

Here is the first of two excerpts:

This paper presents several new findings. First, we provide suggestive evidence that higher minimum wage increases overall exit rates among restaurants, where a $1 increase in the minimum wage leads to approximately a 4 to 10 percent increase in the likelihood of exit, although statistical significance falls with the inclusion of time-varying county-level characteristics and city-specific time trends. This is qualitatively consistent but smaller than what Aaronson et al. (forthcoming) find; they show that a 10 percent raise in the minimum wage increases firm exit by approximately 24 percent from a base of 5.7 percent. Differences in sample and specifications may account for the differences between our study and theirs.

Next, we examine heterogeneous impacts of the minimum wage on restaurant exit by restaurant quality. The textbook competitive labor market model assumes identical workers and firms who therefore are equally likely to share in the minimum-wage generated employment and profit losses. However, models that depart from the standard competitive model to allow for heterogeneous workers and firms suggest that a minimum wage increase would cause the lowest productivity firms to exit the market (Albrecht & Axell, 1984; Eckstein & Wolpin, 1990; Flinn, 2006). We show that there is, in fact, considerable and predictable heterogeneity in the effects of the minimum wage, and that the impact on exit is concentrated among lower quality restaurants, which are already closer to the margin of exit. This suggests that the ability of firms to adjust to minimum wage changes could differ depending on firm quality. Finally, we provide evidence that higher minimum wages deter entry, and hastens the time to exit among poorly rated restaurants.

The report's conclusion is hardly breathtaking. According to the report, somewhere between 4 and 10 restaurants per hundred will close as a result of the increase in the minimum wage. And, that number may fall when other variables are added to the mix. In addition, so far only the lower rated restaurants are impacted. And considering the minimum wage is just going into effect, it's possible the techniques used by higher rated restaurants to limit the impact will be passed down to the lower rate restaurants -- which is a standard development in the market economy.

In fact, the findings are consistent with the literature. As this report conceded: even studies that identify negative impacts find fairly modest effects overall, suggesting that firms adjust to higher labor costs in other ways. Most economists would call a 4-10% closure rate (which has the potential to be lower when other factors are considered) of marginally efficient restaurants modest.

And a final point: the authors make no mention of San Francisco's restaurant bubble. That means that we could simply be seeing correlation, no causation.

What can we conclude from this little exercise:

First: Jazz Shaw doesn't read for comprehension.

Second: Jazz Shaw shouldn't be allowed to write about economics.

Third: Jazz Shaw will continue to do so, largely because he thinks he's an expert.

And so, we will continue to point out just how wrong he is.

Wednesday, April 19, 2017

The Amazon.com effect: retailers say they're not selling, but consumers report they are buying

- by New Deal democrat

This was originally one post but I think it works better divided into two parts.

One of the issues I keep reading about recently is the (alleged) divergence between "soft" and "hard" data. For example, consumer sentiment as measured by the University of Michigan (and the Conference Board, and Gallup) has been making new highs since the Presidential election last November (according to Gallup, mainly fueled by a massive gain in optimism among Republicans). while "hard data," chiefly industrial production but also including consumer spending, has failed to follow suit.

One problem with this thesis has been that manufacturing as measured by the industrial production index, turned up for five months in a row. It turned down in March, and one good measure of how intellectually honest the commentator is, is whether they have been using a consistent measure for industrial production:

One problem with this thesis has been that manufacturing as measured by the industrial production index, turned up for five months in a row. It turned down in March, and one good measure of how intellectually honest the commentator is, is whether they have been using a consistent measure for industrial production:

Production as a whole only fell in January and February because of utility production (warm winter in the eastern half of the US). In March, production only rose because utility production rebounded sharply (March was actually colder than February in much of the East).

So a Doomer who was all over the decline in industrial production for the last two months should be touting its advance in March. If the Doomer backs out utilities this month, take a look to see if they did the same thing last month -- almost certainly not.

Another problem with the soft/nard data dichotomy is that online retail appears to have reached a tipping point where it is causing big damage to brick-and-mortar retailers, who are laying off thousands of employees and even shutting down completely.

So a Doomer who was all over the decline in industrial production for the last two months should be touting its advance in March. If the Doomer backs out utilities this month, take a look to see if they did the same thing last month -- almost certainly not.

Another problem with the soft/nard data dichotomy is that online retail appears to have reached a tipping point where it is causing big damage to brick-and-mortar retailers, who are laying off thousands of employees and even shutting down completely.

I am concerned that the official real retail sales numbers might not be adequately picking up online retail:

But here is Amazon.com's sales numbers for 2016 vs. 2015:

And here is the number that really jumps out -- Gallup's consumer spending, here measured for the last two years:

Pay attention to that $100 line. Except for Christmas seaon 2015, that line wasn't breached at all in the 14 day average until December 2016. And spending has remained above that $100 line all during February, March, and April so far. Most often for the last 10 weeks, this measure has been up over 10% YoY. Now, before you criticize Gallup's measure, it earned its bones in 2011 at the time of the Debt Ceiling Debacle, when it was the only measure that accurately reported that consumers hadn't stopped spending.

