When looking at a large, established company's earnings and cash flow statements, the main thing I want is predictability and consistency. While I don't expect the numbers to be completely uniform, lots of jumping around indicates the underlying economy is weak or that management may be having problems. With that in mind, let's start by looking at Ebay's Margins:

Over the last 5 years, the gross margin has declined from 71.58% in 2009 to 68.62% in 2013 -- a drop of about 4%. This isn't fatal; it does indicate the COGS has increased slightly over the last 5 years. At the same time, the operating margin has increased from 16.69% to 21.01%. The primary reason for this increase is SGA expenses as a percent of gross revenue have decreased from 37.86% in 2009 to 29.68% in 2013. The net margin has decreased from 27.37% in 2009 to 17.8% in 2013. But this drop is a bit of a misnomer; in 2009, the company recorded $1.4 billion in "other" income, in addition to income from continuing operations. In other words, a net margin in the high teens (17%-19%) is far more customary.

The decrease in the SGA expenses is encouraging, as it indicates costs are clearly under control. That's always a good sign. And the overall consistency in the revenue statement's margins also tells us management has a steady and disciplined hand.

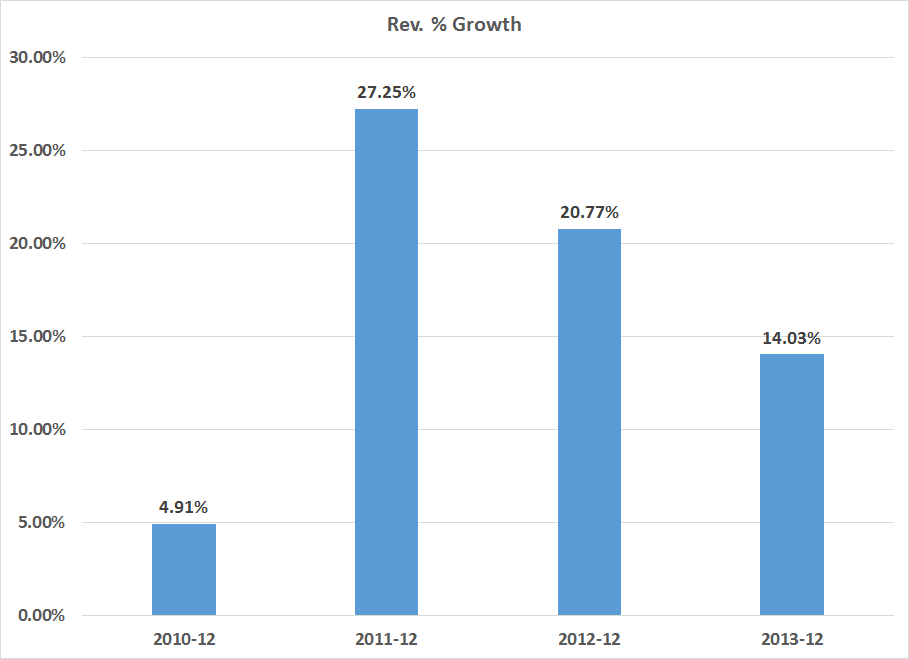

Next, let's take a look at the company's overall revenue growth:

Coming out of the recession, growth was slow at a bit under 5%. 2011 and 2012 had some strong growth (perhaps pent-up demand kicking in) while 2013's figure was a bit more subdued. However, for a maturing company like Ebay, 14% is certainly nothing to sneeze at. Given Ebay is a mature company, top line revenue growth in the 14%-20% is far more likely.

Let's turn to the cash flow statement, starting with the relationship between operating earnings and investment activities. A mature company like Ebay should be able to derive investment funds from its operations, thereby freeing it on the financing side.

Here's a chart of the difference between operating cash flows and investment expenditures:

Ebay received a big cash infusing in 2009. In that year, they had $2.9 billion in operating income but only $1.1 billion in investments. Then they only had $567 million in PPE investments which was 19% of operating revenues. It's also highly probably management invested minimally as the economy was just emerging form the recession and growth was low. In 2010, there is still a net increase in cash, again with the most likely reason being conservatism on the part of management; their biggest investment expense was still PPE, but that total was only 26% of operating expenses. In 2011 and 2012, Ebay ramped up PPE investments, which totaled $963.5 million and $1.257 billion, respectively. The growth in their overall PPE expenditures is expressed in this chart:

In addition to strong increases in PPE, Ebay has been adding to their overall investment portfolio at a strong pace on an annual basis:

These investments have gone both to cash (in the form of short-term securities) and overall investments.

Finally, let's turn to the financing section of the cash flow statement. It shows two points.

1.) Over the last five years, Ebay has issued $4.4 billion in debt and repaid $1.5 billion, for a net change in debt outstanding of $2.8 billion.

2.) Ebay has repurchased a little over $4 billion in stock. Overall treasury stock has increased from $5.3 to $9.3 billion.

This leads to an interesting question: if and when Ebay will pay a dividend. Consider EBay's retained earnings:

Total retained earnings have increased from $8.3 billion in 2009 to $18 billion in 2013. The board is obviously paying shareholders now in the form of share buybacks. But, given that high level of retained earnings and EBay's ability to generate cash, a dividend might be in the future.

So, to conclude, EBay's management has costs under control as evidenced in the income statement. Margins have been constant and growth has been steady. I would expect a drop in annual growth rates to the high teens in the future. The cash flow statement indicates the company has the ability generate a large percentage of its investment needs through ongoing sales, freeing the company up when it comes to structuring their financing.

Simply put, EBay's a solid company.