Saturday, June 16, 2018

Weekly Indicators for June 11 - 15 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

There was a little whipsawing among some data, but the overall picture remains consistent.

Friday, June 15, 2018

May industrial production: meh

- by New Deal democrat

Industrial production is the ultimate coincident indicator. It is almost invariably the number that determines economic peaks and troughs.

In May it declined -0.1%. While that obviously isn't a positive, it does nothing to suggest any sort of change of trend:

and is in line with any number of similar monthly numbers during the expansion.

In this second graph I've broken it down into manufacturing (blue, left scale) and mining (red, right scale):

Again, there's nothing here to suggest any change of trend. In particular, the energy production sector of the economy which has done so much to undergird the overall number for the last 9 years, continued to improved.

So: meh.

May retail sales come in strong

- by New Deal democrat

Real retail sales for May came in strong, up +0.6% just in the month:

As the graph shows, this is on trend for the entirety of this expansion, and is also a new high, surpassing that of last winter.

Per capita real retail sales also made a new high, an indicator that the expansion is likely to continue at least one more year:

Finally, the YoY% growth in real retail sales has also been increasing:

Since this is a short leading indicator (3 to 6 months) of the trend in YoY% growth in employment, it suggests that the recent run of strong monthly jobs numbers should continue, averaging in about the 175,000 to 200,000 range over the next few months.

Earlier this week I wrote that real retail sales would show how well the average household is doing holding up, considering the stagnation of real wages over the last several years. Needless to say, the answer is "fine, so far."

Earlier this week I wrote that real retail sales would show how well the average household is doing holding up, considering the stagnation of real wages over the last several years. Needless to say, the answer is "fine, so far."

I hope to say much more on this at some point in the next week or two.

Thursday, June 14, 2018

The Fed's actions say "So much for symmetry"

- by New Deal democrat

Interest rates and money supply are the two long leading indicators under the control of the Fed. With yesterday's indication that they will hike 4 rather than 3 times this year, they are belying their statements that they will treat 2% core inflation as a target rather than a ceiling.

This post is up at XE.com.

Wednesday, June 13, 2018

Chewing over the message of online job postings

- by New Deal democrat

Here's an interesting graph I came across yesterday. It's from the Conference Board. What it does is track the number of job postings online, and breaks them down between first postings and repeat postings:

Let me say first of all that it is of limited use. The data only goes back to 2005, so there isn't much history -- heck, online job postings didn't even *exist* until the end of the 1990s! Further, online job postings have undergone a secular increase, as more and more companies have come to use it -- so I would expect the historical trend to be positive. But has it reached maturity? Or is it still in its growing stage? I dunno .... and probably neither does anybody else.

But with all those cautions, it struck me that the big gap between first time and repeat postings in of a piece with the gap between actual hires and job openings in the JOLTS series:

In the case of online job postings, the repeat postings are either trolling for resumes on an ongoing basis, or else evidence of inability to find a suitable candidate (at the wage the employer wants to pay) the first time around.

What is also interesting is how the two series converged beginning in 2006 as the 2007 recession approached. Which is what I would expect. As the job situation softens, I would expect companies to pull back on repostings more than original postings, as they become hesitant to go through with a hire if a good candidate does not appear promptly.

I'm not sure what to make of the decline in both during 2016-17. It certainly was not borne out by other employment data. But for now, the two series continue to diverge. That does not strike me as a sign that companies are skittish about hiring.

Tuesday, June 12, 2018

Gas- and housing-powered inflation mean real wages are going nowhere

- by New Deal democrat

This morning consumer price inflation for May was reported at +0.2%. YoY inflation was 2.8%. This is tied for the highest in six years (blue):

The cause of the increase was primarily twofold -- and neither one reflective of wage inflation. First, gas prices have increased by over 20% in the past year (red, right scale above).

Second, the costs for shelter (housing) are picking up steam again, up 3.5% YoY(red):

Note that, courtesy of gas prices, inflation for everything else except for shelter has also been rising (blue).

