Saturday, April 8, 2017

Weekly Indicators for April 3 - 7 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

The thesis that trouble in the brick and mortar retail sector means We're DOOOMED!!!! is not borne out by the wider array of indicators.

Hot Air "Econ" Bloggers: Still Dumber Than a Box of Rocks

Thanks to a very busy work schedule, I've had less time to monitor and write about the "analysts" at Hot Air. But, now that I've got some time, let me play a bit of catch-up.

First, we have Ed's latest on the employment report, which contains this lovely observation:

The loss in retail jobs is curious, too. Consumer confidence hit a new high in March, part of an upward trend that started in … October 2016. We’ll get the 2017 Q1 GDP report at the end of the month, but the trend on personal consumption expenditures was good for the last three quarters of 2016, finishing with a 3.5% annualized quarter-on-quarter increase in Q4. Some big-box chains are struggling at the moment — JC Penney, Sears among them — so perhaps it’s more of an adjustment within the sector.

Actually, it's more than an "adjustment" within the sector. This may have escaped Ed's vast reading spindle, but there is a little outfit called "Amazon" that has completely upended the retail environment. It's led to several bankruptcies and numerous other store closings. In short -- it's not an "adjustment," it's a complete rethinking of the retail sector. Also observe what Ed doesn't note -- the 53,000 drop in construction jobs and the 50,000 decline in education and and health employment. It's almost as it he can't read a simple table or do simple math.

And then there's Jazz Shaw, the man who relentlessly crusades against increases in the minimum wage. How does his simple (and very incorrect) supply and demand analysis of a resource market jibe with this chart of the Seattle unemployment rate:

Despite raising the minimum wage to $15, Seattle's unemployment rate continued to drop and is now at 2.9%. Once again, the research of Alan Kreuger is born out at the expense of idiots like Jazz.

I realize that picking on the economic skills of Ed and Jazz is unfair. Neither have any formal training in the topic, so they're bound to get basic points wrong. But they continue to write horribly misguided analysis under the erroneous belief that they have meaningful analysis to offer. And that makes them fair game.

Once again, reality -- as in facts and data -- have intruded into Hot Air's little economic world to disprove their basic theories. Will they print retractions or corrections? No -- those are only required for the liberal press. Conservative bloggers have no such code of ethics.

Friday, April 7, 2017

March jobs report: participation up, unemployment down, wage growth miserly

- by New Deal democrat

HEADLINES:

- +98,000 jobs added

- U3 unemployment rate down 0.2% from 4.7% to 4.5%

- U6 underemployment rate down 0.3% from 9.2% to 8.9%

Here are the headlines on wages and the chronic heightened underemployment:

Wages and participation rates

- Not in Labor Force, but Want a Job Now: up +284,000 from 5.597 million to 5.781 million

- Part time for economic reasons: down -151,000 from 5.704 million to 5.553 million

- Employment/population ratio ages 25-54: up +0.2% from 78.3% to 78.5%

- Average Weekly Earnings for Production and Nonsupervisory Personnel: up $.04 from $21.86 to $21.90, up +2.3% YoY. (Note: you may be reading different information about wages elsewhere. They are citing average wages for all private workers. I use wages for nonsupervisory personnel, to come closer to the situation for ordinary workers.)

January was revised downward by -22,000. February was also revised downward by -16,000, for a net change of -38,000.

NOTE: Beginning next month, I will begin keeping track in the headlines of both manufacturing and mining job growth. Better news in these numbers was a central part of Trump's campaign, and after a 3 month grace period, I think it is fair to begin to see how well - or poorly - he is keeping that promise.

The more leading numbers in the report tell us about where the economy is likely to be a few months from now. These were positive with one exception.

- the average manufacturing workweek was fell from 40.8 hours to 40.6 hours. This is one of the 10 components of the LEI.

- construction jobs increased by +6,000. YoY construction jobs are up +177,000.

- manufacturing jobs increased by +11,000, and after being down YoY for a year, in the last two months have now turned up.

- temporary jobs increased by 10,500.

