- by New Deal democrat

Our last piece of important housing information for the month was released this morning; namely repeat home sale prices as measured by the FHFA and Case Shiller. The former increased by 0.6%, and the latter by 0.3%, continuing their increases since the beginning of this year:

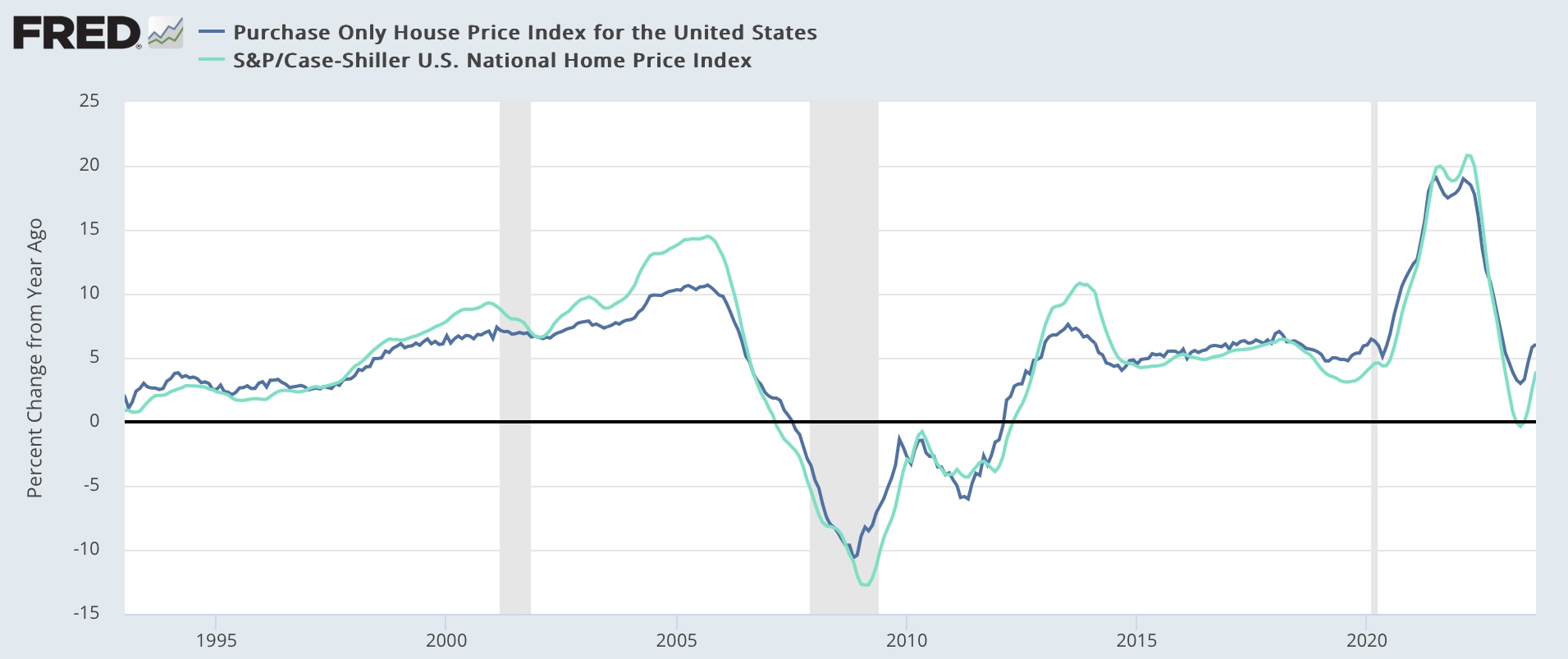

On a YoY basis, the FHFA Index is up 6.1%, while the Case Shiller Index is up 3.9%:

As repeat sales, by definition these are existing home sales, and the increases in these indexes are similar (on a non-seasonally adjusted basis) to the last year’s record in the NAR data:

The story continues to be that many existing homeowners are frozen in place by 3% mortgages. They are not selling and saddling themselves with new 7% or 8% mortgages. So inventory is way down, and buyers, especially entry level buyers, have to compete for that small inventory. This is completely different from the new home market, where homebuilders are using mortgage rebates and other incentives, such as smaller home sizes, to lower the cost to buyers, and so sales have not suffered nearly as much.

Finally, because sales prices lead the CPI measure for shelter via fictitious Owners’ Equivalent Rent, here is the YoY comparison of each:

The upturn in repeat sales prices will probably have some softening effect on the downward slope of OER in the months ahead, but the expected downward slope remains very much intact.