Most everyone assumes the Fed will raise rates again later this week. Let me point out, as others have as well (e.g., Dean Baker) that this will only make housing costs *more* rather than less expensive, and so will not serve to bring inflation down, short of causing a recession.

Meanwhile, while *nominal* wage growth for ordinary workers has finally been rising in the last few months, up 2.8% YoY:

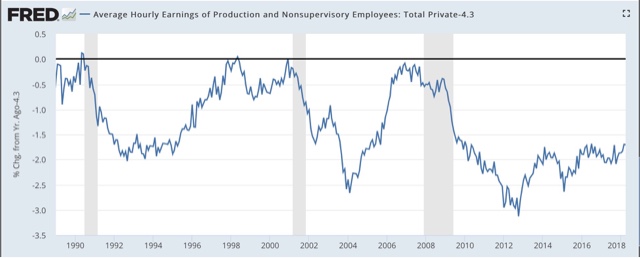

today's 2.8% YoY consumer inflation means that *real* wages haven't grown at all, up less than 0.1% YoY:

Further, since gas prices bottomed in winter 2016, *real* hourly wages have barely risen at all, as shown in the below graph normed to 100 as of February 2016:

Since that time, real wages have increased only 0.3%.

We'll get our best clue as to whether the ordinary American household is simply holding its own, or is in actually undergoing increased stress, when retail sales are reported later this week.

Monday, June 11, 2018

Update: wholesalers' sales and inventories -- it's all good

- by New Deal democrat

Another slow start to the data this week, so let's take a look at relationship I haven't updated in awhile.

Total sales in the economy are broken up into three categories: manufacturers', wholesalers', and retailers'. We'll get retail sales, the biggest component of the three, later this week.

But wholesalers' sales and inventories were released last week, and are a useful coincident barometer. They are a better measure than manufacturers' sales, since those have been very much secularly affected by the adoption of just-in-time inventory controls.

The important thing to remember is that sales (blue, left scale) lead inventories (red, right scale). Here's both for the last 20 years:

Note than in addition to the two last recessions, sales also plateaued first in 2012 slightly before inventory growth did, and again during the "shallow industrial recession" of 2016. As of April, both sales and inventory were both rising, a very typical result during an expansion.

Also, frequently commentators will write about gyrations in the inventory to sales ratio. But a comparison of the ratio (green, right scale) to the more leading measure of sales (blue, left scale) reveals that there the inventory to sales ratio only started to rise significantly coincident (literally, as of the same month) with the downturn in sales for each of the last two recessions as well as the shallow industrial recession of 2016.

Before that, any such upturn in the ratio was within the range of noise and so gave no meaningful signal. In other words, that inventories might be rising at a faster rate than sales doesn't give us information that is useful in terms of analyzing the business cycle. And, if anything, the trend in the ratio recently is downward.

So the overall message is that, for now, where sales are concerned, it's all good.

Sent from my iPad

Saturday, June 9, 2018

The disastrous German Emperor who was a doppelganger to Donald Trump: Kaiser Wilhelm

- by New Deal democrat

You know the drill. It's Sunday, so I write about whatever else is on my mind.

I am presently reading Miranda Carter's "George, Nicholas, and Wilhelm," her 2009 biography of the three grandchildren of Queen Victoria who were respectively, the King of England, Tsar of Russia, and Kaiser of Germany at the time of the outbreak of World War 1.

I was gobsmacked by her portrait of of Kaiser Wilhelm's character, for it is a virtually identical doppelganger to that of Donald Trump.

I was gobsmacked by her portrait of of Kaiser Wilhelm's character, for it is a virtually identical doppelganger to that of Donald Trump.

The best way to show that is via a few excerpts, presented with no embellishment.

