- by New Deal democrat

- by New Deal democratThe big housing debate is whether prices are on the cusp of bottoming (or possibly, already have) vs. whether there is a considerable ways still to go before housing prices bottom.

Two of the most popular bloggers, Bill McBride a/k/a Calculated Risk, and Barry Ritholtz, are on opposite sides.

Back on February 6, CR said:

There are several reasons I think that house prices are close to a bottom. First prices are close to normal looking at the price-to-rent ratio and real prices (especially if prices fall another 4% to 5% NSA between the November Case-Shiller report and the March report). Second the large decline in listed inventory means less downward pressure on house prices, and third, I think that several policy initiatives will lessen the pressure from distressed sales (the probable mortgage settlement, the HARP refinance program, and more).Barry Ritholtz responded with a 5 part series, in which he concluded:

....[T]his doesn't mean prices will increase significantly any time soon. Usually towards the end of a housing bust, nominal prices mostly move sideways for a few years, and real prices (adjusted for inflation) could even decline for another 2 or 3 years.

homes will continue stumbling along the bottom of the price range, with a negative bias to prices. Another 5-10% is a very easy downside target — assuming nothing else goes wrong.CR's style is inductive: he looks at past patterns, such as months of housing supply on the market, notices that the same patterns are in evidence now, and concludes we are near a bottom. By contrast, Ritholtz's piece is more deductive. Certain factors, since as a large number of foreclosures, are hanging over the market. It is logical that these will cause prices to fall further, therefore they will.

It will hardly surprise anybody who has been reading my housing posts for the last year that I believe housing is close to making a "nominal" bottom (i.e., without adjusting for inflation). My arguments and conclusions are close to CR's.

Nevertheless, Barry Ritholtz has written a comprehensive and intelligent defense of his position. Since I respectfully disagree, it is fair that I point out why his arguments ultimately fail to convince me.

Ritholtz's arguments can be distilled into three: (1) housing is not actually affordable by traditional measures. Down payments remain unrealistically high, and buyers cannot qualify for mortgages; (2) there is a large overhang of "shadow inventory" most especially including but not limited to foreclosures, which are primed to put renewed downward pressure on prices; and (3) potential buyers, especially younger buyers, are fearful of the potential immobility that comes with owning a house vs. renting.

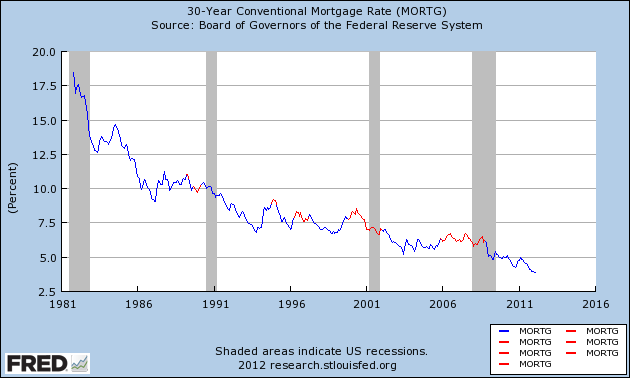

My rebuttal, in order, is in summary that: as to point (1) Barry's argument regarding traditional housing affordability fails to account for the role of mortgage rates. Once we take those into account, housing is already fairly priced. Beyond that, his argument about what potential homeowners can afford contains a vital mathematical error. As to point (2) the rate at which foreclosures and other shadow inventory come on the market makes a world of difference as to whether they affect the first derivative of prices (i.e., the direction), or only the second derivative (e.g, rather the rate of increase is faster or slower). At times Barry's own stated argument is as to the second derivative rather than the first. Finally, as to point (3) demographics are destiny. Not only is there "pent-up demand" of young buyers who so far have been unable to buy a home, but there is an ongoing increase in the number of young adults at the age when the purchase of a first home takes place. This is an increase in demand that will overwhelm the contrary factors.

One final point: much like the argument as to the overall economy, much of the vehemence is semantic. CR says that the housing recovery has begun. Ritholtz says his intent is debunking the housing recovery story. Despite this, CR and Ritholtz are really not far apart. Like me, CR believes prices are making a "nominal" bottom and in real terms they will continue to decline. Ritholtz sees at minimum another 5% to 10% decline, with prices "stumbling along the bottom of the price range." Those two conclusions aren't necessarily inconsistent, depending on whether part of Ritholtz's decline includes nominal prices.

Next: Housing affordability