- the number of people unemployed for 5 weeks or less decreased by -232,000 from 2,566,000 to 2,324,000. The post-recession low was set nearly 18 months ago at 2,095,000.

Other important coincident indicators help us paint a more complete picture of the present:

- Overtime fell 0.1 from 3.3 to 3.2 hours.

- Professional and business employment (generally higher- paying jobs) increased by +56,000 and are up +639,000 YoY.

- the index of aggregate hours worked in the economy rose by 0.1 from 106.3 to 106.4

- the index of aggregate payrolls rose by 0.3 from 132.6 to 132.9.

Other news included:

- the alternate jobs number contained in the more volatile household survey increased by +472,000 jobs. This represents an increase of 1,699,000 jobs YoY vs. 2,185,000 in the establishment survey.

- Government jobs rose by +9,000.

- the overall employment to population ratio for all ages 16 and up rose +0.1% from 60.0% to 60.1 m/m and is up +0.2% YoY.

- The labor force participation rate was unchanged month m/m and YoY at 63.0%.

SUMMARY

While the headline for most summaries of this report will probably be the miss in the headline jobs number, the deeper trends appear to be a continuation of what we have seen for the last few months: significant declines in both the unemployment and underemployment rates, a continuing sharp increase in labor force participation (the biggest in nearly 30 years), but continuing wage growth stagnation. These trends are probably linked. The big move from people off the sidelines into the labor market is probably helping keep a lid on wage growth.

The only other negatives in the report is the stubborn high number of people outside of the labor force who want a job now, and the decline in the manufacturing workweek and overtime.

All in all, this was a quite positive late cycle jobs report, as the YoY% gain in jobs continues to decelerate, but remain positive.

Thursday, April 6, 2017

The return of the Doomers: OMG it's a slight pullback!

- by New Deal democrat

There finally was enough of a soft patch in the data for the Doomers to raise their heads out of the peepholes. They're still wrong.

This post is up at XE.com.

Wednesday, April 5, 2017

Jamie Dimon on labor force participatioin and disability

- by New Deal democrat

First of all, sorry for the light posting this week. I've had some urgent business I need to attend to irl.

But I wanted to post this for future reference. Via Business Insider, this is from Jamie Dimon's letter to stockholders:

If the work participation rate for this group [men ages 25-54] went back to just 93% – the current average for the other developed nations – approximately 10 million more people would be working in the United States. Some other highly disturbing facts include: Fifty-seven percent of these non-working males are on disability ....I don't know where he got the 57% statistic from, but if it is true it is potent evidence that the main factor behind the 60 year long decline in prime age labor force participation by men is an increase in those on disability, probably due to both the expansion of the program, and better longevity and diagnostics -- and probably also tied in to opiate addiction as well.

Sunday, April 2, 2017

Saturday, April 1, 2017

Weekly Indicators for March 27 - 31 at XE.com

- by New Deal democrat

The vast majority of all indicators remain very positive. This post is up at XE.com

Friday, March 31, 2017

Positive Q4 2016 profits help long term outlook

- by New Deal democrat

Corporate profits are a long leading indicator, but they are reported with a long lag. So Q4 2016 profits were finally reported yesterday. This post is up at XE.com.

Thursday, March 30, 2017

Does productivity growth lead to wage growth? "Not really, no."

- by New Deal democrat

I've seen a few articles recently claiming that low wage growth is because productivity by workers has been stalling. A convenient way to absolve the oligarchy.

Except, if the theory were true, we should see bigger wage gains in the sectors of the economy with the most productivity growth.

Well, some British researchers studied that, and here is what they found:

Does productivity growth help predict wage growth at an industry level? Not really, no. The distribution of productivity growth across industries is positively correlated with subsequent wage growth – industries with higher productivity growth now will tend to have higher wage growth in subsequent quarters. However, productivity growth has little additional value in predicting wage growth over and above univariate models....

The real conclusion is buried in the prior discussion:

These correlations may also tell us something about how an increase in productivity in a particular industry feeds through into real wages. Rather than bidding up relative nominal wages (and therefore, the relative RCW in that industry), an increase in productivity leads to lower relative prices for the output of that industry, increasing RPW for given nominal wage. This boosts the real consumption wages of workers in all industries.