First, a look at his "stable genius":

First, a look at his "stable genius":

"[Wilhelm] liked to think of himself as another Frederick the Great: politician, soldier, strategist, philosopher, cultural arbiter .... [But s]ome of those who had known him as a prince, however, worried a little about what kind of king he would make.... "He thinks he understands _everything_, even shipbuilding." Bismarck [ ] muttered about Wilhelm's inflated opinion of his own abilities ... and his minuscule attention span: he would "take a little peek ... learn nothing thoroughly and end up believing he knew everything." "

(pp. 75-76)

"Wilhelm considered himself an expert on many things and was not shy about saying so. In later years, he would personally inform the Norwegian composer Edward Grieg that he was conducting Peer Gynt all wrong; tell Richard Strauss that modern composition was "detestable" and he was "one of the worst"; and, against the wishes of its judges, withdraw the Schiller Prize from the Nobel Prize-winning German dramatist Gerhart Hauptmann, whose downbeat Ibsen-esque social realism he didn't like.

"[After, In 1889 in an attempt to smooth over some family difficulties, Queen Victoria had awarded Wilhelm an honorary admiralty of the Royal Navy,] Wilhelm fell upon his new title as if nothing had ever given him so much pleasure in his whole life..... Even Phillip zu Eulenburg noted disappointedly that he was "like a child over it [the British naval uniform]." Wilhelm told Herbert von Bismarck that his British naval title meant that "he would have the right as admiral of the Fleet, to have a say in English naval affairs and to give the Queen his expert advice... [He] was perfectly serious in what he said."

"...[Later that year,] Wilhelm put on his admiral's uniform, flew the pennant of a British navy admiral, and invited himself -- as a real admiral would -- to inspect the British squadron anchored [off the Greek coast].... In December, he sent [Victoria] a plan for the reorganization of the Royal Navy.... In 1891 he sent more "humble suggestions...." "

(pp. 90-93)

On his complete inability to maintain atttention, and wild vacillations:

"Wilhelm appeared unable to distinguish the trivial from the important -- he'd spend hours looking at photographs of warships or moving the position of the smoke stacks on a new cruiser, rather than read government reports.... Worse, he was an appalling vacillator, changing his mind -- he was often influenced by the last person he'd talked to, and constantly in quest of popularity -- with such frequency that it drove his ministers mad and made the government look irresolute and confused. Chancellor Captivi ... observed wearily that "he often contradicted his official announcements and misunderstandings arose in consequence." His colleague Marschall, the foreign minister, was more forthright: "It is unendurable. Today one thing and tomorrow the next and after a few days something completely different."

"Then there was his habit of making sudden rogue interventions, getting overexcited during speeches and announcing a new law that completely contradicted agreed government policy, or writing to foreign monarchs without telling the Foreign Office, or appointing someone completely inappropriate to a government position.... He was quick to resent anyone he felt wasn't sufficiently supportive."

(pp. 132-33)

On his existing in a completely different mental universe:

"...[T]he young kaiser [ ] showed not only an ability to flatly deny something that everyone else knew to be true, but a determination to see the world rather too much the way he wanted it to be...."

On his praeternatural ability to detect personal vulnerabilities:

"[Wilhelm] had an odd ability to home in on people's preoccupations and vulnerabilities.... There were moments when Wilhelm's probings hit a nerve ...."

(p. 151)

On his residing in a media bubble:

".... The truth was that, having laid claim to being Germany's savior and the most brilliant man in Europe, Wilhelm had proved quite unable to live up to his promise .... Although he'd told Captivi that the chancellor's job was just a temporary role until he himself was ready to take the reins of government, he had no staying power at all. "Distractions," Waldersee had observed increasingly bitterly, " ... are everything to him ... He reads very little apart from newspaper cuttings, hardly writes anything himself ... and considers those talks best which are quickly over and done with." Wilhelm was all front. He'd filled his first years as kaiser with a round of pageants, processions, parades and elaborate memorials .... "

(pp.132-33)

".... The truth was that, having laid claim to being Germany's savior and the most brilliant man in Europe, Wilhelm had proved quite unable to live up to his promise .... Although he'd told Captivi that the chancellor's job was just a temporary role until he himself was ready to take the reins of government, he had no staying power at all. "Distractions," Waldersee had observed increasingly bitterly, " ... are everything to him ... He reads very little apart from newspaper cuttings, hardly writes anything himself ... and considers those talks best which are quickly over and done with." Wilhelm was all front. He'd filled his first years as kaiser with a round of pageants, processions, parades and elaborate memorials .... "

(pp.132-33)

Carter's summary is that:

"Wilhelm manifested many symptoms of "narcissistic personality disorder": arrogance, grandiose self-importance, a mammoth sense of entitlement, fantasies about unlimited success and power; a belief in his own uniqueness and brilliance; a need for endless admiration and reinforcement and a hatred of criticism; proneness to envy; a tendency to regard other people as purely instrumental -- in terms of what they could do for him, along with a dispiriting lack of empathy."

