One of the best short-term precursors to job growth (besides real retail sales) is GDP growth. Generally it takes 2% YoY GDP growth to generate job growth, so normalizing for that, there is a very clear relationship:

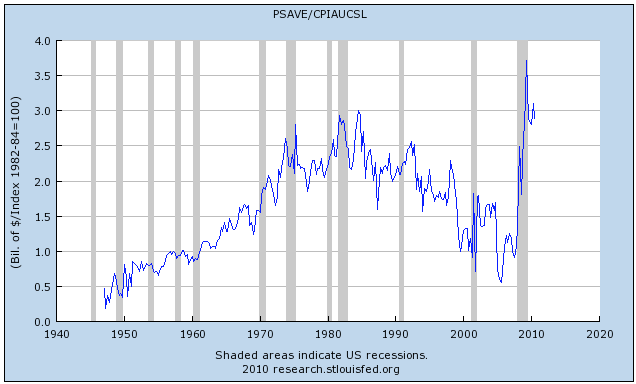

Among the best longer-term precursors, as I explained back in July, is the "real personal savings rate." To update this overview, first let's look at real, i.e., inflation-adjusted, saving. As you can see from this first graph, it is at the highest level in at least half a century:

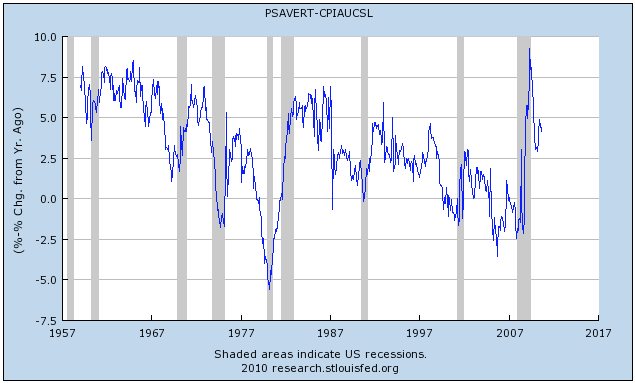

Now let's take this same data and translate it into the real, inflation-adjusted, savings rate.

This too briefly was at half-century highs at the very bottom of the recession. Since then the savings rate has declined, but is still in the higher range for the last several decades.

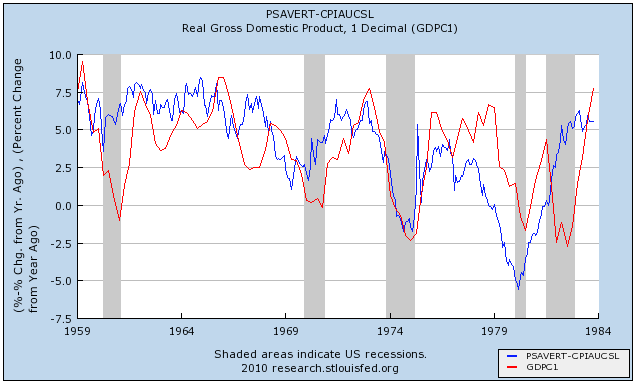

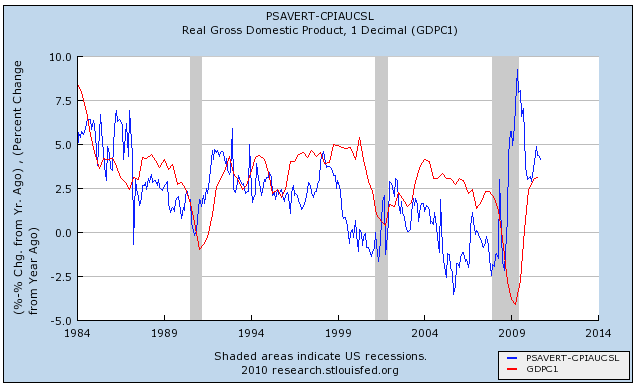

Now let's take the real personal savings rate (blue) and compare it with real GDP (red). Here is the relationship between 1959 and 1984:

and here is the same relationship from 1984 to the present (note: this is before this morning's data):

The relationship isn't perfect, but the lagged correlation is clear. A substantial change in the real personal savings rate is mirrored by a similar substantial change in real GDP about 6 to 18 months later. The logic of this isn't hard to follow: increased savings serve as the "tinder" that ignites subsequent spending. Once the spending starts, an economic boom begins. When the savings rate declines substantially, the fuel available for subsequent spending declines, and so does spending itself, with a lag.