So, productivity gains lead to a deceleration in consumer inflation, *not* better nominal wage growth.

Oops!

Ultimately, wage growth isn't about productivity. It's about bargaining power. And bargaining power is the biggest blind spot of most macroeconomic theory.

Wednesday, March 29, 2017

Wage growth and labor force participation: a Big Picture summation

- by New Deal democrat

The jobs and wages of average Americans is a major focus of my blogging, since they are a major component of Americans' well-being.

Recently I've written quite a bit about the labor force participation rate, especially about prime age individuals. In addition to the big secular influx of women into the workplace between roughly the mid-1960s into the early 1990s, there has been an almost remarkably steady slow decline averaging about -0.3% a year in prime age male participation, going all the way back to the 1950s!

A major element of the participation rate is comparison with other alternatives to being in the labor force.

Two alternatives to labor participation appear to have had a significant effect on the rate.

First, the cost of child care, which has soared over the last 15 years, compared with subdued (or paltry) wage growth has caused many women and some men as well in the prime age demographic to leave the labor force completely and instead raise their children as homemakers.

A second alternative, which appears to be a major determinant of the decline in male participation at least over the last 60 years is the expansion of disability insurance. This increase in disability has been mainly due to neck and back conditions, and together with improved longevity, has increased the incidence of long-term disability dramatically.

It has also been suggested that the huge increase in the incarceration rate from roughly 1980 through 2000 has also played an important role in depressing participation.

In several posts over the last week, I've suggested that the traditional Phillips curve which posited a relationship between lower unemployment and higher wage growth and inflation, is best seen as a special variant of a broader relationship between the labor force participation rate (i.e., the total of those both employed and unemployed). For 46 of the last 52 years it has been true under first a high inflation regime and secondly a low inflation regime that an increase in labor force participation has been correlated with more wage growth.

But on a secular basis, the correlation does not reflect direct causation. Rather, increased labor force participation (blue in the graphs below) appears to lead an improvement in wage growth (red) by about one year. Here's the high-inflation, high labor bargaining power 1960s and 1970s:

and there is the low inflation, low bargaining power era since 1988:

In both of these eras, generally participation led wage growth by about one year.

For completeness purposes, here is the transitional Reagan Administration:

In this transition period, labor bargaining power was curtailed sharply as was inflation. Even so, the leading/lagging relationship appears intact, as lower participation led lower wage growth by about a year.

A more nuanced cyclical feedback mechanism appears to be that too rapid an increase in participation will lead either to higher inflation (the 1960s and 1970s) or lower short term wage growth (the 1980s to present. To show that, below is a variation on the misery index. The "misery index" came out of the 1970s and added the inflation rate to the unemployment rate. In the graph below, I have double-weighted inflation. the only major departures between this "misery index" and labor force participation are the Oil shocks of 1974, 1979, 1990, and 2008:

Let me wrap up this compendium on labor force participation by applying this to our present situation. In the last 1 1/2 years, there has been one of the two biggest surges in participation in the last 30 years, meaning that wage growth has stalled out:

If this increase in the labor force is successfully absorbed into the economy, improved wage growth ought to resume as early as later this year.

Tuesday, March 28, 2017

Variations on the Phillips curve: labor force participation and wage growth

- by New Deal democrat

Over the last month or so, in a few posts I have looked at the relationship between labor force participation, wages, and unemployment. Last week I looked at several variations on the Phillips Curve -- the proposed relationship between inflation and the unemployment rate. While over a single business expansion the relationship seems to work, i.e., lower unemployment rates correlate with higher inflation, that hasn't been true over a longer term secular basis, and it specifically reverses during and after severe recessions, where higher (but declining) unemployment rates have been correlated with higher (and declining) inflation.

But a much tighter relationship appears to exist between the labor force participation rate (the total employed plus unemployed as a share of population) and wage growth:

We have two secular regimes where higher participation is correlated with higher wage growth separated by a brief transition where higher participation was correlated with a sharp decline in wage growth.