So if retailers are reporting poor sales, but consumers are telling people that they are spending 10% this year vs. last year, then we have to wonder if the official measures aren't catching the full extent of the big secular increase in online sales.

But here is Amazon.com's sales numbers for 2016 vs. 2015:

And here is the number that really jumps out -- Gallup's consumer spending, here measured for the last two years:

Pay attention to that $100 line. Except for Christmas seaon 2015, that line wasn't breached at all in the 14 day average until December 2016. And spending has remained above that $100 line all during February, March, and April so far. Most often for the last 10 weeks, this measure has been up over 10% YoY. Now, before you criticize Gallup's measure, it earned its bones in 2011 at the time of the Debt Ceiling Debacle, when it was the only measure that accurately reported that consumers hadn't stopped spending.

So if retailers are reporting poor sales, but consumers are telling people that they are spending 10% this year vs. last year, then we have to wonder if the official measures aren't catching the full extent of the big secular increase in online sales.

Maybe Jazz Shaw and John Hinderaker Should Read Papers Before Promoting Their Results

Yesterday, the conservative blogsphere was on fire with a new report from the Harvard Business School that supposedly proved raising the minimum wage is forever damaging to the local restaurant industry. Rather than reading the actual report themselves, both Mr. Shaw and Mr. Hinderaker relied on the Washington Examiner as their media filter. This was a big mistake. In the words of the Princess Bride, "I don't think that report says what you think it says..

First, let's start with the following stunning rebuke of Mr. Shaw and Mr. Hinderaker, both of whom argue that simple economics shows raising the minimum wage is damaging:

Mr. Shaw:

There is an entire body of work in the progressive sphere dedicated to nothing but this particular propaganda effort. The premise makes no sense in terms of basic economics (or simply math, for that matter) but it keeps on being repeated. And yet, when the experiment is moved off of the chalkboard and out into the real world the opposite always seems to happen.

Mr, Hinderaker:

A number of cities across the country have enacted dramatic increases in the minimum wage. This has caused a great deal of harm, but on the plus side, it has enabled research on the economic consequences of mandating wages at higher than market rates.

However, the new report directly contradicts both statements. From page 6 of 33 of the report:

Our results contribute to the existing literature in several ways. First, our findings relate to a large literature seeking to estimate the impact of the minimum wage, most of which has focused on identifying employment effects. While some studies find no detrimental effects on employment (Card and Krueger 1994, 1998; Dube, Lester & Reich, 2010), others show that higher minimum wage reduces employment, especially among low-skilled workers (see Neumark & Wascher, 2007 for a review). However, even studies that identify negative impacts find fairly modest effects overall, suggesting that firms adjust to higher labor costs in other ways. For example, several studies have documented price increases as a response to the minimum wage hikes (Aaronson, 2001; Aaronson, French, & MacDonald, 2008; Allegretto & Reich, 2016). Horton (2017) find that firms reduce employment at the intensive margin rather than on the extensive margin, choosing to cut employees hours rather than counts. Draca et al. (2011) document lower profitability among firms for which the minimum wage may be more binding

The emboldened sentences are very clear. First, there is a large amount of academic support for arguing that raising the minimum wage to certain levels has no negative effect. But here's the kicker: the reports that supposedly support Mr. Shaw and Mr. Hinderaker don't provide the support they thought. The negative effects are "modest, suggesting that firms adjust in other ways." This is a point I made last spring,

Shaw's and Perry's reasoning run into two primary microeconomic problems. Both assume labor demand is elastic (a term I doubt Mr. Shaw is familiar with) -- that a change in cost will have a disproportionate impact on demand. However, this simply isn't true. For example, let's assume that a restaurant owner currently has 10 employees when wages increase. Let's assume he fires 4 people due to increase cost. At some point, he'll cut off his economic nose to spite his face -- that is, he'll lower his payroll to such an extent that he'll hurt customer service, lowering overall revenue. Given the profit maximizing principal underlying cost theory (again, I doubt Mr. Shaw is aware of this concept, either), the current level of 10 employees is probably already peak efficiency, which means he'll either, absorb the cost, cuts costs elsewhere, raise prices, or do some combination of all three.

And then there's the inherent problem of the production function graph:

As anyone who knows micro (which, it is painfully obvious Mr. Shaw doesn't) would note, when you lower your primary short-term variable cost (labor) you also lower your output. Now, it's possible you might not do too much damage, depending on a number of different factors, but the bottom line is that you're moving in the wrong direction.

In my next post, I'll look at the results. Because, like the above points, they don't support Mr. Shaw or Mr. Hinderaker nearly as much as either thinks.

Tuesday, April 18, 2017

Jazz Shaw Still Can't Make the Minimum Wage Argument Stick

Jazz Shaw desperately wants to make sure that his readers believe raising the minimum wage is a bad idea that will lead to job losses. Hot off the presses, he cites a new Harvard Business Review article that he things validates his position.

San Francisco’s higher minimum wage is causing an increasing number of restaurants to go out of business even before it is fully phased in, a new study by the Harvard Business School found.

