Tula Connell is with the AFL-CIO. I have asked her to contribute to this blog to help enlarge the conversation about unions, international trade and, well, anything else that pops into her fertile mind. - BonddadTreasury Secretary Henry Paulson needs a new appointment scheduler.

Someone on his staff failed to notice that as the former Goldman Sachs honcho heads to China this week, the U.S. Trade Representative was slated to released the 2006

Report to Congress on China's WTO Compliance. The report, issued today, is highly critical of the Chinese government's failure to meet their obligations. It places a “particular emphasis on reducing IPR [intellectual property rights] infringement levels in China” and on pressing China to make greater efforts to institutionalize market mechanisms and make its trade regime more predictable and transparent.

The timing couldn’t be worse for Paulson.

When Bush and the Republican Congress rammed through China’s membership in 2001, they assured us that making China a full partner would ease the path for that nation to lower its trade barriers and bring its laws and regulations into compliance with international standards. In fact, the opposite occurred: Since China joined the World Trade Organization (WTO) in 2001, the U.S. deficit has grown to more than $200 billion. In 2005, the trade deficit with China grew by 25 percent to

$202 billion—the largest bilateral deficit in world history.

Behind this unsustainable trade deficit are two major factors: China’s policy to devalue its currency and its abysmal workers’ rights record. In fact, the Treasury Department once again is delaying the release of its semi-annual report on currency—so as not to embarrass Paulson while in China. Although the undervaluation of China's currency has become accepted fact, every Treasury report to date has failed to suggest taking any action.

While Paulson will chat with China’s leaders about the China’s currency devaluation, he has no intention of bringing up workers’ rights.

He should—if not because ethical principles call for providing fellow humans with decent working conditions and living wages, then for our own self-interest as a nation. Because addressing China’s human rights violations is one important step toward reversing the declining U.S. trade balance with China.

The deterioration of working conditions in China

continues every year, with nearly non-existent enforcement of wage, overtime, safety and health and environmental laws. Oppressing Chinese workers is the functional equivalent of devaluing currency. In failing to address the systematic abuse of its workers, the Chinese government further displaces U.S. jobs.

American companies like Wal-Mart rack up billions of dollars in profits by taking advantage of the artificially low wages made possible by the Chinese government’s repression of democracy, political dissent and fundamental human and workers’ rights.

Application of an International Trade Commission model shows that up to 973,000 manufacturing jobs and 1,235,000 total jobs are displaced by China's repression of labor rights. The nonprofit Economic Policy Institute (EPI) estimates 410,000 manufacturing jobs were lost to China between

2002 and 2004. U.S.-China Economic and Security Review Commission studies conclude that between 70,000 and 100,000 jobs are moved annually to China, and those numbers accelerated after 2001.

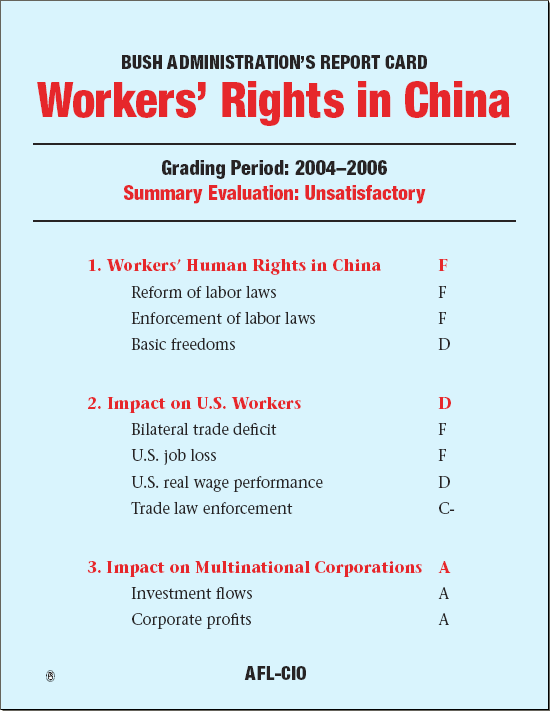

The 2006 annual report of the U.S.-China Economic and Security Review Commission (a bipartisan, congressionally appointed commission) also provides evidence that China has been seriously inconsistent in meeting its obligations as a member of the WTO. The report backs up conclusions in the AFL-CIO’s Bush administration report card on China and an AFL-CIO Solidarity Center study on workers’ rights in China.

