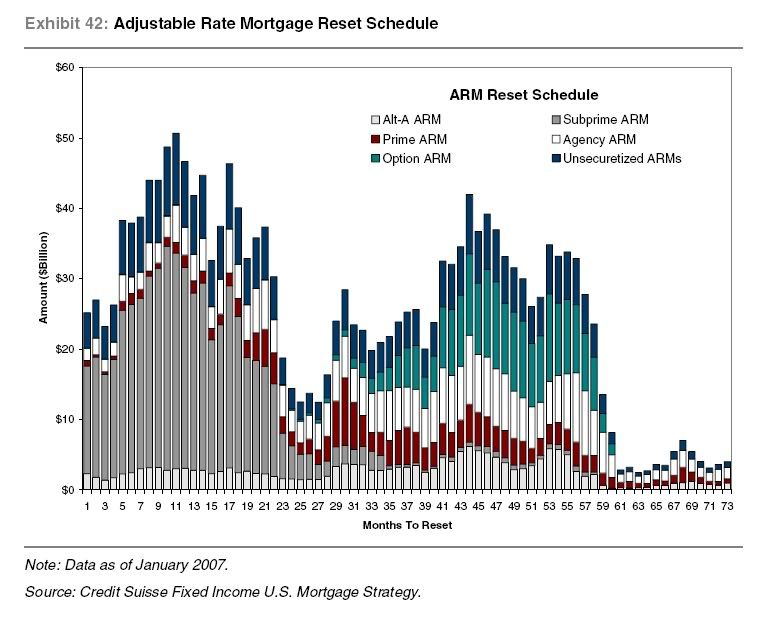

Almost six months ago I had a debate with another blogger who viewed the March increase in foreclosures over February as the beginning of a new "tsunami." The genesis of this story goes back to this graph and others like it that made the rounds beginning in 2006:

In the above graph, month 43 -- August 2010 -- marks the peak of those resets. While there is a similar graph which shows an even higher peak next year, like the graph above it shows an "eye of the storm" in mid 2008 and increases since then, so YoY increases in foreclosures should have resumed by now. So, today I am officially sticking a fork in the notion of a "foreclosure tsunami" due to those resets.

This morning Realtytrac reported that:

foreclosure filings -- default notices, scheduled auctions and bank repossessions -- were reported on 338,836 properties in August, a 4 percent increase from the previous month but a 5 percent decrease from August 2009. One in every 381 U.S. housing units received a foreclosure filing during the month.

The report further noted that, while:

Lenders foreclosed on 95,364 U.S. properties in August, the highest monthly total in the history of the report ... A total of 96,469 U.S. properties received default notices (NOD, LIS) in August, a 1 percent decrease from the previous month and a 30 percent decrease from August 2009 -- the seventh straight month where default notices have decreased on a year-over-year basis. Default notices peaked in April 2009, when 142,064 were reported nationwide.

In other words, old foreclosures were pushed to conclusion, while the pace of new foreclosure actions has slowed dramatically.

Here is an updated chart showing total foreclosure activity and YoY change for the last 19 months:

| Month | YoY % change | actual foreclosures |

|---|---|---|

| 04/2009 | +32 | 342,038 |

| 05/2009 | +18 | 321,480 |

| 06/2009 | +33 | 336,173 |

| 07/2009 | +32 | 360,149 |

| 08/2009 | +18 | 358,471 |

| 09/2009 | +29 | 343,638 |

| 10/2009 | +19 | 332,292 |

| 11/2009 | +22 | 306,627 |

| 12/2009 | +15 | 349,519 |

| 01/2010 | +15 | 315,716 |

| 02/2010 | +6 | 308,524 |

| 03/2010 | +8 | 367,056 |

| 04/2010 | -2 | 333,837 |

| 05/2010 | +1 | 322,920 |

| 06/2010 | -7 | 313,841 |

| 07/2010 | -10 | 325,229 |

| 08/2010 | -5 | 338,836 |

It bears emphasizing that the rate of foreclosures isn't "good", in fact it's very bad. But if the new wave of re-amortizing mortgage resets were going to result in a foreclosure tsunami, it surely would have manifested itself by the crest of that new wave. It hasn't. Foreclosure activity probably has been driven not by mortgage resets, but by stabilization in home prices and stabilization in jobs. The fundamental position of homeowners did not change for the worse in the last year.

Thus, there may yet be an echo-foreclosure increase due to renewed house prices declines - not mortgage resets - in the next couple of years. RealtyTrac's spokesman, Rick Sharga, suggested as much a month ago, indicating his belief that foreclosure activity probably won't peak until next year.

Nevertheless, the idea that an increase in resets would lead to a foreclosure tsunami at this point has to be regarded as a myth that has been busted.