The closings were concentrated among struggling, lower-rated restaurants. The higher minimum also caused fewer new restaurants to open, it found.

“We provide suggestive evidence that higher minimum wage increases overall exit rates among restaurants, where a $1 increase in the minimum wage leads to approximately a 4 to 10 percent increase in the likelihood of exit,” report Dara Lee and Michael Luca, authors of “Survival of the Fittest: The Impact of the Minimum Wage on Firm Exit.” The study used as a case study San Francisco, which has an estimated 6,000 restaurants in the Bay Area and is ratcheting up its minimum wage. Restaurants are one of the largest employers of minimum wage workers.

Except, it's not the minimum wage causing this. Instead, San Francisco's restaurant bubble is bursting. According to 2010 Census data:

Not only did San Francisco come in as number one with the most restaurants per capita, no other city even came close. At 39.3 restaurants per 10,000 households, San Francisco has nearly 50 percent more relative restaurants than the second place city.

That's an amazing large number of restaurants per capita -- a pace of growth the city maintained throughout the tech boom:

San Francisco's restaurant scene is outpacing New York — at least in terms of growth. That's according to a new study by conducted by international payment processing company First Data, which compares New York and San Francisco's restaurant scenes and delivers some intriguing insights about dining trends in both cities.

Here's the crux of the matter:

To do that I'm going to tell the story of the rise and fall of Matt Semmelhack and Mark Liberman's AQ restaurant in San Francisco. But this story isn't confined to SF. In Atlanta, D.B.A. Barbecue chef Matt Coggin told Thrillist about out-of-control personnel costs: "Too many restaurants have opened in the last two years," he said. "There are not enough skilled hospitality workers to fill all of these restaurants. This has increased the cost for quality labor." In New Orleans, I spoke with chef James Cullen (previously of Treo and Press Street Station) who talked at length about the glut of copycats: "If one guy opens a cool barbecue place and that's successful, the next year we see five or six new cool barbecue places... We see it all the time here."

Here's econ 101 for Mr. Shaw: San Franciso's large number of restaurants created a labor shortage. That means there were too few workers. It's called supply and demand. Combine that with sky high real estate prices and it's no wonder we have this problem. Mr. Shaw is making a classic rookie mistake: correlation does not equal causation.

So, once again, we have an analytical failure by Mr. Shaw. Does he care? Not at all. Retractions and corrections are for the liberal press, not conservative bloggers.

San Francisco’s higher minimum wage is causing an increasing number of restaurants to go out of business even before it is fully phased in, a new study by the Harvard Business School found.

The closings were concentrated among struggling, lower-rated restaurants. The higher minimum also caused fewer new restaurants to open, it found.

“We provide suggestive evidence that higher minimum wage increases overall exit rates among restaurants, where a $1 increase in the minimum wage leads to approximately a 4 to 10 percent increase in the likelihood of exit,” report Dara Lee and Michael Luca, authors of “Survival of the Fittest: The Impact of the Minimum Wage on Firm Exit.” The study used as a case study San Francisco, which has an estimated 6,000 restaurants in the Bay Area and is ratcheting up its minimum wage. Restaurants are one of the largest employers of minimum wage workers.

Except, it's not the minimum wage causing this. Instead, San Francisco's restaurant bubble is bursting. According to 2010 Census data:

Not only did San Francisco come in as number one with the most restaurants per capita, no other city even came close. At 39.3 restaurants per 10,000 households, San Francisco has nearly 50 percent more relative restaurants than the second place city.

That's an amazing large number of restaurants per capita -- a pace of growth the city maintained throughout the tech boom:

San Francisco's restaurant scene is outpacing New York — at least in terms of growth. That's according to a new study by conducted by international payment processing company First Data, which compares New York and San Francisco's restaurant scenes and delivers some intriguing insights about dining trends in both cities.

Here's the crux of the matter:

To do that I'm going to tell the story of the rise and fall of Matt Semmelhack and Mark Liberman's AQ restaurant in San Francisco. But this story isn't confined to SF. In Atlanta, D.B.A. Barbecue chef Matt Coggin told Thrillist about out-of-control personnel costs: "Too many restaurants have opened in the last two years," he said. "There are not enough skilled hospitality workers to fill all of these restaurants. This has increased the cost for quality labor." In New Orleans, I spoke with chef James Cullen (previously of Treo and Press Street Station) who talked at length about the glut of copycats: "If one guy opens a cool barbecue place and that's successful, the next year we see five or six new cool barbecue places... We see it all the time here."

Here's econ 101 for Mr. Shaw: San Franciso's large number of restaurants created a labor shortage. That means there were too few workers. It's called supply and demand. Combine that with sky high real estate prices and it's no wonder we have this problem. Mr. Shaw is making a classic rookie mistake: correlation does not equal causation.

So, once again, we have an analytical failure by Mr. Shaw. Does he care? Not at all. Retractions and corrections are for the liberal press, not conservative bloggers.

Subscribe to:

Posts (Atom)