- by New Deal democrat

Yesterday’s JOLTS report for August showed a jobs market that is still just beginning to mend. Hires were up, and layoffs and discharges were down, which is good, but job openings and voluntary quits both declined.

We are far enough along past the worst of the pandemic jobs losses that it is worthwhile to compare the state of the various JOLTS components with the 2 previous recoveries from recession bottoms in the series’ histories (this because the JOLTS data only dates from 2001.

In the two past recoveries:

Let’s examine each of those in turn. In each case, I break out 2001-19 in a first graph and then this year in a second.

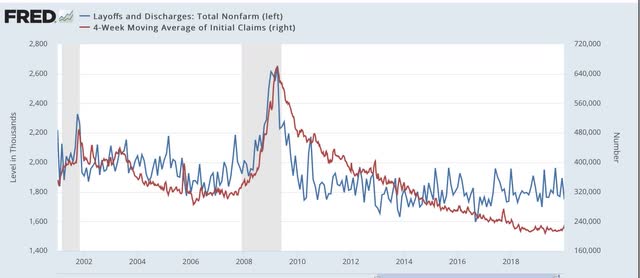

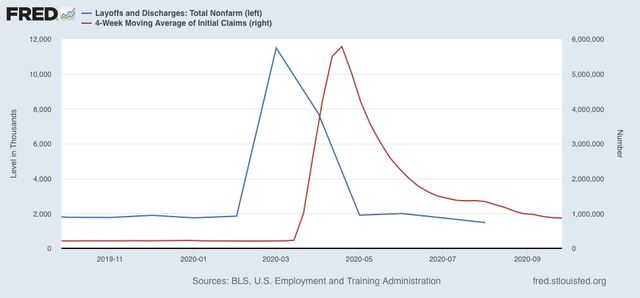

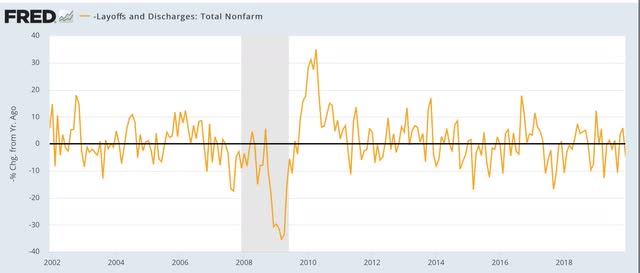

This first graph compares layoffs and discharges (blue) with the 4 week average of initial jobless claims (red):

You can see that, by the end of the recessions, layoffs were already declining, and continued to decline steeply over the next 3-8 months before reaching a “normal” expansion level. The turning point coincides exactly with the much less volatile, but more slowly declining, level of initial jobless claims.

The same has been the case this year, as layoffs and discharges already declined to their “normal” level in May, while initial jobless claims peaked one to two months later, and have been declining (slowly) ever since.

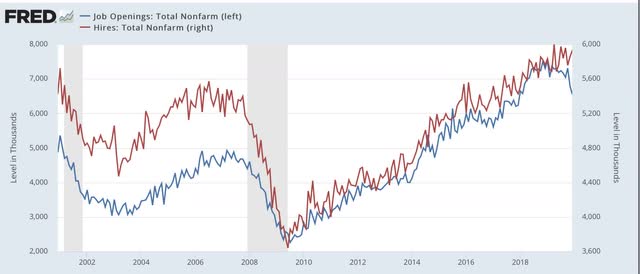

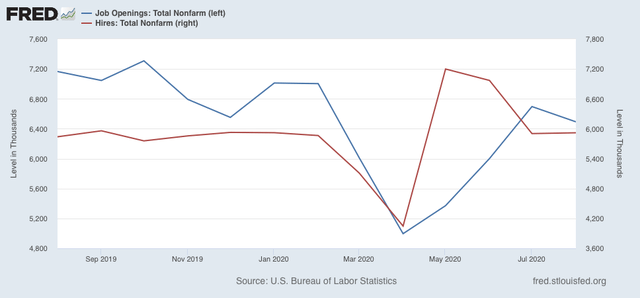

Next, here are hires (red) and job openings (blue):

You can see that actual hires started to increase one to two months before job openings.

This year, both made troughs in April, but hires rebounded sharply in May and June compared with job openings.

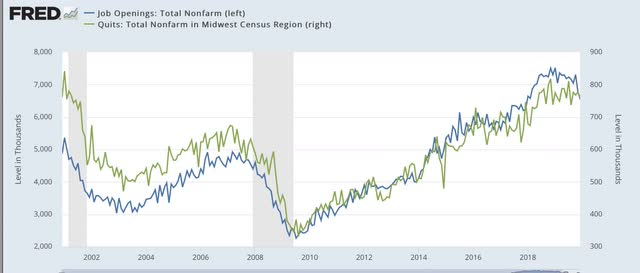

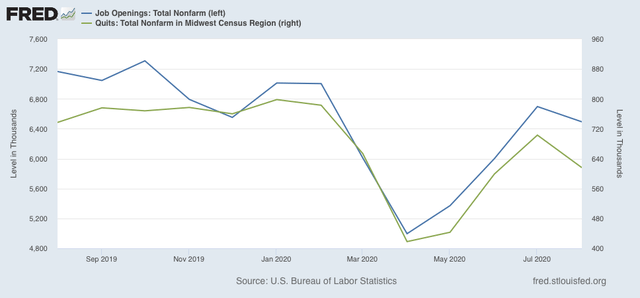

Finally, here are quits (green) vs. job openings (blue):

Actual hiring started to rise slightly before quits made a bottom. After that, both rose more or less together (suggesting it is openings that leads to the increase in voluntary quits)

Focusing on the past year, we see that both made a trough in April, and have risen equivalently since.