(p. 93)

That the personalities of Kaiser Wilhelm and Donald Trump are so nearly identical is shocking.

(p. 93)

That the personalities of Kaiser Wilhelm and Donald Trump are so nearly identical is shocking.

As it turns out, moreover, I'm not the only one who has noticed this identity.

In March of last year, David E. Banks wrote in The Independent the two's similarities. Last October, the magazine Foreign Policy noted that "The Donald Trump - Kaiser Wilhelm Parallels are Getting Scary." Also last October, the Irish Times published .the following:

One of the foremost historians on the first World War war has compared US President Donald Trump to Kaiser Wilhelm II.

Professor Margaret MacMillan, the author of the bestselling book The War That Ended Peace, said Mr Trump shares many of the character traits of the Kaiser who led Germany into the first World War.

She describe those traits as giving the impression of being “reckless, inconsistent and belligerent”

Trump, rather like Kaiser Wilhelm II of Germany, is vain and has to be the centre of atte ntion. They both admire the military tremendously. There are a lot of parallels.

And finally, just this past week, Miranda Carter herself, excerpting some of the same quotes from her book that I have above, wrote in the New Yorker "What Happens when a Bad-Tempered Distractible Doofus runs an Empire?"

Perhaps the two most depressing takeaways from these comparisons is how Carter notes that other countries found it very easy to manipulate the Kaiser to their own advantage; and Prof. MacMillan's opinion that “He has done something to the US which will take a long time, if ever, to recover from.”

It would all be just rueful cynicism if Kaiser Wilhelm's bombastic aggressive narcissism hadn't been so pivotal to the miscalculations which exploded into World War.

It would all be just rueful cynicism if Kaiser Wilhelm's bombastic aggressive narcissism hadn't been so pivotal to the miscalculations which exploded into World War.

Weekly Indicators for June 4 - 8 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

While there were no big changes, the overall theme of slow deceleration continues.

Thursday, June 7, 2018

Gimme credit update: less demand, tightness for consumers

- by New Deal democrat

I take a more in-depth look at the provision of credit over at XE.com.

While credit is plentiful for producers, the situation looks tighter for consumers.

Wednesday, June 6, 2018

Brief JOLTS update

- by New Deal democrat

I'm still traveling, so this will be a quick update.

In re yesterday's JOLTS report, the main take seems to be that job openings were higher than the total number of unemployed, so presumably they could all be hired and we'd have actual full employment next month, right?

I don't think so. Month after month, hires have totaled considerably fewer than openings for several years. If full employment were so close, why wouldn't hires be catching up? And every month, there are new layoffs, quits, and other separations, all of whom (except for those who retire) are available to fill those job openings.

In any event, let me focus on the simple metric of "hiring leads firing." Here's the long term relationship since 2000, quarterly through the end of March:

No sign yet of either turning down, although both may be plateauing.

In the 2000s business cycle, hires YoY turned down well in advance of the recession. That isn't the case now:

so there's no danger sign of any oncoming economic downturn in this month's report.

Here is a close-up of the last several years, monthly, of hiring vs. separations:

The YoY comparisons will get more challenging starting next month, as hires have been within a 2% range since last May, and have not made a new high since last October.

Since we are late in the cycle, my anticipation is that we will indeed see negative YoY readings on hiring at some point in the second half of this year, but we'll see.

Tuesday, June 5, 2018

Wage growth: is the dam finally breaking?

- by New Deal democrat

[Apologies for the light posting: I've been traveling, and there isn't a lot of news this week.]

