- by New Deal democrat

This is an update of a post I wrote almost exactly 10 years ago. I’m doing this because of an important secular change I noticed that appears to have happened in the financial markets.

So, dear reader, perhaps you are wondering what has happened in the 10 years since then.

Back when I first started delving into financial markets and economy 30 years ago, I noticed that, dating all the way back to the Great Depression, the stock market appeared to perform best during periods of very low inflation, or very slight deflation, that persisted. The more inflation beyond about 3%, the worse the market performed. And in the rate case where deflation was more than -1%, the stock market performed horribly (because deflation of greater than -1% almost always includes wage deflation).

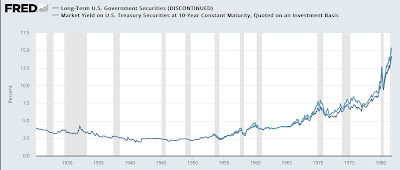

It has generally also been true that bond yields move in very long, e.g., 60 year or so cycles of declining vs. increasing interest rates.

For example, here are long bond rates between the early 1920s and 1980:

And here they are between 1981 and the present:

Based on those two insights, it appeared that bond yields and stock prices behaved differently vs. one another during times of longer term declines in the inflation rate (disinflation), times of very low inflation rates or even deflation (deflation), or longer term increasing interest rates (reflation).

So, 10 years ago I wrote the following:

“it is important to keep in mind the difference between inflationary recessions and deflationary recessions. All of the post-WW2 recession through 2000 were inflationary recessions. Inflation increased, the Fed raised short rates to counter it, long rates began to decline as bond investors anticipated weakness, and a recession began. In deflationary recessions, an asset bubble bursts, and/or a debt overhang reaches critical mass, and the inflation rate declines, possibly turning into deflation. Interest rates follow, subject ot the zero lower bound.

“The difference in the two types of scenarios is manifest in the different way that interest rates have behaved vis-a-vis stock prices during the disinflationary period of 1982-97 vs. 1998 to the present.”

“The difference in the two types of scenarios is manifest in the different way that interest rates have behaved vis-a-vis stock prices during the disinflationary period of 1982-97 vs. 1998 to the present.”

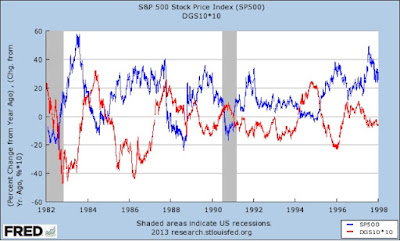

At that point in the post I included two graphs (in the old FRED format you may remember). First, the YoY% change in stock prices vs. Treasury yields from 1982-98:

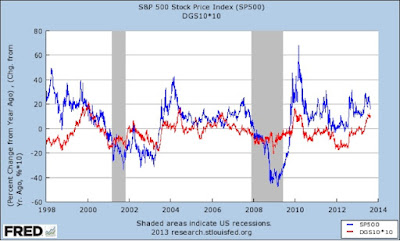

And then the period from 1998 to 2013:

I continued:

“During the disinflationary period of 1982-97, the YoY percentage change in stock prices was the mirror image of the YoY percentage change in bond yields. Stocks rose when bond yields fell, and stocks fell when bond prices rose. From 1998 on, however, almost always stock prices and bond yields have moved in the same direction (with the exception of late 2003 through mid-2006).

“During that period, bond yields fell even with a strong economy.

“But that changed beginning in 1998. From that point until the present, bond yields have generally risen with a strengthening economy, and fallen with a weaker economy. As first the tech stock bubble burst, and then the housing bubble burst, there were deflationary moves in asset prices and declining bond yields simultaneously. Several times since then, there have been brief periods of outright deflation. Perhaps a more finely grained assessment is that, since 1998, during periods of a strong economy, bond yields and stock prices behaved as mirror images. But during periods of a weak economy (which has been the vast majority of the time since the turn of the Millenium), the two asset classes have moved in tandem.”

“But that changed beginning in 1998. From that point until the present, bond yields have generally risen with a strengthening economy, and fallen with a weaker economy. As first the tech stock bubble burst, and then the housing bubble burst, there were deflationary moves in asset prices and declining bond yields simultaneously. Several times since then, there have been brief periods of outright deflation. Perhaps a more finely grained assessment is that, since 1998, during periods of a strong economy, bond yields and stock prices behaved as mirror images. But during periods of a weak economy (which has been the vast majority of the time since the turn of the Millenium), the two asset classes have moved in tandem.”

Fear not. Here is the same graph (averaging stock prices monthly), starting in 2014 through early 2021:

And here it is from 2021 to the present:

You can see that bond yields and YoY inflation continued to move in broad similarity up until early 2021, just as they had since 1998.

Then the situation changed. Since early 2021, they have moved in opposite directions. It could of course just be a brief divergence, but I suspect this is a longer term secular change, marking a reflationary era in which over time the trend in bond yields will continue to be higher, just as it was between the early 1950s to 1980. Stock prices will react negatively to each such racheting higher.