- by New Deal democrat

The former King of Coincident Indicators, industrial production, has faded ever since the “China shock” at the beginning of the Millennium. Downturns in production almost always coincided with the onset of recessions beforehand. Since then, there have been several big downturns, in 2015-16, 2019, and a smaller one in 2023-24, without recessions having occurred.

The headline number in this morning’s report for March, a decline of -0.3%, is somewhat misleading. That’s because it includes utilities, which had all time highs in January and February more than 5% higher than at any time before the pandemic, and over 3% higher than any prior post-pandemic measure (possibly a combination of an particularly cold winter and crypto mining), declined -5.8% in March. The below graph is normed to 100 as of the pre-pandemic record in April 2018:

When we strip out utilities and just look at manufacturing production (red in the graph below), March saw a 0.3% increase to a new post-pandemic record, in contrast to the headline decline (blue):

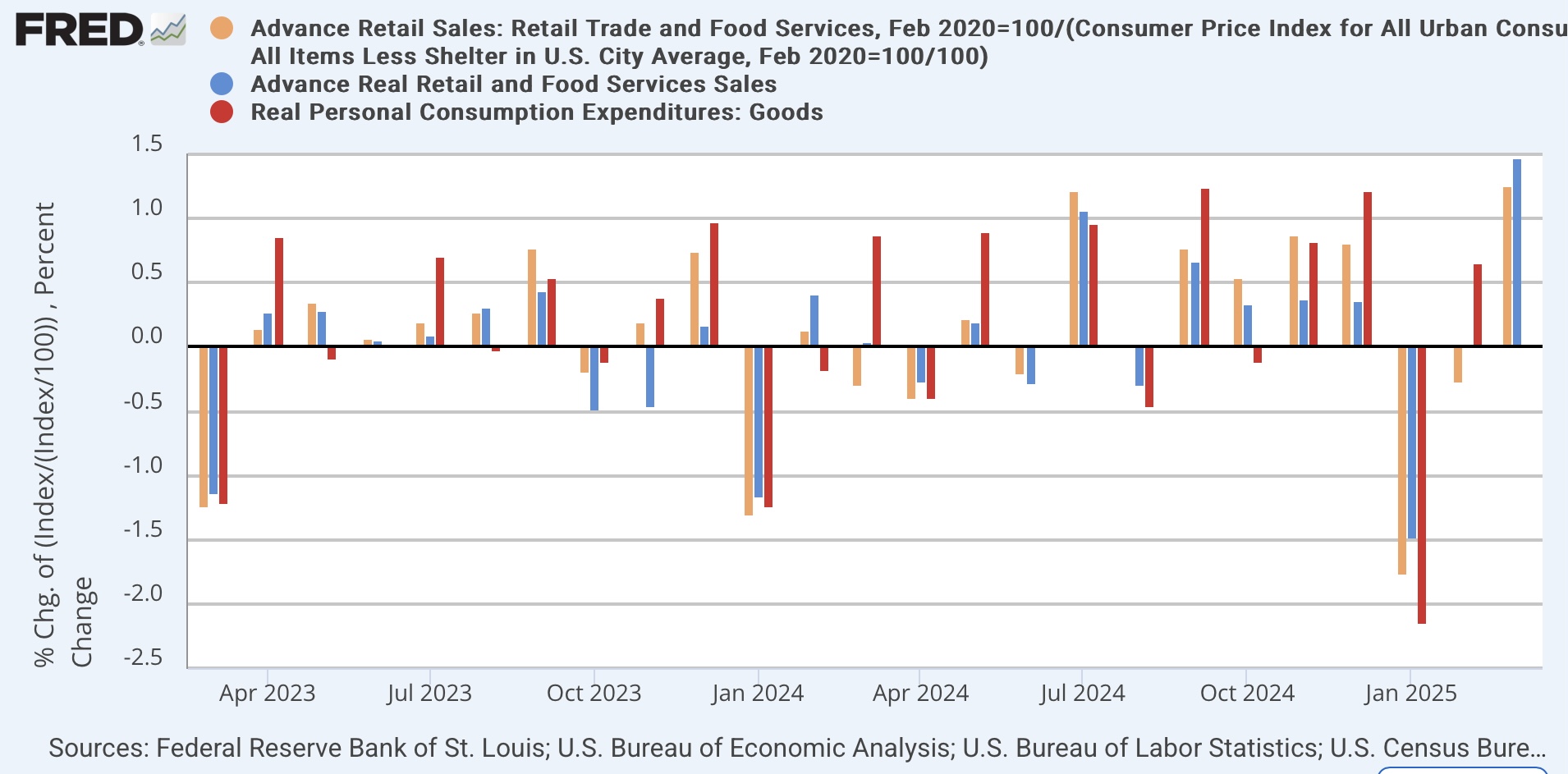

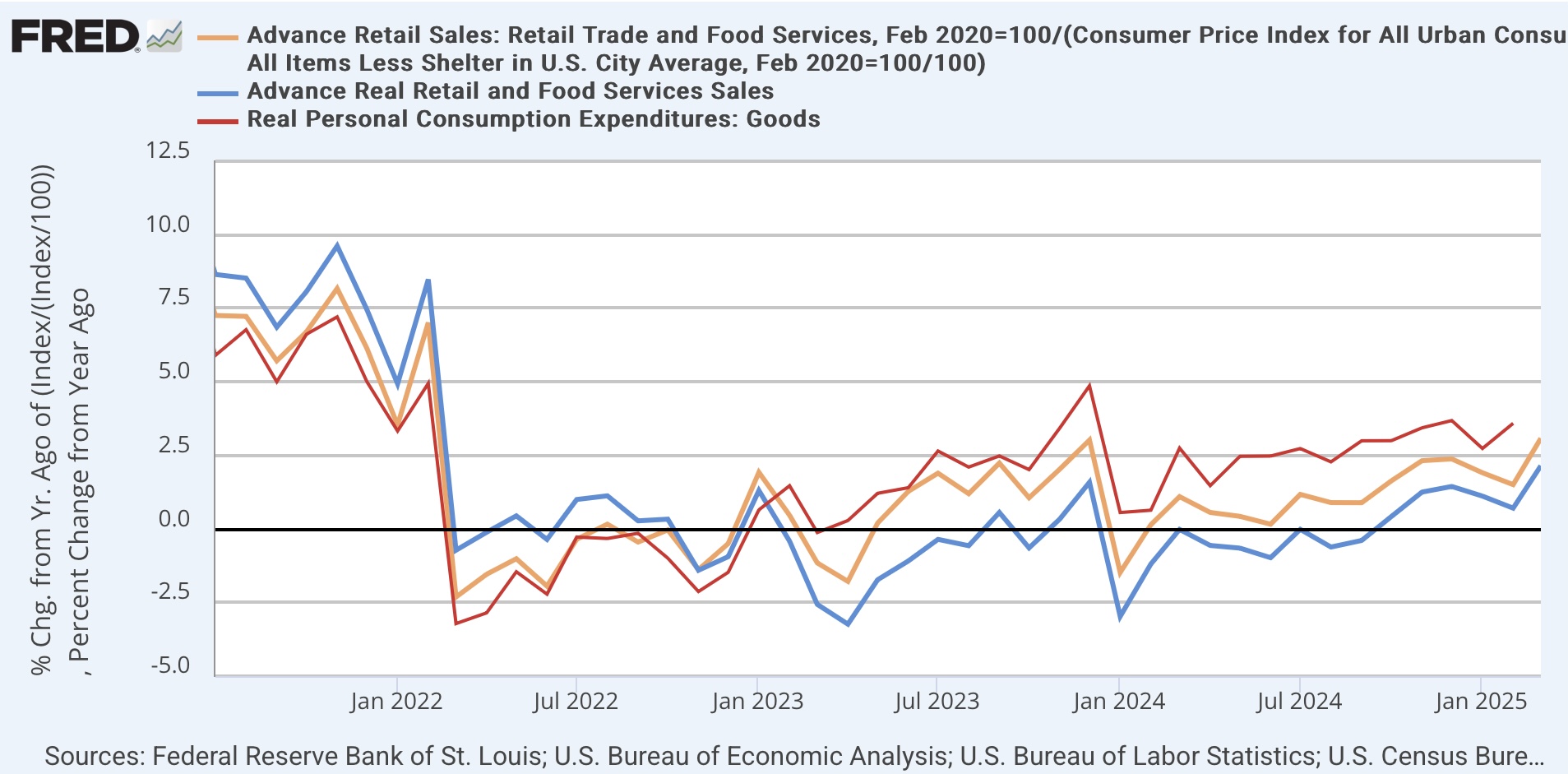

I suspect the big increases in February and March in manufacturing, like this morning’s retail sales numbers, were about front-running T—-p’s tariffs. Which means that like retail sales, production might have been pulled forward from the next few months, which may lead to whipsaw declines.

I think the best way to look at both pieces of data reported this morning is simply to note that expansion continued in March, and we’ll have to watch the incoming data especially carefully in the next few weeks and months.

In that regard, the New York Fed published its regional “Business Leaders Survey” for April this morning, headlining that:

“Business activity in the region’s service sector declined significantly for a second consecutive month, according to firms responding to the Federal Reserve Bank of New York’s April Business Leaders Survey. The survey’s headline business activity index came in at -19.8, its lowest level in more than a year. The business climate index dropped nine points to -60.7, its lowest level in more than four years, suggesting the business climate was considerably worse than normal.”

Here is the accompanying graph for the headline number:

Similar non-manufacturing surveys will be reported by the Philly, Richmond, Kansas City, and Dallas Feds over the next two weeks, and may give us our first hints of tariff-related declines in activity to the 70% of the economy that is services.

In the meantime, tomorrow we will get our first important look at the housing construction sector in March.