A couple of months ago I wrote that raising wages may have become a "taboo," i.e., that in some cases employers may be refusing to raising wages, even though it may be costing his money. One of the items I relied upon was from the NFIB, as small business owners presumably are not "monopsonies." As of February, the last time I had data, small business owners were complaining of inability to fill positions, but were not raising wages.

Over the last three months, that may have changed, as revealed in the NIFB survey from May. Let's compare hiring in small business through February:

and now through May:

In the last three months, employment growth per firm has finally broken out to the upside.

Meanwhile, unfilled job openings in small businesses, which have been soaring for the last five quarters (red dots, blue dot at end is for month of May):

are finally giving rise to actual wage increases over the last three months (red dots in the below graph are monthly):

This is supportive of the YoY% growth in average wages for nonsupervisory workers as of last week's employment report for May:

As I noted then, it looks like wage growth for ordinary workers may finally be starting to accelerate.

While it seems crystal clear that the tax cuts for large businesses are just going into stock buybacks, it is certainly possible that small businesses are using some of their extra cash to increase pay for new workers.

If the behavioral paradigm I hypothesized -- that the taboo against raising wages has been undergoing an extinction burst -- the most recent data from the NFIB supports that employers are finally conceding that the Great Recession-era behavior of freezing wages is no longer successful.

Saturday, June 2, 2018

Weekly Indicators for May 28 - June 1 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

The long leading indicators have now crossed a threshold.

Friday, June 1, 2018

May jobs report: excellent news on unemployment, underemployment, and wages

- by New Deal democrat

HEADLINES:

- +223,000 jobs added

- U3 unemployment rate fell -0.1% from 3.9% to 3.8%

- U6 underemployment rate fell -0.2% from 7.8% to 7.6%

Here are the headlines on wages and the braoder measures of underemployment:

Wages and participation rates

- Not in Labor Force, but Want a Job Now: up 68,000 from 5.115 million to 5.183 million

- Part time for economic reasons: down -37,000 from 4.985 million to 4.948 million

- Employment/population ratio ages 25-54: unchanged at 79.2%

- Average Weekly Earnings for Production and Nonsupervisory Personnel: rose $.07 from $22.52 to $22.59, up +2.8% YoY. This is the highest nominal YoY gain for the entire expansion. (Note: you may be reading different information about wages elsewhere. They are citing average wages for all private workers. I use wages for nonsupervisory personnel, to come closer to the situation for ordinary workers.)

Holding Trump accountable on manufacturing and mining jobs

Trump specifically campaigned on bringing back manufacturing and mining jobs. Is he keeping this promise?

Trump specifically campaigned on bringing back manufacturing and mining jobs. Is he keeping this promise?

- Manufacturing jobs rose 18,000 for an average of 22,000/month in the past year vs. the last seven years of Obama's presidency in which an average of 10,300 manufacturing jobs were added each month.

- Coal mining jobs rose 300 for an average of 110/month vs. the last seven years of Obama's presidency in which an average of -300 jobs were lost each month

The more leading numbers in the report tell us about where the economy is likely to be a few months from now. These were mixed.

- the average manufacturing workweek declined -0.2 hours from 41.0 hours to 40.8 hours. This is one of the 10 components of the LEI.

- construction jobs increased by 25,000. YoY construction jobs are up 286,000.

- temporary jobs decreased by -7800.

- the number of people unemployed for 5 weeks or less decreased by -81,000 from 2,115,000 to 2,034,000. This is a new post-recession low.

Other important coincident indicators help us paint a more complete picture of the present:

- Overtime declined -0.2 hours from 3.7 hours to 3.5 hours.

- Professional and business employment (generally higher-paying jobs) increased by 23,000 and is up +206,000 YoY.

- the index of aggregate hours worked in the economy rose by 0.2%.

- the index of aggregate payrolls rose by 0.5%.

Other news included:

- the alternate jobs number contained in the more volatile household survey increased by +293,000 jobs. This represents an increase of 2,582,000 jobs YoY vs. 2,363,000 in the establishment survey.

- Government jobs increased by 5,000.

