- by New Deal democrat

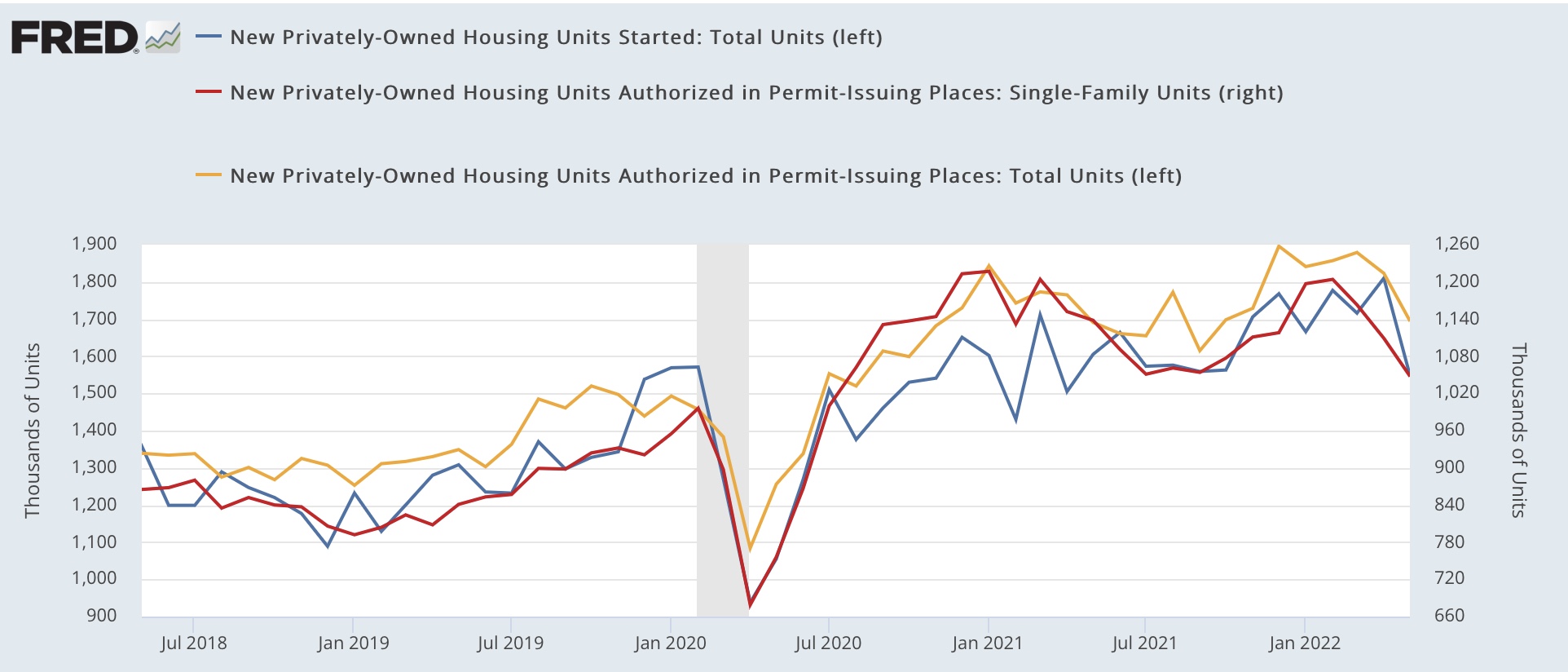

Housing permits and starts declined across the board in May.

In the past year there has been a unique divergence between permits and starts due to construction supply shortages. This has been reflected in the number of housing units authorized but not started increasing to a near-50 year records of 298.4 in March. In May that number increased from April by 1.5 million annualized to 287.6:

For the month, single family permits (red above, right scale) declined 61,000 annualized to 1.048 million, a 22 month low. Total permits declined 128,000 to 1.695 million annualized, an 8 month low, and starts declined for the month by 261,000 to 1.549 annualized, a 13 month low.

Finally, below is the most recent version of a graph I have run many times in the past 10 years, showing that mortgage interest rates (red, inverted *10 for scale) lead housing permits (gold) and starts (blue):

Interest rates are higher by 2% vs. one year ago. As the graph shows, the last time the comparison was this bad was 1994, resulting in a 20% decrease in permits and starts the following year. Both permits and starts have now turned negative YoY.

The “demographic tailwind” that buoyed housing activity 5 and 10 years ago has dissipated, as the number of 25-35 year old first time buyers has stopped increasing. Thus I expect a 20% YoY decline in housing permits and starts to manifest over the coming 12 months.

The conundrum is whether the 50 year high backlog in units not yet started will delay the downturn until it clears - which might take another 6 to 12 months. Since starts are the actual economic activity, until I see an unequivocal downturn there, the massive negative signal from permits, mortgage rates, and mortgage applications remains open to question.