Let's break it down. First, here are the inflationary 1960s and 1970s, where there was also a great deal of labor bargaining power due to strong unions:

Here is the low inflation late 1980s to the present, where there has been very little labor bargaining power:

In both of these cases, for a total of almost 45 of the last 50+ years, higher wage growth has been correlated with higher labor force participation.

Here is the brief transition period during the 1980s Reagan Administration, where both inflation and labor bargaining power sharply declined:

The bottom line is that, once we take into account labor bargaining power, there appears to be a very good and durable relationship between changes in prime age labor force participation and

growth in wages.

But of course, correlation is not causation, and I have suggested in prior posts that if anything, wage growth may lag labor force participation, with some complex mutual causation. I will wrap this thought process up in one final post later this week.

Sunday, March 26, 2017

A thought for Sunday: Thank You, Freedom Caucus!!! Plus, Democats should offer a plan to "Reform and Improve" Obamacare

- by New Deal democrat

First of all, thank the Great Flying Spaghetti Monster for the GOP's Freedom Caucus!!! They have been the best friends Progressives like myself could have hoped for.

Every time the mainline GOP or corporatist Democrats wanted to move the country back to 1929, the Freedom Caucus has insisted that nothing short of 1859 will do. By refusing to take "yes" for an answer, they have again and again -- in the Debt Ceiling Debacle of 2011, in the "Fiscal Cliff" of 2012, and again with TrumpRyancare this past week -- single-handedly kept the US in the late 20th Century.

Secondly, I hope the Democratic Party does not slip back into passivity on Obamacare simply because they have won this battle. I strongly suspect that the main reason Trump is implacably against "Obamacare" is because Obama humiliated him at the White House Correspondents' Dinner once upon a time, and he is nothing if not vengeful. He wants to obliterate Obama's legacy.

So Democrats need to make a big stink any time the Trump Administration undercuts Obamacare provisions to try to make it fail (as they have already done in several respects, e.g., state waivers).

Beyond that, Obamacare does have some significant problems. The individual mandate is hated, and the penalty isn't big enough. More young people need to buy in. Further, some of the Exchanges and health care provider networks are too narrow, and in a few states they are in big trouble. Complacency is not a winning strategy.

If Democrats truly care about making this country better for the vast majority of its population, now that most people are finally of the opinion that health care ought to be reasonably available to everybody, not just if their employer offers it, Democrats should respond to the GOP's deplorable "repeal and replace" efforts with a promise to "reform and improve" Obamacare should they gain a Congressional majority.

How would a plan to "reform and improve" Obamacare work? There is renewed talk of "Medicare for All" and if the public can be sold on that, I certainly have no problem. But I suspect the public is not interested in "Medicare for All." So what is a viable Plan B?

The goals ought to be:

1. universal coverage. Obamacare still leaves about 10% of the population uncovered.

2. better plans. Too many of the Bronze and Silver plans have sky-high deductibles and copays, making them little more than "junk insurance."

3. administrative efficiency. There are too many potential side-by-side bureaucracies: Medicare, Medicaid, SCHIP, private exchange providers, employer-provided insurance, auto and homeowner medical coverage, and potentially a "public option" provider. The less redundancy among providers, the more the cost savings which can be plowed into cheaper premiums and better coverage.

Two elements of a viable Plan B are well-known: the "public option" and age 55+ (or at least age 62+) Medicare buy-in. These will ensure wider choices, more competition, and to the extent older workers choose to retire early with the Medicare buy-in, lower premiums and a healthier risk pool in the Exchanges.

Additionally, Plan B ought to include a reform to abolish the individual mandate and penalty and replace them with automatic enrollment in a basic health care plan.

Here's how I envision it would work. Just like SS, Medicare, unemployment and disability deductions to paychecks, establish a Health Care automatic deductible. If your employer offers healthcare, the deductible is reduced by the amount of the premium, all the way to zero if applicable.

If your employer doesn't offer healthcare, if you are under age 40, you are automatically enrolled in the least expensive Bronze plan in your state. If you are 40 or older, you are automatically enrolled in the least expensive Silver plan in your state.