- the overall employment to population ratio for all ages 16 and up rose 0.1% to 60.4 m/m and is up 0.4% YoY.

- The labor force participation rate declined -0.1% to 62.7 m/m and is unchanged YoY

SUMMARY

This was an excellent report with only a few drawbacks. Both unemployment and underemployment fell to rates not seen since the turn of the Millennium. Perhaps more significant, average hourly earnings for nonsupervisory workers increased at the highest rate since 2009. The trend over the last 6 months has been rising, and it appears that ordinary workers are finally getting a little wage traction.

Other good news included the continued decline in involuntary part-time employment, and the decline in short term unemployment to its lowest level in the expansion.

There were a few negative notes, including an increase in discouraged workers, a decline in the manufacturing workweek (which really just took back April's gain), a decline in the leading temp jobs number, and a deceleration in gains in the higher-paying business and professional category. Further, undoubtedly this report will signal to the Fed that it is OK to raise interest rates again.

This report was a continuation of the recent string of very good reports, as last autumn's big increase in consumer spending feeds through into jobs. I nevertheless expect the late cycle trend of deceleration to re-assert itself over the next few months.

Thursday, May 31, 2018

Corporate profits for Q1 2018 give caution signal

- by New Deal democrat

Corporate profits for Q1 were repored yesterday as part of the GDP update.

They are both a long leading indicator for the economy as a whole, and they also lead the stock market, when the latter is averaged quarterly. By both measures, they are flashing caution.

This post is up at XE.com.

Tuesday, May 29, 2018

More evidence of increasing deflationary pressure on wages

- by New Deal democrat

One of my pet peeves is that economics as a discipline needs to import the entirety of learning theory from psychology, not just parlor tricks like the endowment effect. For example, learning from models.

To wit, once Jack Welch was successful in using a pay scheme at GE that ensured that a given percentage of employees would not get a raise in any given year, it was inevitable that other employers who adopt the idea until it spread throughout corporate America. And it not giving raises to a certain percentage of employees was successful, why not implement it across the board with *all* employees?

Monkey see, monkey do.

As I noted several weeks ago, even though we are at least closing in on full employment, the percentage of employers not raising wages at all has gone up in the last year:

And now, cue Atrios about how big companies, fat with their new tax cut $$$, aren't planning on raising wages at all:

[E]xecutives of big U.S. companies suggest that the days of most people getting a pay raise are over .... [In] rare, candid and bracing talk from executives atop corporate America, made at a conference Thursday at the Dallas Fed[, t]he message [wa]s that Americans should stop waiting for across-the-board pay hikes coinciding with higher corporate profit ....

Monday, May 28, 2018

Memorial Day 2018

- by New Deal democrat

For all those, of whatever race, creed, color, or nationality, who gave their lives so that government of the People, by the People, and for the People shall not perish from the Earth:

Gettysburg National Cemetery

Antietam National Cemetery

May they rest in peace.

Saturday, May 26, 2018

Weekly Indicators for May 21 - 25 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

The primary movers -- in differing directions -- were interest rates, manufacturing, oil prices, and several housing-related metrics.

Friday, May 25, 2018

$3 a gallon gas has returned!

- by New Deal democrat

According to GasBuddy, as of this morning the average price of gas in the US is $3 a gallon:

This is the highest in 3 1/2 years. YoY gas prices are up a little over 25%.

I suspect that this is a significant psychological threshold. While it's not a "shock," which historically has caused Americans to cut back their spending by double the increased amount that they spend on gas, causing a recession, it might very well cause a 1:1 retrenchment, which will be felt by discretionary spending like restaurants. And, of course, it recirculates more of the currency outside of the USA into the treasuries of petroscheikhdoms.

An interesting byproduct is that the regional Fed districts which suffered the most from the downturn several years ago are turning in the best manufacturing and new orders growth in any of the districts now.

Thursday, May 24, 2018

Housing market shows no sign of stalling out yet

- by New Deal democrat

Now that all of the major reports are in, I take an extended look at the state of the housing sector.

This post is up over at XE.com.

Subscribe to:

Posts (Atom)