Although there has been some variation, the past several months have recapitulated the pattern from the last two early recoveries: the first two data series to turn - layoffs and hires - have indeed turned, while the last two - job openings and voluntary quits - have appeared to bottom but have had a much less dramatic rise.

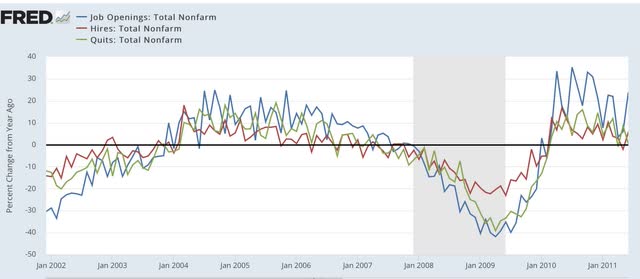

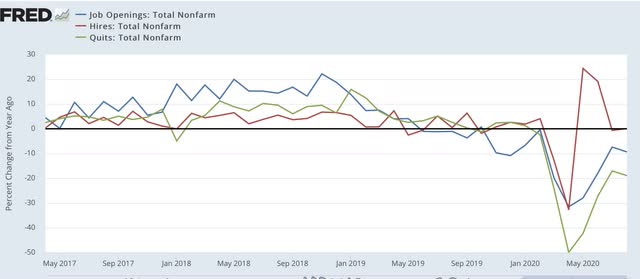

Because seasonal adjustments might not be giving us a true picture during this pandemic year, here are job openings (blue), hires (red), and voluntary quits (green), measured YoY without seasonal adjustments for the recoveries after the 2001 and 2007-09 recessions:

We are far enough along past the worst of the pandemic jobs losses that it is worthwhile to compare the state of the various JOLTS components with the 2 previous recoveries from recession bottoms in the series’ histories (this because the JOLTS data only dates from 2001.

In the two past recoveries:

- first, layoffs declined

- second, hiring rose

- third, job openings rose and voluntary quits increased, close to simultaneously

Let’s examine each of those in turn. In each case, I break out 2001-19 in a first graph and then this year in a second.

This first graph compares layoffs and discharges (blue) with the 4 week average of initial jobless claims (red):

You can see that, by the end of the recessions, layoffs were already declining, and continued to decline steeply over the next 3-8 months before reaching a “normal” expansion level. The turning point coincides exactly with the much less volatile, but more slowly declining, level of initial jobless claims.

The same has been the case this year, as layoffs and discharges already declined to their “normal” level in May, while initial jobless claims peaked one to two months later, and have been declining (slowly) ever since.

Next, here are hires (red) and job openings (blue):

You can see that actual hires started to increase one to two months before job openings.

This year, both made troughs in April, but hires rebounded sharply in May and June compared with job openings.

Finally, here are quits (green) vs. job openings (blue):

Actual hiring started to rise slightly before quits made a bottom. After that, both rose more or less together (suggesting it is openings that leads to the increase in voluntary quits)

Focusing on the past year, we see that both made a trough in April, and have risen equivalently since.

Although there has been some variation, the past several months have recapitulated the pattern from the last two early recoveries: the first two data series to turn - layoffs and hires - have indeed turned, while the last two - job openings and voluntary quits - have appeared to bottom but have had a much less dramatic rise.

Because seasonal adjustments might not be giving us a true picture during this pandemic year, here are job openings (blue), hires (red), and voluntary quits (green), measured YoY without seasonal adjustments for the recoveries after the 2001 and 2007-09 recessions:

Note that, even taking out the seasonal adjustments, hires rebounded first, as they did after the 2001 recession. Quits and openings have moved generally in tandem.

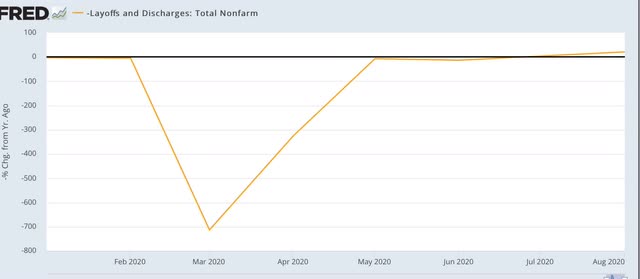

I have broken out layoffs and discharges separately below, because the their level in April and May of this year would obliterate all other variations (note: inverted so that fewer layoffs shows as positive):

This metric returned to normal almost immediately after both of the past two recessions, and did so again by July of this year.

In short, the pandemic recovery in summer was real in the jobs market, but remained in its early stages. I emphasize that the virus remains in control, and should there be a renewed out of control surge this winter, the jobs market will react equivalently.