The deductible would also include a small contribution towards Medicaid. Then, if you are unemployed, you are automatically enrolled in Medicaid, but can continue with the silver or bronze plan as above if you choose.

The Kaiser Foundation estimated that in 2015, the average worker paid about $1200 per year for their employer provided health care, and the employer picked up another $4800 for a total of $6000 per year. This out of an average annual salary of about $30,000. This boils down to roughly a 4% deduction from worker wages, with the employer kicking in 16% more.

So, just for example, let's make the automatic deduction the following:

2% for a 20 year old + another 0.1% for the unemployment medical coverage.

3% plus 0.15% for a 30 year old

4% plus 0.2% for a 40 year old

5% plus 0.25% for a 50 year old

6% plus 0.3% for a 60 year old

Employers would pick up the rest up to a total of $6000. The self-employed pick up both the employer and employee share, with subsidies as per existing Obamacare.

Remember that if the employer is already providing coverage, that is counted against the payroll deduction. and the deduction ought to kick in gradually, e.g., 1% a year, so that employees do not sustain any acutal nominal losses.

Now you have a social insurance program that provides universal coverage. And we know that social insurance programs like Social Security, etc., are very popular.

Now you have a social insurance program that provides universal coverage. And we know that social insurance programs like Social Security, etc., are very popular.

Dems could turmpet such a plan to "Reform and Improve" Obamacare, and campaign on pushing for it if they get a Congressional majority. Heck,call it Trumpcare and President Caligula might even sign on!

Saturday, March 25, 2017

Weekly Indicators for March 20 - 24 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

Among the entire array of indicators, only 3 were negatives this week.

Friday, March 24, 2017

Leading housing data continues to be positive

- by New Deal democrat

We now have all of the February housing sales data. With the exception of the least important series, the trend in each continues to move in the positive direction.

This post is up at XE.com.

Thursday, March 23, 2017

Variations on the Phillips Curve: unemployment and underemployment

- by New Deal democrat

This is part of a longer post I wanted to write, and if FRED didn't play so poorly with iPad I would put it all up. But, having finished with my cursing, let me put up a truncated version now and follow up with another one sometime in the next week.

This picks up on my post from several days ago in which I noted that a fuller explanation of the cycle of wage gains should take into account the labor force participation rate for prime age workers. So I thought I would show the differences in how the Phillips Curve (the tradeoff between wages and unemployment) looks depending on how completely we look at it.

Let's start with the unemployment rate (bottom scale) vs. YoY nonsupervisory wage growth (left scale) since the series started in the 1960s:

It's pretty clear that there are two regimes, higher vs. lower wage growth (top vs. bottom). And if you were looking for a clean relationship in which lower unemployment equals higher wage growth, it ain't there.

But let's cull out the two big recessions and recoveries 1981-89 and 2007-17. Here's the 1980s:

and here's the last 10 years:

In each case, once unemployment gets low enough, increased wage growth does kick in. But before that, we see wage growth falling as unemployment increases during the recession -- and continuing to decrease in the earlier part of the recovery thereafter while unemployment remains relatively high (over 7% or so).

Here's the same scatterplot for the U6 underemployment rate:

The traditional Phillips Curve gained prominence during the post-WW2 era when unemployment remained relatively low for nearly 30 years. Now we can see that it is only part of the story. It only holds true when the unemployment and underemployment rates are low enough. At higher un(-der)employment rates, whether going into or coming out of recessions, wage growth decelerates even if unemployment or underemployment are decreasing.

Wednesday, March 22, 2017

A look at yield curve compression

- by New Deal democrat

Since the mid-1950s, an inverted yield curve has been perhaps the single most deadly harbinger of a recession in the next 1-2 years. The most typical measurement has been the spread between 10 year and 2 year treasuries:

Typically these inversions have happened because the Fed raised interest rates in an effort to tame inflation deemed to high. Thus, because we are in a very low inflation and interest rate environment, I suspect this version of the yield curve is one of the most likely long leading indicators to fail to signal before the next economic downturn. Most notably, the yield curve between short term and long term bonds never inverted at all between 1931 and 1954, as indicated by calculating the spread of the archival "long term government securities" data with 3 month treasuries:

My suspicion is -- and here unfortunately I do not have any old data to compare with -- that a compression at closer points along the yield curve is likely to be a more accurate signal in this environment. To show you why, let's take a look at the spread between 30 year and 10 year treasuries (blue in the graphs below), 10 year and 5 year treasuries (red), and 5 year and 2 year treasuries (green).

