- by New Deal democrat

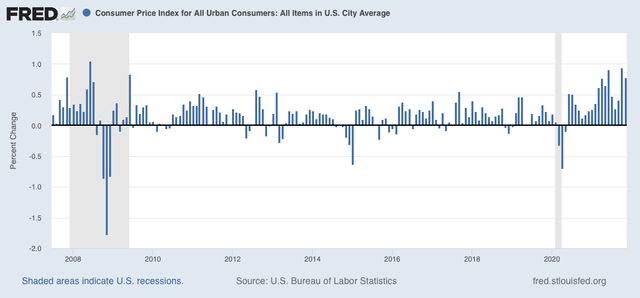

As you may already know, consumer prices increased 0.8% in November. In the past two months, there has been a re-acceleration in CPI, with the monthly numbers equal to earlier this year and the worst since the Great Recession:

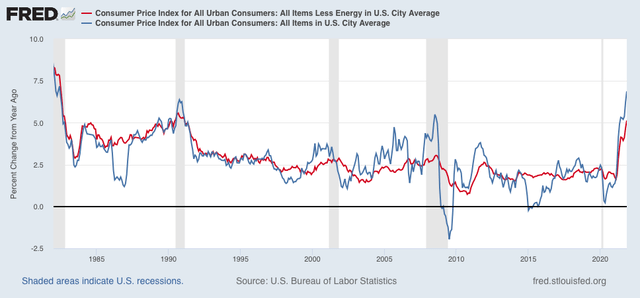

On a YoY basis, consumer inflation is now the highest since the big Reagan recession of 1981-82. My favorite measure, CPI ex energy, is also up 5.1% YoY, the worst in 30 years:

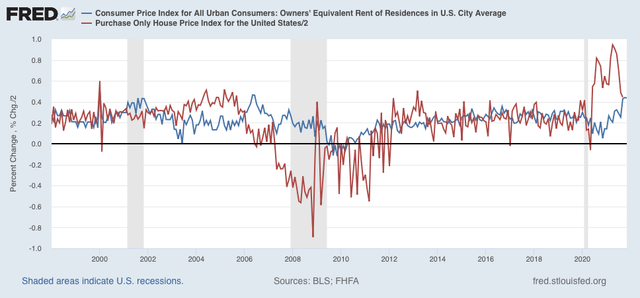

Inflation has shown up in all the wrong places: houses, cars, and gasoline. And remember that house prices are only indirectly reflected via owners’ equivalent rent, which has also started to increase:

Aside from the fact that “real” wage income has indeed actually declined this year (as I’ll discuss immediately below), the impact of house prices on consumers’ inflation concerns is an important factor that among others even Paul Krugman is missing (because he’s looking at only the “official” CPI stats, which do not include house prices).

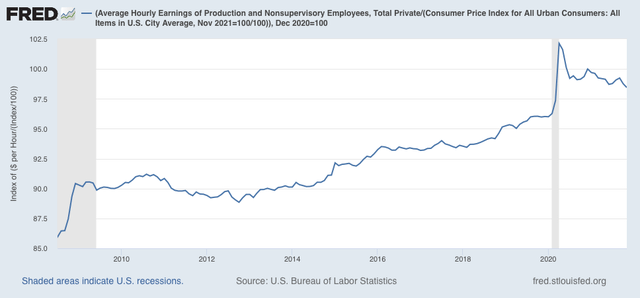

Average real hourly wages also declined again, down another -0.3% at -1.6% below their recent peak last December and about 3% below their peak in spring 2020:

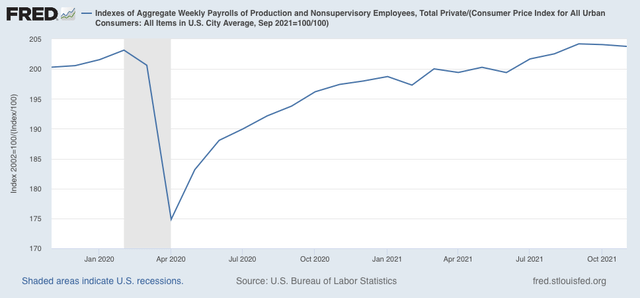

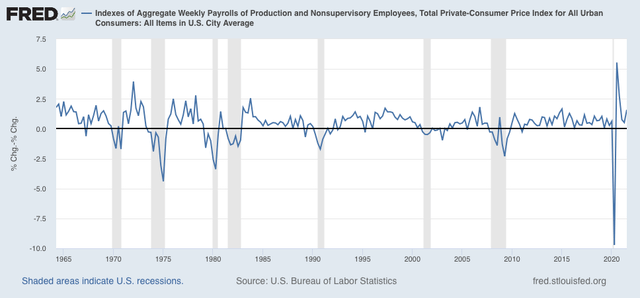

Further, real aggregate payrolls, an overall measure of consumer health, also declined -0.1%, and are -0.2% below their peak in September:

This is significant, because for the past 50+ years, when aggregate real wages have retreated from peak for 3 to 9 months, a recession has typically followed:

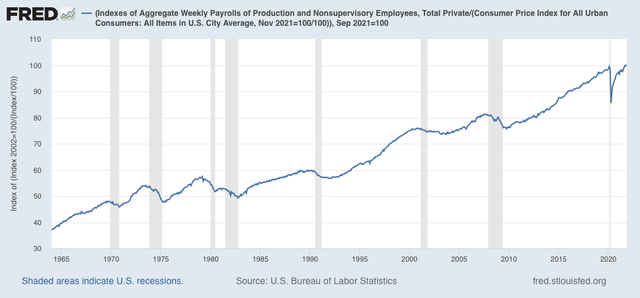

Measured quarterly, a -0.3% decline in real aggregate wages from the previous quarter has more often than not signaled a recession, and even when a recession has been avoided (e.g., 1967 and 1995) GDP growth has typically slowed dramatically (note: graph ends with September data):

Last month I wrote that inflation was “a Big Deal,” because it showed that consumers were already under pressure, and because, via owners’ equivalent rent, we could expect higher inflation to continue next year. Today’s report only reinforced that concern. While we haven’t crossed a threshold at this point into a downturn consistent with a recession, we certainly are at a point where a sharp deceleration beginning with the consumer sector of the economy is more likely than not.