In July, the AFL-CIO filed the second workers’ rights case

against the Chinese government. The Bush administration rejected the petition, despite the lack of improvement for Chinese workers since we filed the first petition in 2004. As we filed the petition this year, workers from across the nation sent nearly

70,000 letters to President Bush and Congress urging them to take action to halt the abuse of China’s workers.

For instance:

- Chinese mines are the most dangerous in the world, with more than 10,000 Chinese miners dying in industrial accidents each year (some 80 percent of the worldwide total).

- Rates of illness and injury have never been higher in China’s manufacturing sector as officials of China’s own Work Safety Administration conceded as recently as February 2006.

- There are as many as 10 to 20 million child workers in China—from one-eighth to one-quarter the number of factory workers.

- China’s minimum working age standard is widely violated, and the Chinese government does little to enforce the standard. As the U.S. State Department stated in its 2005 Human Rights Report on China, “The government continued to maintain that the country did not have a widespread child labor problem.”

- The Chinese government implements an extensive system of forced labor camps. The precise number of forced prison laborers is unknown, but estimates range from 1.75 million to 6 million and higher.

The

right to strike was removed from China's Constitution in 1982 because the political system had "eradicated problems between the proletariat and enterprise owners." But as aggregate unpaid wages have risen to record levels, along with increased child labor, Chinese workers are walking off the job in massive numbers, despite the illegality of their actions and the risks involved.

According to figures from China’s Ministry of Public Security, there was a sharp rise in officially registered public disturbances in 2005. Large-scale incidents of "mass gatherings to disturb social order" rose by 13 percent. In one report, "mass protests" or "mass incidents," including riots, demonstrations and collective petitions, rose from 58,000 in 2003 to 87,000 in 2004.

These abuses allow producers in China, including many multinational and U.S. corporations, to operate in an environment free of independent unions, to pay illegally low wages and to profit from the widespread violation of workers’ basic human rights.

The second factor behind China’s trade advantage, the nation’s deliberate undervaluing of its currency, the yuan, enables the Chinese government to export products at an artificially low price—running up the U.S. trade deficit and costing good American jobs. In fact, the yuan is estimated to be undervalued by as much as 40 percent.

An AFL-CIO report shows China’s fixed currency rate artificially lowers the price of its goods by 40 percent and subsidizes exports, putting U.S. companies and workers at a disadvantage. The lack of currency flexibility has been a major factor in U.S. job losses and a trade deficit with China that hit $202 billion last year.

In a letter to the Wall Street Journal earlier this year, AFL-CIO Secretary-Treasurer Richard Trumka said the Chinese government’s deliberate undervaluing of its currency is an anchor “that is dragging down American manufacturing and the middle class:”

Currency manipulation is one of the primary reasons for the massive bilateral trade imbalance between the United States and China, as well as for the flood of investments by U.S and other multinational companies. On top of the Chinese government’s record capital investments in manufacturing, foreign direct investment (FDI) in the country increased from $46.8 billion in 2000 to $60.3 billion in 2005. Seventy percent of China’s FDI is in manufacturing, with heavy concentration in export-oriented companies and advanced technology sectors. The dangers of this model of development are apparent: job and technical capacity loss in the U.S., growing inequality and political and financial instability in China, and the accumulation of nearly $1 trillion in U.S. dollar assets by the Chinese government. This is also a development model based upon the brutal repression of workers’ rights and human rights.

Last year, the Senate introduced legislation sponsored by Sens. Charles Schumer (D-N.Y.) and Lindsey Graham (R-S.C.) that would have imposed a 27.5 percent tariff on all Chinese imports if that country did not raise the value of its currency within 12 months. The bill was never introduced in the House, and Senate leaders chose not to bring it up in the last session.

Paulson fears the next Congress will pass a tariff, and this is his last-gasp trip to convince China to voluntarily devalue its currency.

But unlike the 109th, the new Congress not only is more likely to take a firmer line on China’s currency devaluation, it will insist that the administration include workers’ rights as a key part of trade agreements and bilateral negotiations.

And the AFL-CIO will be working with Congress to ensure that going forward, trade deals aren’t just free but fair.