Here is 1977 to 1997:

and here is 1997 to 2017:

The first thing I want to point out is that in advance of all recessions in the last 40 years, yield curve inversions happened across the board. All three measures inverted.

Secondly, a compression of all three measures on the order of +0.5% or less was associated with stock market corrections (in the case of 1987, a crash!), but not an outright recession in the near future.

Finally, the most likely measure to invert, including a number of "false positives" for recessions, was the 30 year minus 10 year measure.

With that in mind, let's focus on the last 5 years:

In this era of very low rates, the shortest term measure (5 year minus 2 year) has crossed the +0.5% threshold to the downside several times. The measure next out in the range (10 year minus 5 year) crossed once -- the middle of last year. The longest term measure (30 year minus 10 year) has never crossed the threshold.

We can put this information together by calculating the average spread among the three measures, by taking each value, adding them together, and dividing by 3. When we do so, here's what we get:

No matter how you look at it, at least compared with the last 40 years, no aspect of the yield curve is signaling any danger now.

But if we suspect that it is not necessary for the yield curve to outright invert before the next recession (noting how little of an inversion there was in 2006 before the 2008 recession), then at least we can raise the caution flag in the event that either one or both of the following two things happens: (1) all three term measures declined below +0.5%; and/or (2) the average of the three term measures declines to +0.3% or less.

It is certainly not a perfect work-around. Although the data series are different, no compression at all between long term and 3 month securities occurred before the 1945 demobilization recession, nor before the severe 1938 recession (which appears to have been caused fiscally rather than by Fed action).

But even so, if we think that this low interest rate and inflation environment will function more like that of the 1920s-early 1950s, then measuring yield curve compression across maturities will at least keep us on our toes.

It is certainly not a perfect work-around. Although the data series are different, no compression at all between long term and 3 month securities occurred before the 1945 demobilization recession, nor before the severe 1938 recession (which appears to have been caused fiscally rather than by Fed action).

But even so, if we think that this low interest rate and inflation environment will function more like that of the 1920s-early 1950s, then measuring yield curve compression across maturities will at least keep us on our toes.

Tuesday, March 21, 2017

What's behind stalled nonsupervisory wage growth?

- by New Deal democrat

Wage growth for nonsupervisory workers nominally has been stuck in the +2.3% to +2.5% range (or worse) for three years. Why?

Over the weekend I was cleaning out some old graphs, and came across this one from the Atlanta Fed, suggesting that the Phillips Curve (the tradeoff between unemployment and inflation) is very much alive, with the tweak that the amount of wage growth follows a decline in the unemployment rate with a one year lag:

Over the weekend I was cleaning out some old graphs, and came across this one from the Atlanta Fed, suggesting that the Phillips Curve (the tradeoff between unemployment and inflation) is very much alive, with the tweak that the amount of wage growth follows a decline in the unemployment rate with a one year lag:

The red line is the progression of the Phillips Curve since the beginning of 2011. The dotted line indicates that the Altanta Fed's model was calling for a significant acceleration of wage growth between the spring of 2016 and spring this year. [NOTE: all of the discussion in this post is about nominal, not inflation-adjusted wage growth, which has an awful lot to do with the volatility of gas prices.]

Except when we look at wages for nonsupervisory workers, that really hasn't happened, at least not through February. The below graph compares the YoY change in the unemployment rate (blue) and YoY wage growth for nonsupervisory workers (red):

As noted above, wage growth has been stuck at between 2.3% YoY and 2.5% YoY with some (mainly negative) exceptions since the end of 2013.