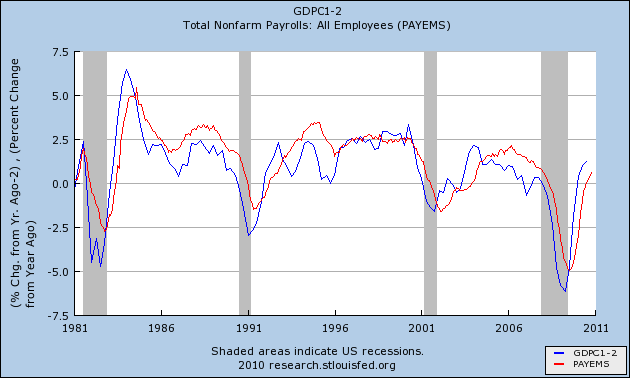

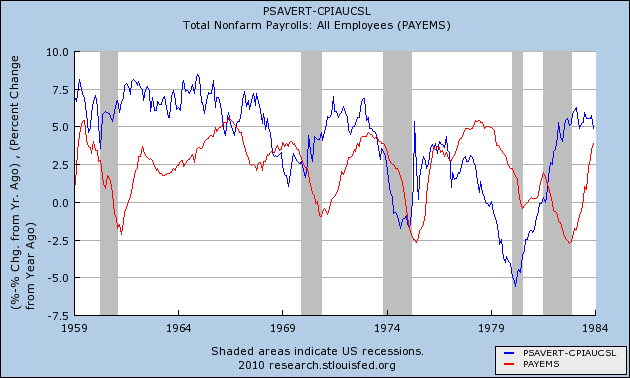

Since (1) the real personal savings rate leads real GDP; and (2) real GDP leads employment; let's put those two together and show the real personal savings rate (blue) and employment (red).

First, here is 1959 to 1984:

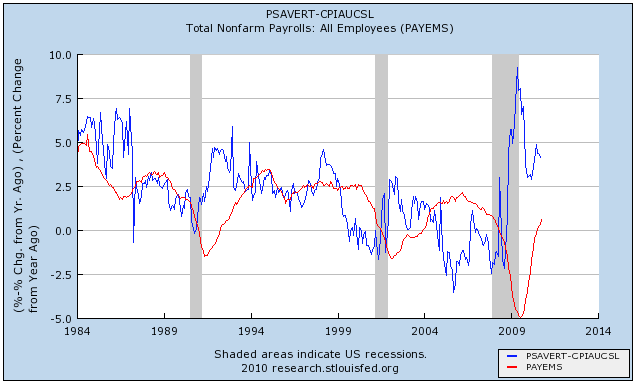

and here is 1984 to the present:

In summary, the real personal savings rate is a very good precursor for employment in a range of 18 to 30 months later. We are now 17 months past the June 2009 peak. This relationship predicts further increases in YoY job growth beginning about now and continuing in 2011.

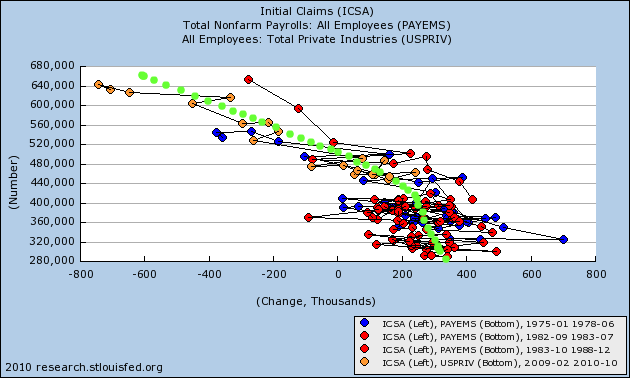

Needless to say, I am very encouraged by this morning's drop in initial jobless claims to 407,000, and the decline in the 4 week average to 436,000. Here is the trendline I drew on Monday comparing initial jobless claims with employment in the recoveries from the last two severe recessions:

Between real retail sales, declining jobless claims, a positive surprise in GDP, and a wellspring of fuel in the real personal savings rate, almost all engines are "GO" for a takeoff in robust job growth. Let's hope this is the beginning.