- by New Deal democrat

You may have heard on your car radio or on television last night after you came home from work that the stock market had a bad day, dropping about 2.5%. Probably the newscaster said something about it being a reaction to the Federal Reserve Bank's announcement that it expects to "taper" its purchases of long term bonds in the near future. While the daily gyrtions of the stock market are not worth getting excited about, IF the "taper" happens, it likely will affect you. Let me explain why.

First of all, let's put the stock market decline of the last two days in perspective. Here's a daily graph of the S&P 500 since the beginning of this year:

Note that the market rose almost 20% since January 1. Even with the 5% selloff over the last 2 days since Bernanke confirmed that the Fed intends to start "tapering" soon, it is still up over 10% for the year.

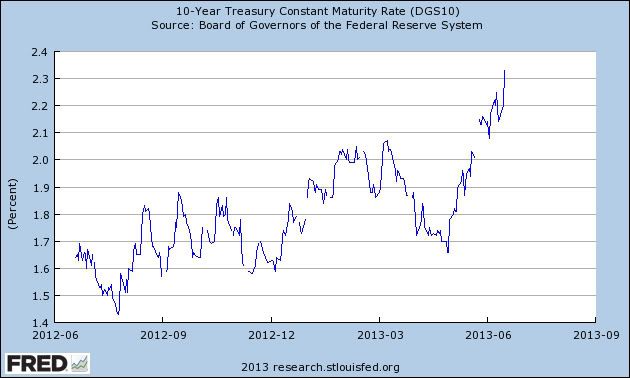

While I don't presume to read traders' (or trading computers') minds (see Barry ritholtz' note this morning about ex post facto rationalizations), generally speaking there is concern that the "taper" of long term bond purchases will cause bond yields (the percent of interest paid on them) to rise. When bond yields rise, the market price to purchase or sell those bonds falls. When most traders expect prices to fall in the future, what do they do? They sell the assets now, causing prices to fall immediately, rather than in the future! That's exactly what has happened over the last month, as shown in this graph of the yield on the 10 year US treasury bond for the last year (keep in mind that yields going up means prices going down):

This is a sharp move, although as we'll see in the next graph, from a longer-term perspective, it is little more than a blip. That being said, there's a pretty good chance that last summer's low in long term interest rates may be the lowest you will ever have seen in your whole life.

The reason average Americans should care about the "taper" is that higher interest rates on bonds also means higher interest rates on things like mortgages. One of my constant points on this blog for the last several years has been that households' refinancing of their mortgage debt at lower and lower rates has put more money in their pockets for spending and for paying down debt. This next graph is an update of one from Mortgage News Daily that I've run a number of times over the last couple of years, comparing the amount of mortgage refinancing (yellow) with mortgage interest rates (blue):

The graph starts in 2008 at the depths of the recession. Note that refinancing was at its low ebb. Since then and especially in late 2011 and 2012, with record low mortgage rates refinancing has boomed. At the far right of the graph you can see the last month's spike in mortgage rates, and the steep decline in refinancing back to mid-2011 levels.

Simply put, the more the "taper" causes interest rates to rise, the less refinancing of mortgages we will see. We'll probably also see a decline in the amount of purchases of new homes as well, since purchasers will also be faced with hgher mortgage rates.

And mortgage refinancing has been one of the most important reasons why the economy has continued to move forward in the last few years, despite the stagnation in real wages, which is what is show in this next graph of average hourly wages divided by consumer prices to give us "real hourly wages":

Real hourly wages have improved over the last 12 months, but they are still below where they were all through 2009 and 2010.

So average Americans should care about the "taper." To the extent it causes interest rates to rise, interest rates you pay on any new debt are likely to go up. Refinancing of old debt will pretty much vanish. Further, at 7.5% unemployment, it is unlikely that real wages are likely to appreciate significantly, to say the least! Interest sensitive sectors of the economy, like home building, will likely deteriorate. With manufacturing already stagnant, the likelihood of falling into a new recession next year increases greatly (remember that interest rates are a long leading indicator, and increases tend to take a year or more to be felt in the real economy).

Finally, let me point out that in the above analysis, I am being like the Ghost of Christmas Future in "A Christmas Carol." I am not showing you what will be; only what might be. All of those bonds I mentioned above, being sold by traders? Other traders bought every single one. There are some people who think the upward move in interest rates is overdone, and they see a buying opportunity. In other words, there is no certainty that the Fed "taper" will cause interest rates to move higher than they already have. Even more importantly, Bernanke premised the "taper" on unemployment moving to 7% or below. If the economy slows because of anticipated or real higher interest rates, we won't see unemployment moving under 7%, and then the Fed is likely to reconsider and not "taper" at all! In other words, it could be a self-unfulfilling prophecy.

But the ultimate conclusion remains that average Americans are deeply and negatively affected by rising interest rates (not to mention what it means for interest paid on new national debt). If the "taper" means a rise in those rates, average Americans should be aware and should care.