Using the U6 underemployment rate to capture the broader picture doesn't change the outcome:

So, what's going on?

I suspect that the change in the labor force participation rate (i.e., that portion of the population actually in the job market, whether employed or unemployed) is the answer.

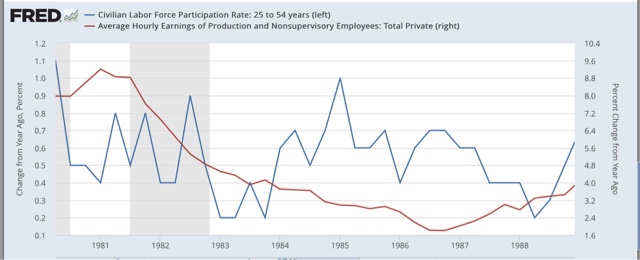

When I use the labor force participation rate for the prime working age population (ages 25-54) (blue) and measure that YoY vs. wage growth, even going all the way back over half a century to 1964, here's what I get:

With the very significant exception of most of the 1980s, the trend in prime age labor force participation appears to lead the trend in wage growth by one to two years.

What is most interesting is that in the era of labor force bargaining power (up until about 1982), a big increase in the labor force lead to a considerably larger amount of wage growth. Once labor's bargaining power was broken during the early part of the Reagan Administration, the big secular increase in labor force participation did not show up as wage growth inflation, but rather as more job growth with outright *decreases* in the average hourly wage.

Note further that since the late 1980s, twice an increase of +0.6% YoY in prime age labor force participation has led to nominal wage growth of +4.0 YoY about one year later.

Now let's zoom in on the last 5 years. The below graph compares the growth in employment (blue) averaged over each half year, with that of the overall labor force participation rate (red) and the prime age participation rate (green):

What is interesting is that over that entire time, average employment gains over each period have not varied that much. What *has* happened, especially notably with those of prime working age, is a temporary pause in the decline in early 2014 and 2015, coincident with the first stalling and then decline in wage growth, and then a surge of participation in 2016, especially during the first half of the year.

To put this in perspective, the participation among the prime 25 - 54 age group plateaued beginning in 1989 (after the secular rise due to women entering the labor force):

So here is the YoY change in the participation by those in prime age since that time:

The YoY change in participation in the last two quarters of 2016 (the last two bars) averaged +0.65%. That is the biggest such increase in participation in the last 30 years!

Putting this together, it appears that the surge in new participation in the labor force, with no surge of employment growth, showed up in a pause in the decline of the unemployment and underemployment rates. As shown below, in the year from September 2015 through September 2016, the unemployment rate only fell -0.1%, from 5.0% to 4.9%. The U6 underemployment rate only fell -0.3%, from 10.0% to 9.7%:

Putting this together, it appears that the surge in new participation in the labor force, with no surge of employment growth, showed up in a pause in the decline of the unemployment and underemployment rates. As shown below, in the year from September 2015 through September 2016, the unemployment rate only fell -0.1%, from 5.0% to 4.9%. The U6 underemployment rate only fell -0.3%, from 10.0% to 9.7%:

This surge in competition for new jobs acted to depress wage growth.

If the long-term graph comparing wage growth and the prime age LFPR is correct, however, and particularly if the same pattern of the late 1980s and 1990s is followed, then the surge in the LFPR does portend a significant acceleration in wage growth for nonsupervisory employees -- finally -- later this year. That the U6 underemployment rate has declined significantly again in the last 3 months is supportive of that suggestion.

If the long-term graph comparing wage growth and the prime age LFPR is correct, however, and particularly if the same pattern of the late 1980s and 1990s is followed, then the surge in the LFPR does portend a significant acceleration in wage growth for nonsupervisory employees -- finally -- later this year. That the U6 underemployment rate has declined significantly again in the last 3 months is supportive of that suggestion.

We'll find out soon enough.

Monday, March 20, 2017

Saturday, March 18, 2017

Weekly Indicators for March 13 - 17 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com. This week it is pretty self-explanatory. Nearly all short leading and coincident indicators are positive.

Subscribe to:

Posts (Atom)